This report contains:

- Summary of UK Performance

- UK update on COVID-19

- The new normal that FMCG retailers and manufacturers expect after COVID-19

- Appendix: Focus on

- Spain

- Greece

- New Zealand

SUMMARY OF UK PERFORMANCE

- End of the 15th week of the UK lockdown and the easing of restrictions in England continue. Risk level remains at 3 with further easing of restrictions gathering pace to help boost the UK economy

- Super Saturday (4th July) sees hairdressers, pubs and restaurants reopen with positive signs that helps fuel growth in the FTSE 100

- In the latest week, sales reached £2.48b; £230m higher than the same time last year and +0.4% up on last week. Last week’s sales were aided by the warm weather which also coincided with a warm spell that drove last year’s peak

- The Convenience channel has benefitted from the changing consumer shopping habits and currently accounts for 25% of all purchases

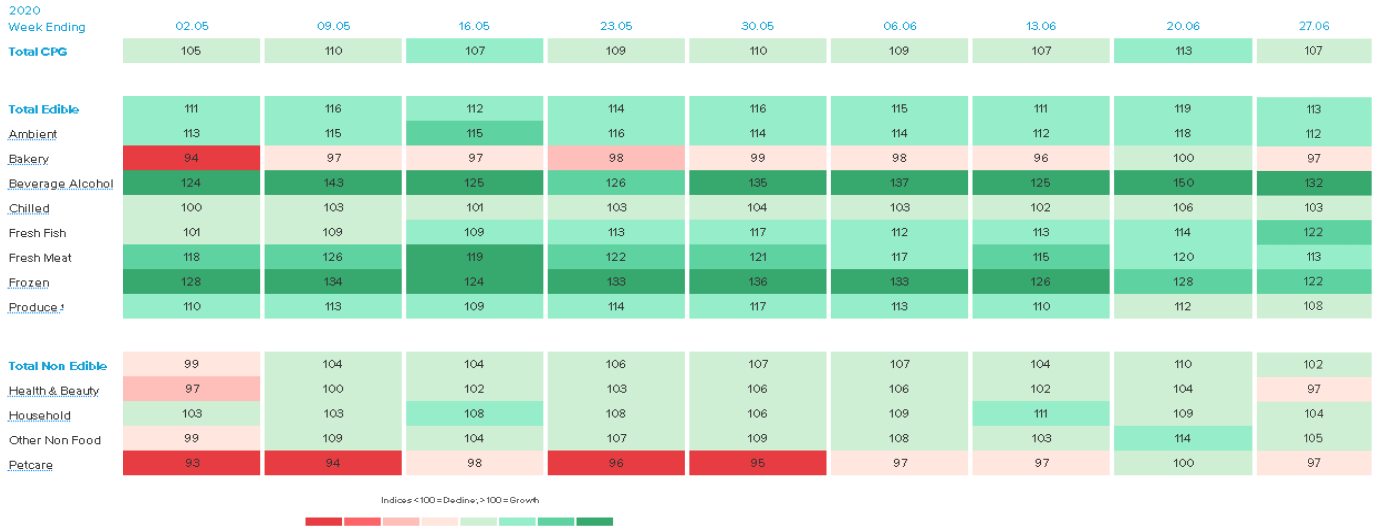

- Since the beginning of 2020 and predominantly since the start of COVID-19, UK Retailer sales are £4.201b higher than last year, driven by Ambient (+£1.3b) and BWS (+£1.1b) departments

- BWS, Tobacco, Meats/Fish, Ice Cream and Carbonates remain the top growing Sub-Categories

- UK Lockdown measures continue to impact the demand for Food to Go categories; Sandwiches, In-Store Deli’s, Bakeries, Newspapers and Laundry Detergents.

