This flash report contains:

• UK Market Context

• Summary of UK Performance

• Category Performance

• Top Manufacturers

• Bottom Manufacturers

Summary of UK Performance

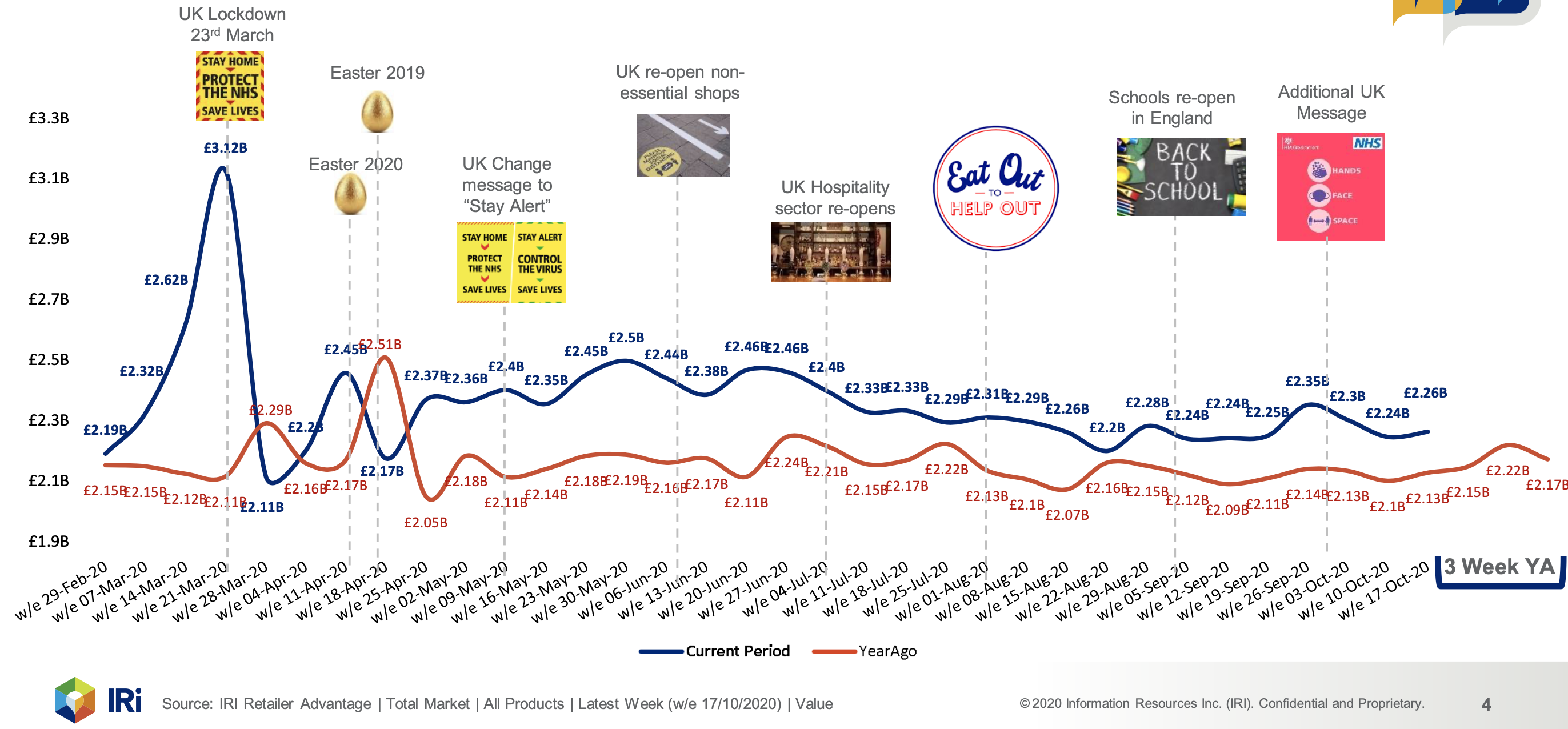

