This report contains:

- Summary of UK Performance

- UK update on COVID-19

- The new normal that FMCG retailers and manufacturers expect after COVID-19

- Appendix: Focus on

Spain

Greece

New Zealand

Summary of UK Performance

- At the end of week 11 of the UK lockdown and the easing of restrictions in England continue. Current risk level remains at 4 but is close to 3, allowing restrictions to be eased and continued monitoring with the next update on the 15th June

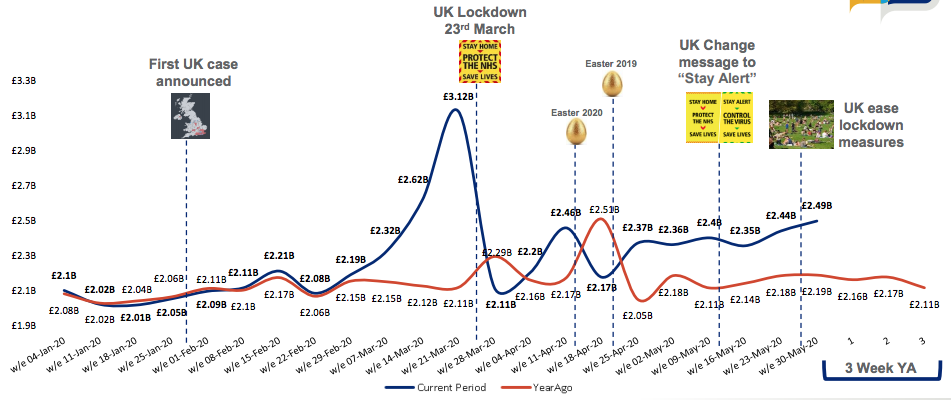

- In the latest week, which includes the Sunday/Monday sales for the recent Bank Holiday weekend and ½ term for many schools, sales reached £2.49b; £309m higher than the same time last year

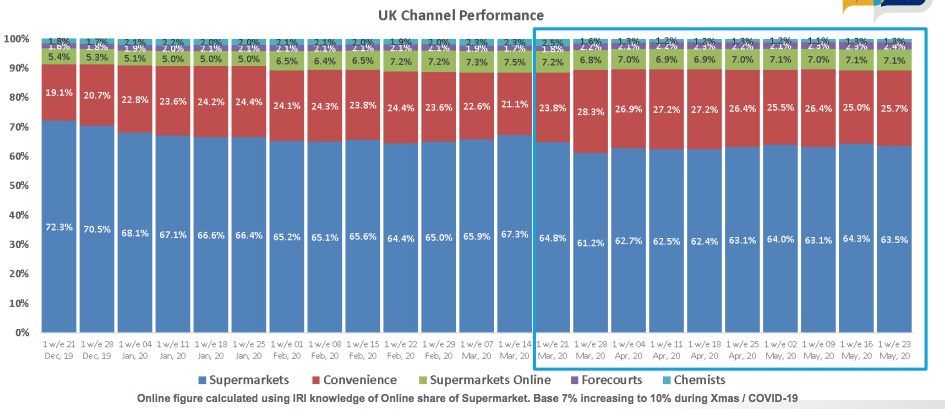

- Increase in Forecourts role across the channels as the easing of lockdown results in more movement. The Online channel maintains its importance in the UK retail environment however in the last few weeks the Convenience channel has lost share back to the Supermarkets

- The additional £309m Total Store sales is +14.2% vs year ago and is driven by an increased Grocery spend of £275.8m and £33.5m in Non Grocery

- Since the beginning of 2020 and predominantly since the start of COVID-19, UK Retailer sales are £3.124b higher than last year, driven by Ambient (+£1.1b) and BWS +(£728m) departments

- Frozen and BWS have seen significant increase in sales vs last year driven by the continued closure of the On-Trade and the warmest May on record in the UK

- UK Lockdown measures continue to drive the reduction in demand for Food to Go categories; Sandwiches, In-Store Deli’s and Bakeries. Laundry Detergents and Toilet Tissue again feature as a result of the panic buying spree in March/April