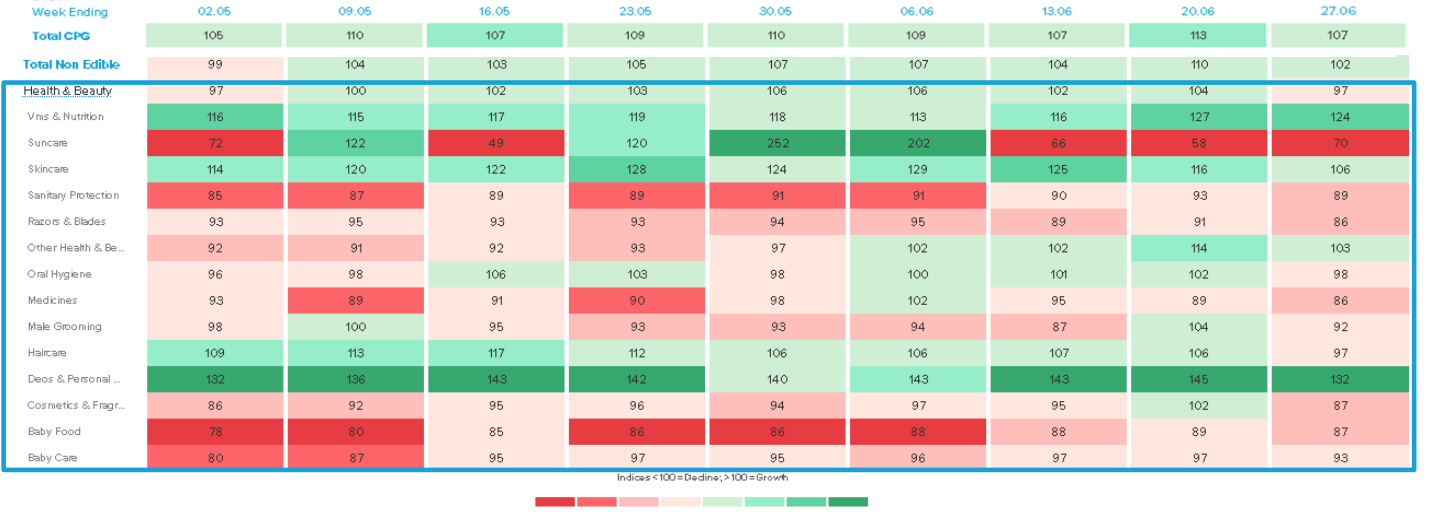

- Focus on Health & Beauty – Suncare is indexing down in recent weeks linked to the weather, however demand for Razor & Blades and Cosmetics & Fragrance is down as lockdown measures mean consumers have a lower need for personal appearance products

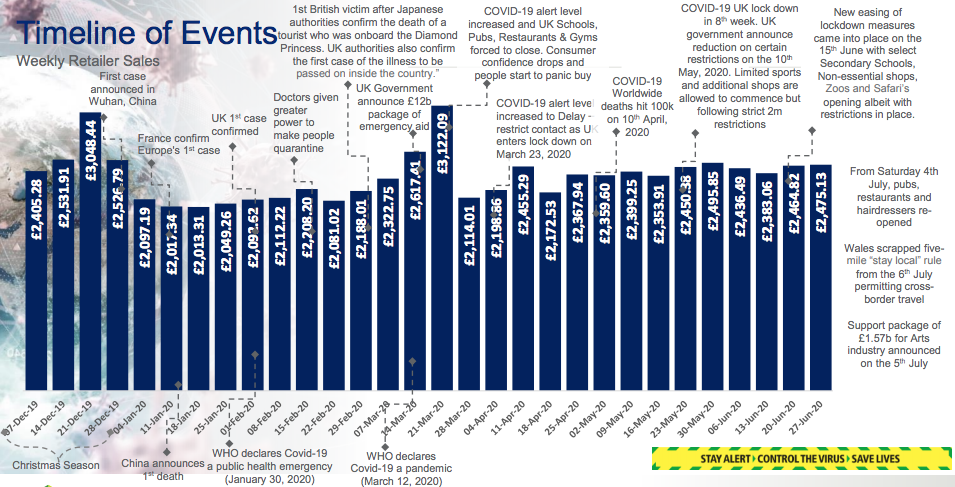

TIMELINE OF EVENTS

End of the 15th week of the UK lockdown and the FTSE 100 has recovered since the lows of April buoyed by the lockdown restrictions being relaxed

- FTSE 100 share climb following Super Saturday (4th July) where the pubs and restaurants reopened with positive signs and continued hopes on the economy rebounding

- Before COVID-19 many people had not heard of furlough. However since the scheme went live on the 20 April, about 185,000 firms have applied for support. Those claims alone covered 1.3 million workers and have cost the Treasury an estimated £1.5bn.