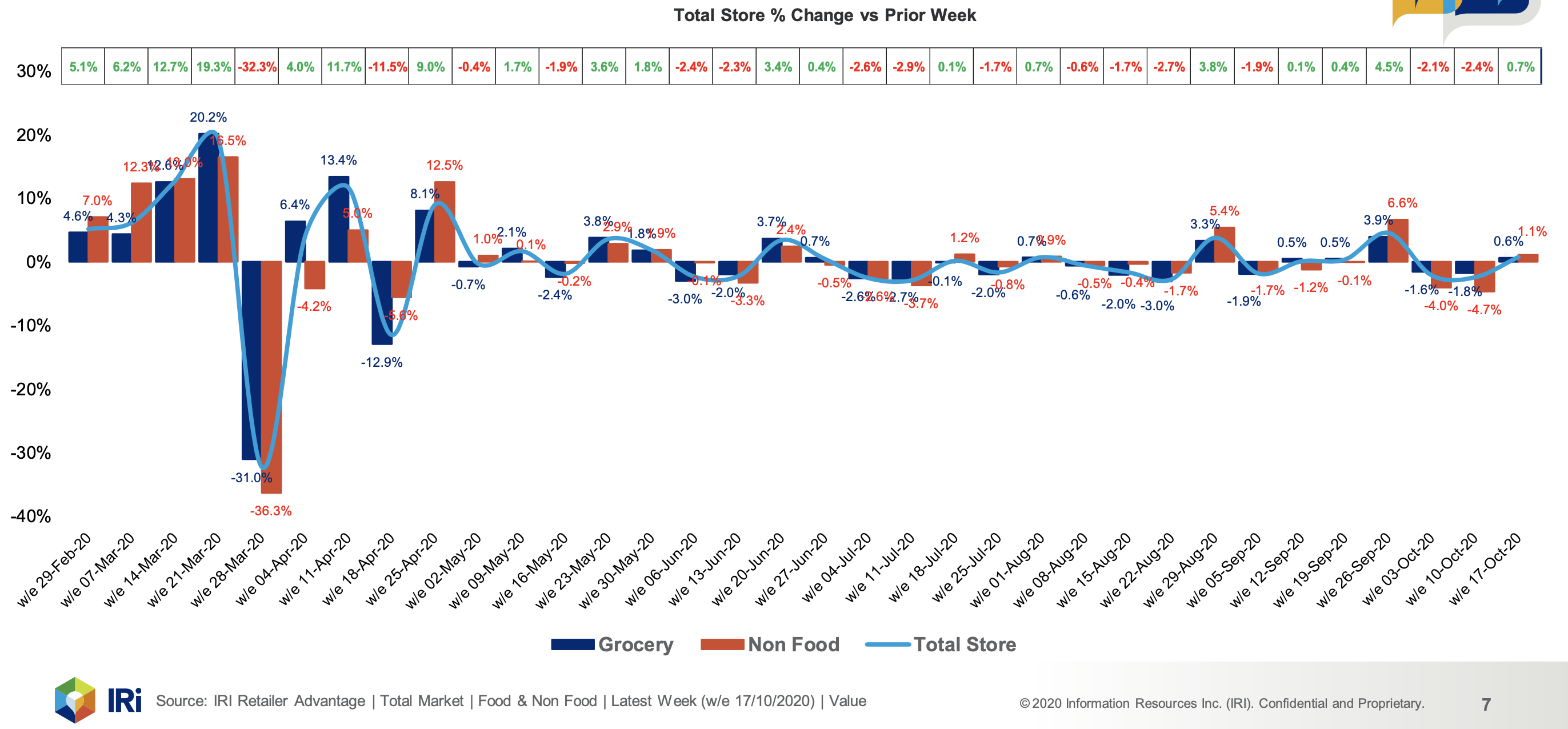

- With the increase in COVID-19 cases and more local areas moving into Tiers 2 and 3, we’ve seen a small +0.7% increase in sales compared to last week.

