This report contains:

- Summary of UK Performance

- UK update on COVID-19

- Total Market Overview

- Additional Support from IRI

- IRI White paper

- IRI Global Demand Index

Summary of UK Performance

- Increased COVID-19 cases and greater local lockdown restrictions are the headlines of the 28th week of the UK lockdown and combined with Brexit are fuelling the concerns of the UK economy.

- Whilst we see an increase in cases, retailers are communicating that they are adding restrictions on quantities people can purchase. This should mean we don’t see the same levels of panic buying as earlier this year. However consumers will need reassuring they will not have problems buying their weekly shop.

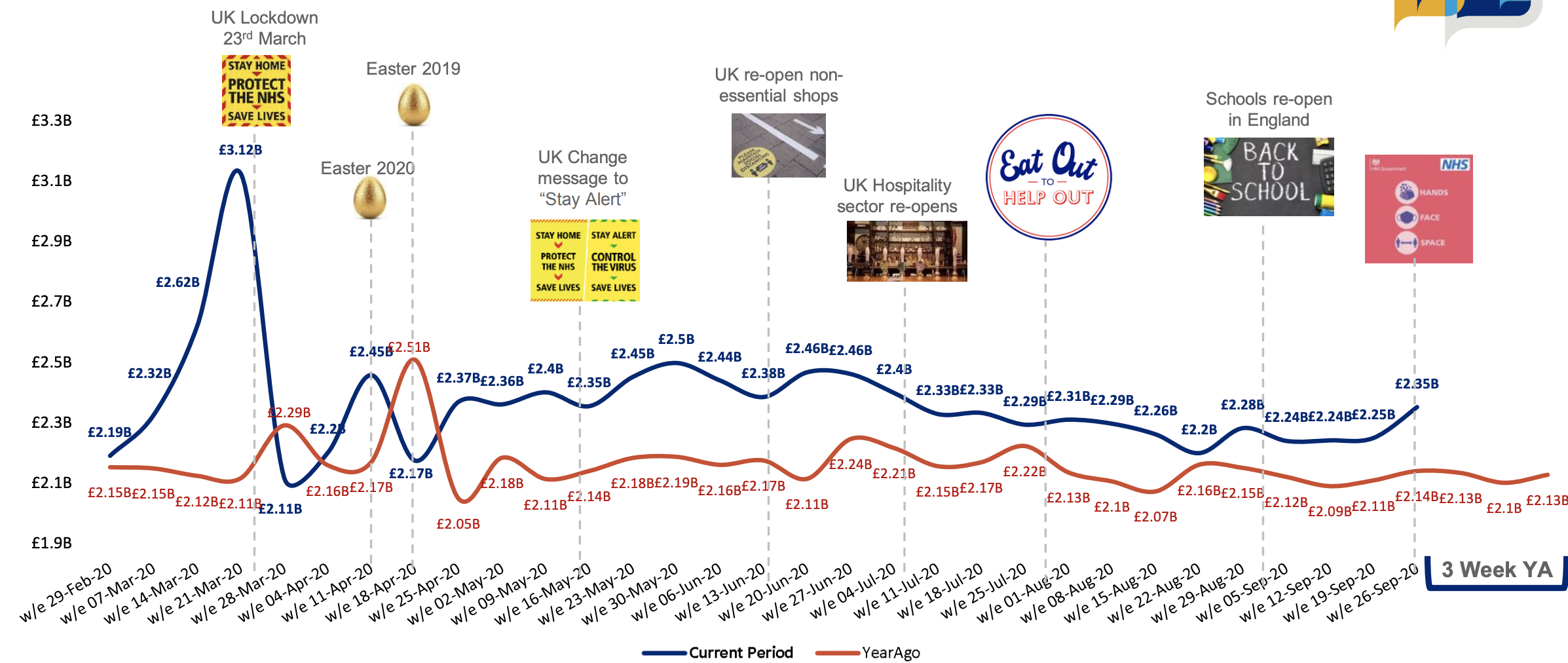

- In the latest week, sales reached £2.35b ; £211m higher than the same time last year up +4.5% on last week’s sales.