- The number of people visiting High Streets surged on "Super Saturday", as hairdressers, pubs, bars, cafes and restaurants reopened in England after a three-month lockdown. Research firm Springboard said footfall was 19.7% higher than last week, rising sharply after 17:00 BST

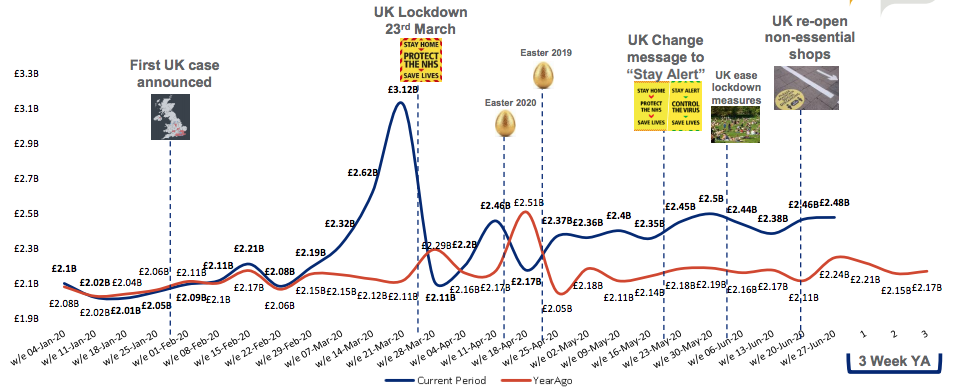

Total Market Value Sales –

In the latest week, sales reached £2.48b; £230m higher than the same time last year and 0.4% up on last week. Last week’s sales were aided by the warm weather which also coincided with a warm spell that drove last year’s peak

IRI’s Demand Index show Bakery, Health & Beauty and Petcare are indexing down vs last year

Focus on Health & Beauty – Suncare is indexing down in recent weeks linked to the weather, however demand for Razor & Blades and Cosmetics & Fragrance is down as lockdown measures mean consumers have a lower need for personal appearance products

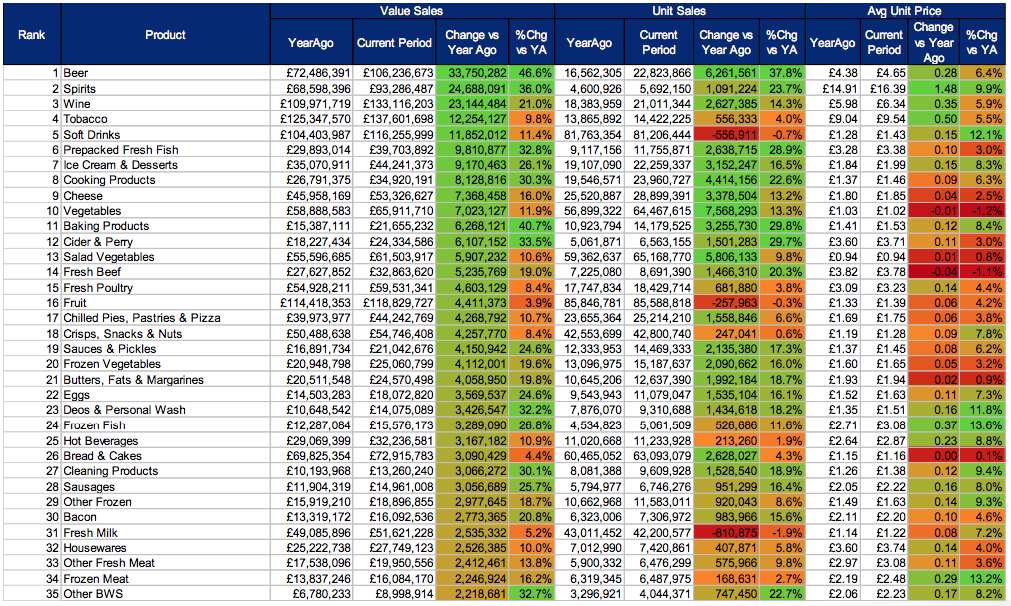

Top 35 Categories based on Value Change for the Latest Week