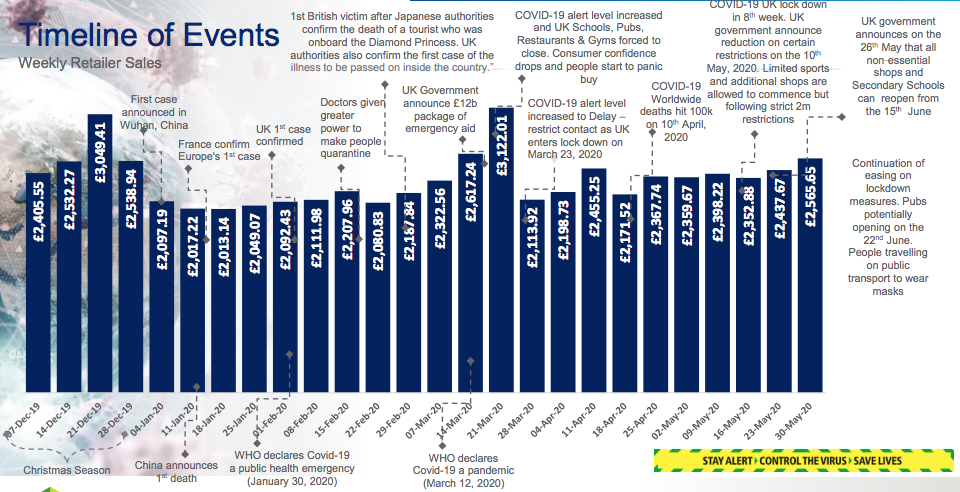

Timeline of events

End of the 11th week of the UK lockdown and the easing of restrictions in England continue. Current risk level remains at 4 but is close to 3, allowing restrictions to be eased and continued monitoring with the next update on the 15th June

- FTSE 100 hits it’s highest level in the last month as optimism towards the easing of restrictions drives the market.

- UK GPD drops in Q1 as a result of COVID-19. There was a widespread fall in output across the services, production and construction sectors

- Easing of Lockdown later in June. More non-essential Retail shops could open their doors, including Fashion and Tech shops

Total Market Value Sales – In the latest week, which includes the Sunday/Monday sales for the recent Bank Holiday weekend and ½ term for many schools, sales reached £2.49b; £309m higher than the same time last year

Increase in Forecourts as easing of the lockdown results in more movement. The Online channel maintains its importance in the UK retail environment however in the last few weeks the Convenience channel has lost share back to the Supermarkets

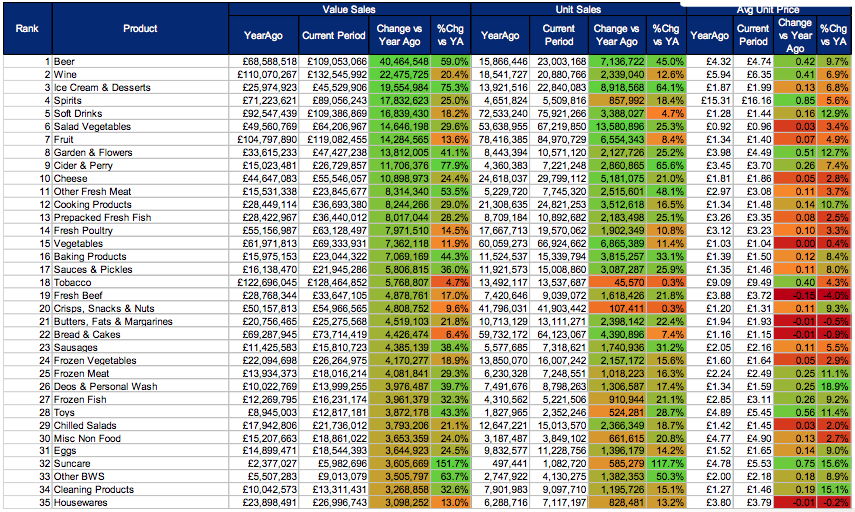

Top 35 Categories based on Value Change for the Latest Week

Top 12 Sub-categories based on Actual Value Change for the Latest Week