- Of the additional £211m spent in the latest week, this was driven predominantly by an increase in Grocery spend of £165m whilst £46m was spent in Non Food.

- Current UK COVID-19 Alert Level remain at 4, to signify an "epidemic is in general circulation; transmission is high or rising exponentially.

- This week's increase is seen across both Value and Units and with the restrictions being brought in by the government, our next set of data will be interesting to see the impact on sales.

- The Convenience and Online Channels have both benefitted from changing consumer shopping habits but the growth in the big shopping basket has seen Supermarkets share increase recently, however in the latest data, Convenience share has increased to 24.4%

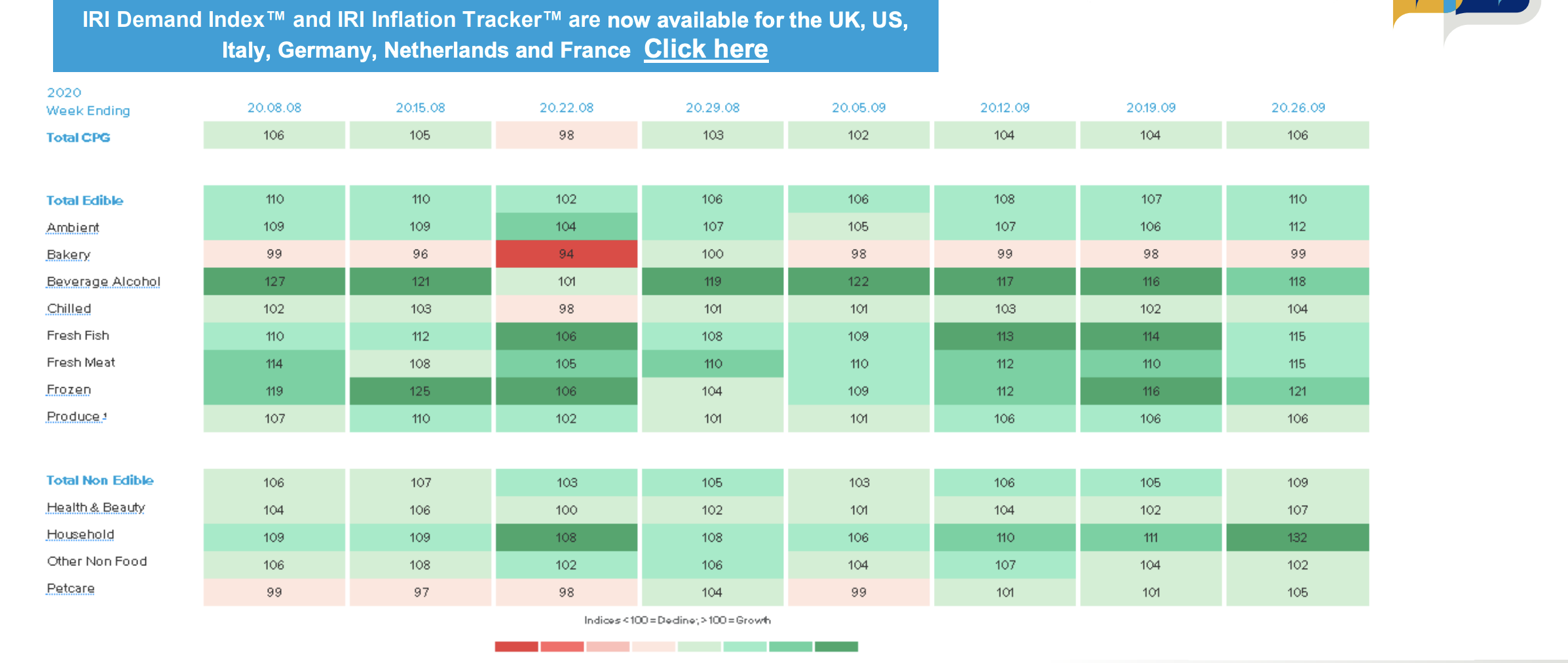

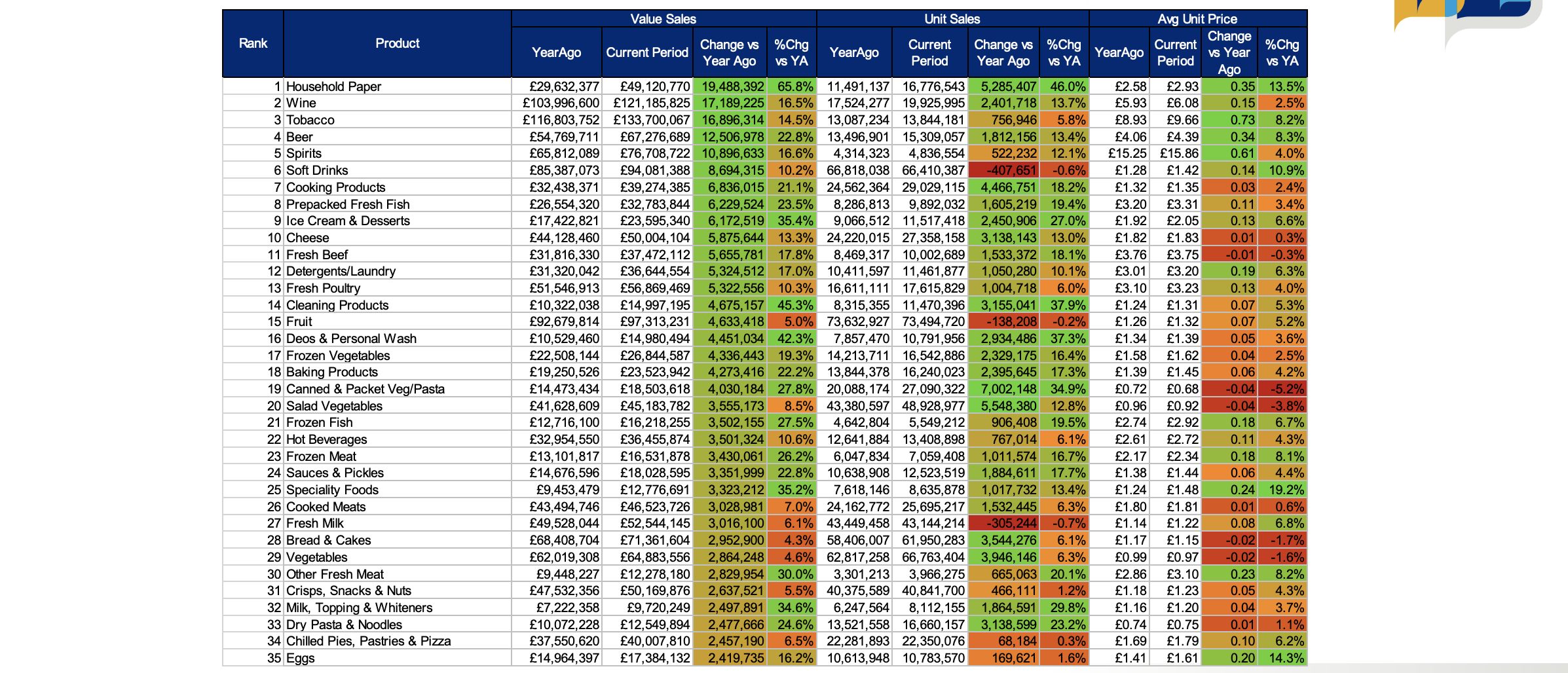

- IRI’s Demand Index Tracker shows Household (132) is driving Non Food. The growth in Household is driven by Household Paper e.g. Toilet Tissue (166) and Cleaning Products (132).