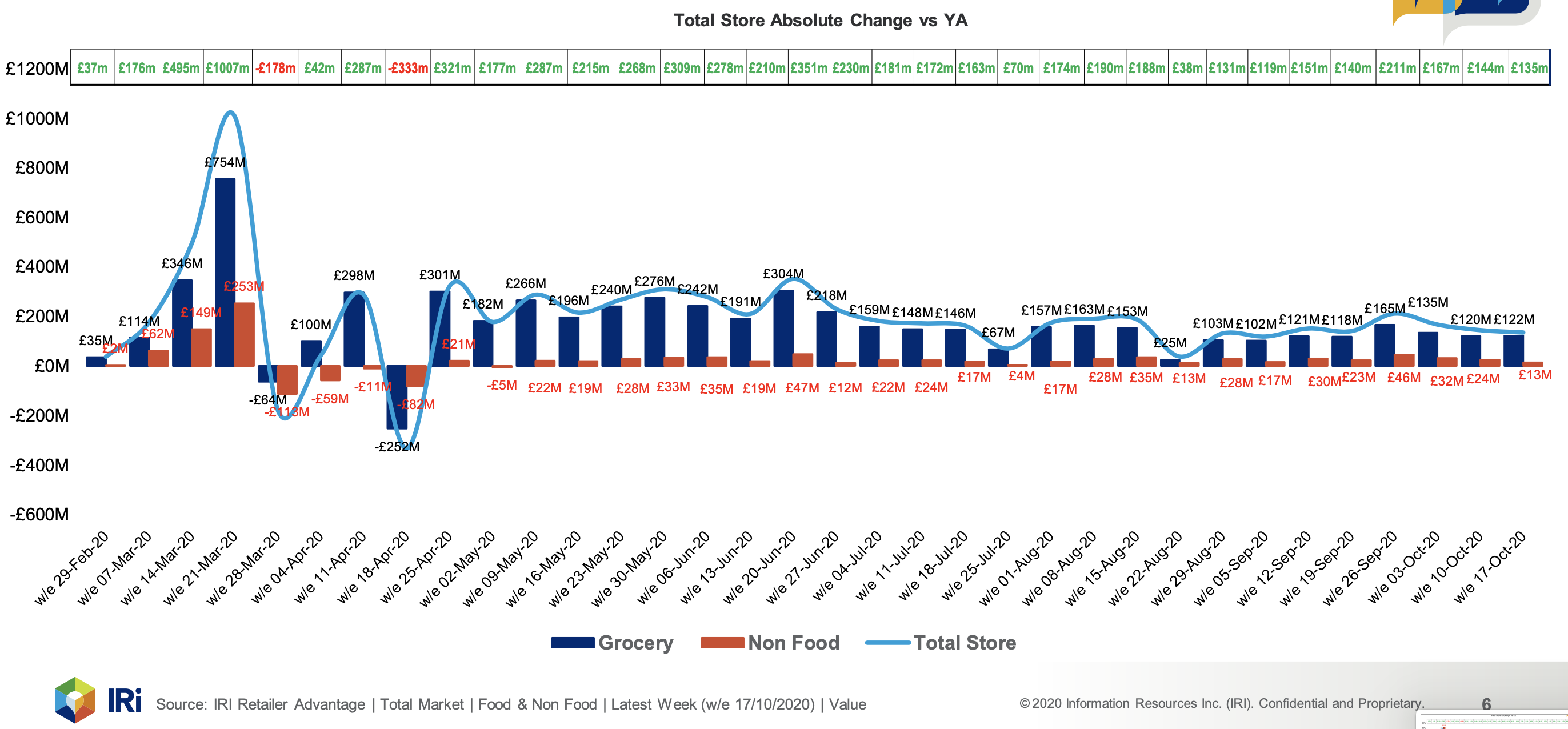

- This week's sales of £2.26b are £135m ahead of last year’s which is a similar picture to last week, reinforcing our assertion that greater in-home consumption has become the norm. With increasing case numbers and the threat of Tier mobility we should expect to see this trend continue over the coming weeks.

- The additional £135m spent in the latest week was driven by an increased Grocery spend of £122m and £13m in Non Food.

- Tracking of Halloween 2020 - In the run up to the 31st October, as we’d expect, the trend line shows an increase across all categories. Only Cakes are down vs YA as the governments message around staying at home for this years Trick or Treating has so far encouraged people to buy into the occasion.