Total Market Sales Value

In the latest week, sales grew 4.5% on last week’s sales to £2.35b which is £211m higher than last year. The recent increases in COVID-19 cases and subsequent increased government restrictions being put in place have meant sales have increased; notably Toilet Tissues which grew 85% on last year and 59% on last week’s sales.

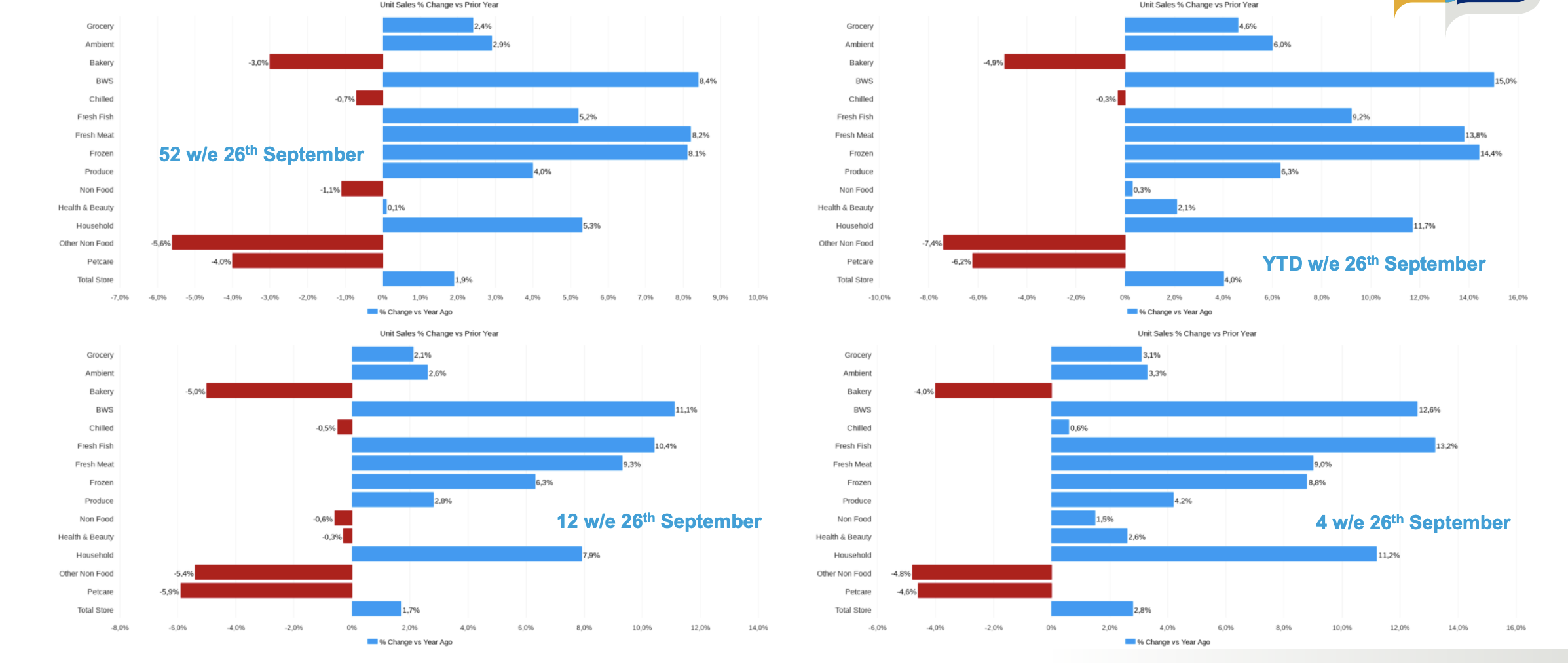

Total Store Unit sales growth in the latest 4w/e is +2.8% and has increased vs the latest 12w/e highlighting the growing signs of a 2nd wave, although not to same level as seen in March.