Total Market Sales Value

With the increase in COVID-19 cases and more local areas moving into Tiers 2 and 3, we’ve seen a small +0.7% increase in sales compared to last week. This week's sales of £2.26b are £135m ahead of last year’s which is a similar picture to last week, reinforcing our assertion that greater in-home consumption has become the norm. With increasing case numbers and the threat of Tier mobility we should expect to see this trend continue over the coming weeks.

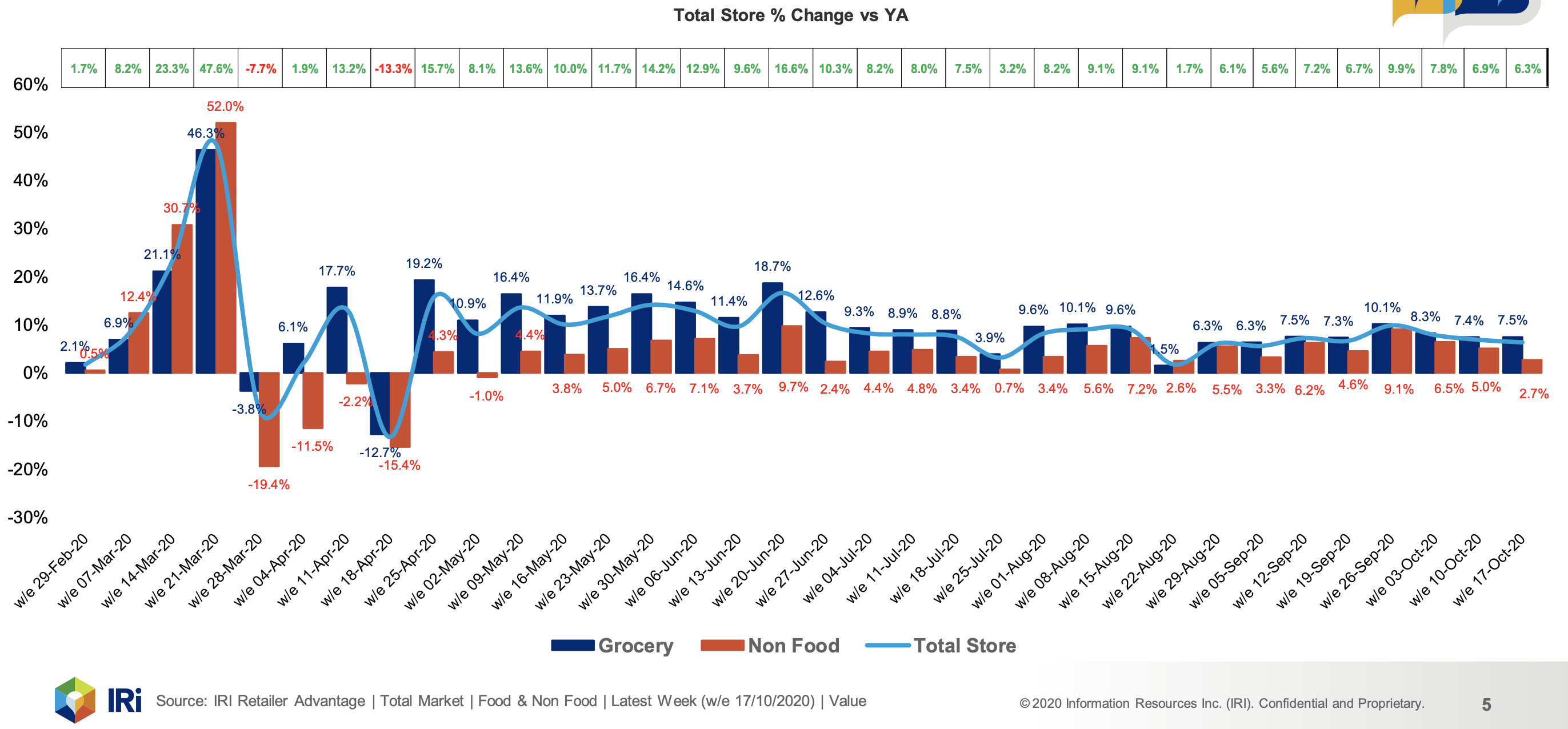

Total Store sales +6.3% vs year ago with Grocery growth +7.5% and Non Food growth +2.7%