The recent increases in UK COVID-19 cases and subsequent increased government restrictions being put in place have meant demand for CPG products have increased.

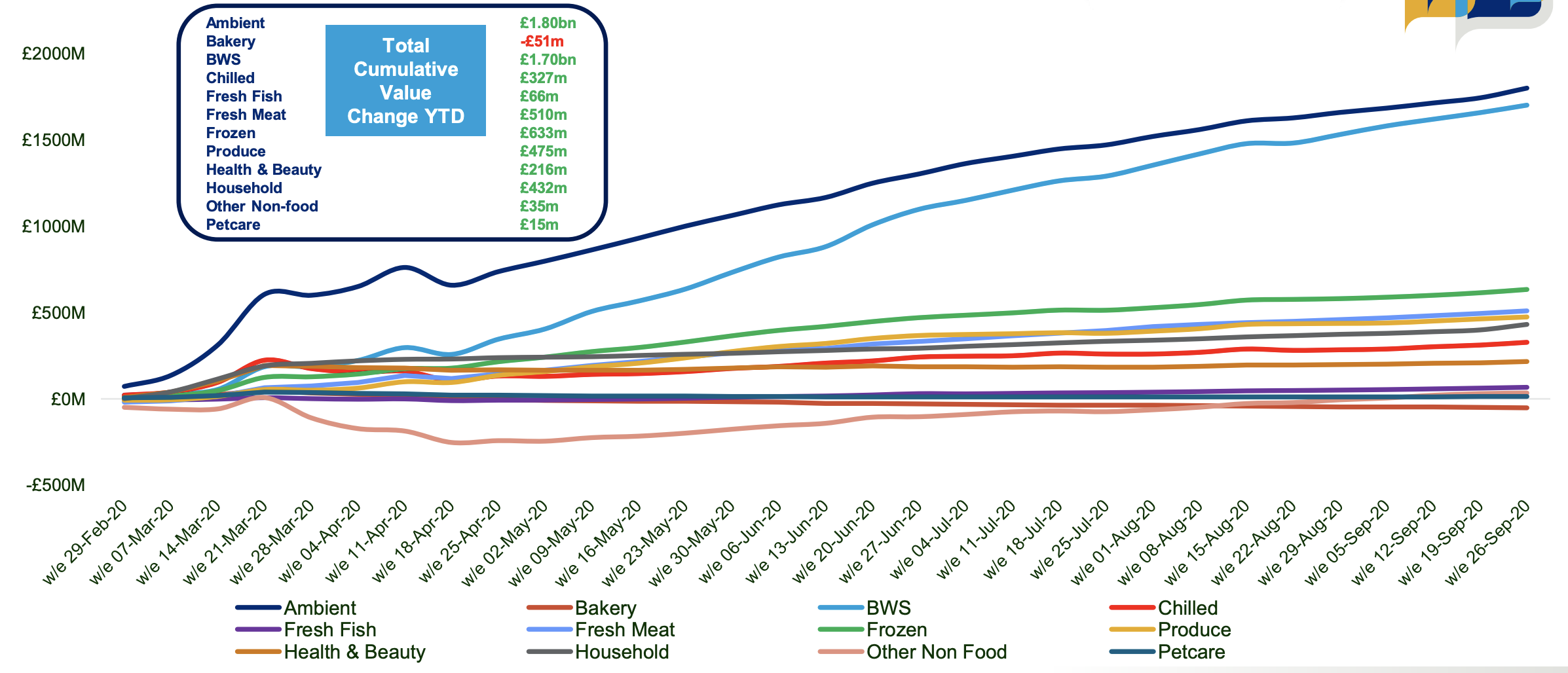

Since the beginning of 2020 and predominantly since the start of COVID-19, UK Retailer sales are £6.160b higher than last year, driven by Ambient (+£1.80b) and BWS (+£1.70b)

Top 35 Categories based on Value Change for the Latest Week.

-1.jpeg?width=480&name=AdobeStock_286414909%20(1)-1.jpeg)