An Additional £135m has been spent in the latest week driven by an increased Grocery spend of £122m and £13m in Non Food

Overall sales grew +0.7% this week compared to last week with Grocery sales up +0.6% and Non Food sales up +1.1%

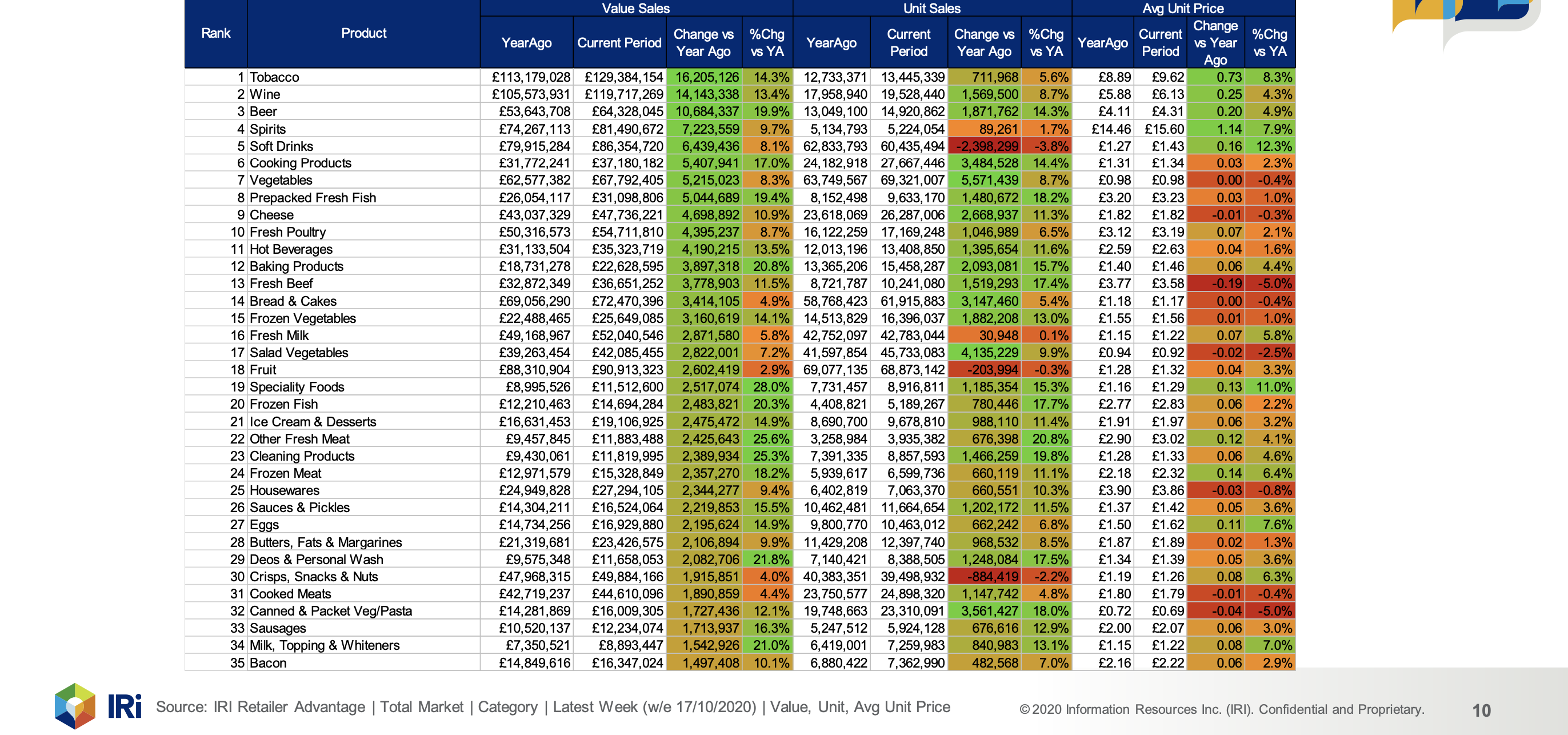

Top 35 Categories based on Value Change for the Latest Week