This flash report contains:

• UK Market Context

• Summary of UK Performance

• Category Performance

• Top Manufacturers

• Bottom Manufacturers

• Christmas Trackers

Summary of UK Performance

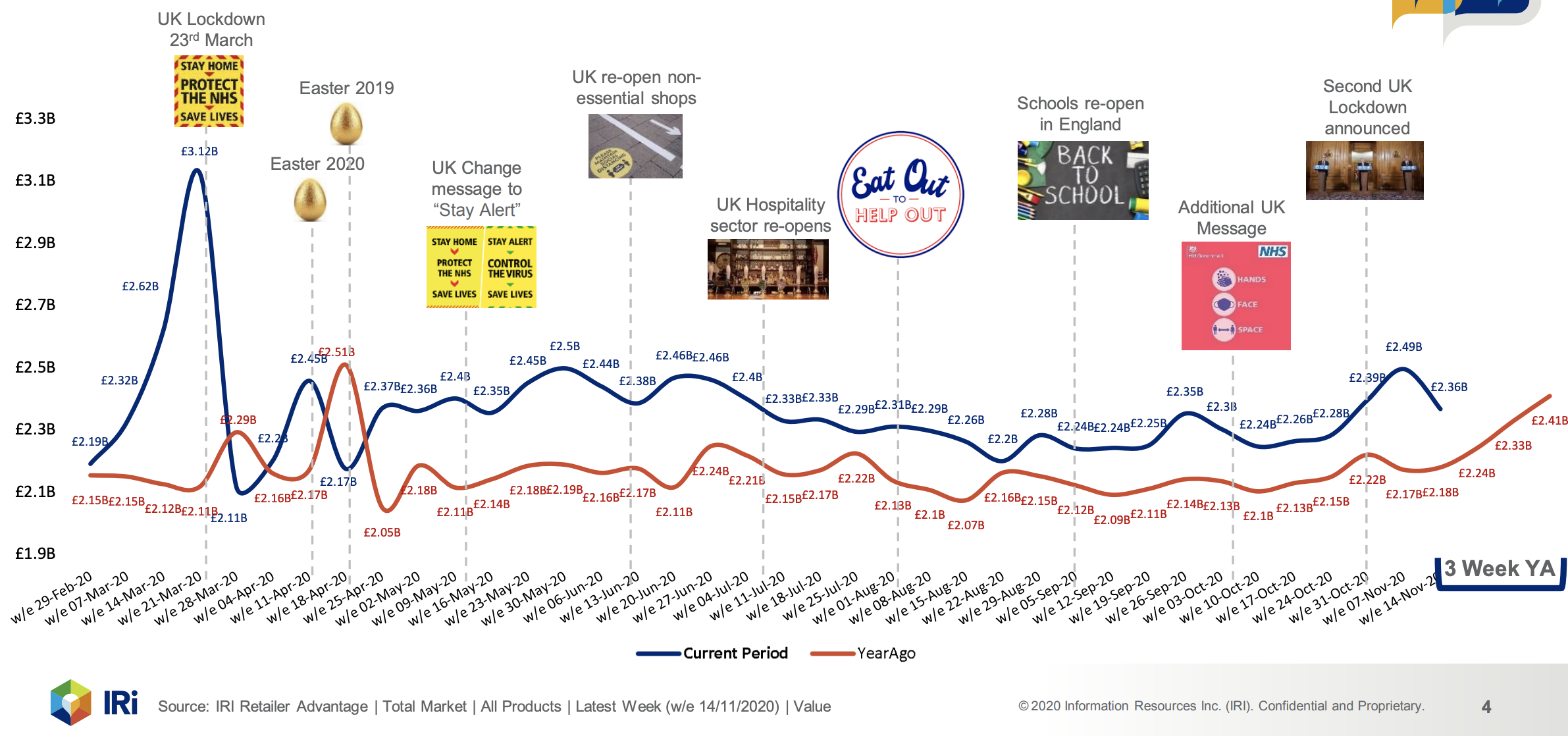

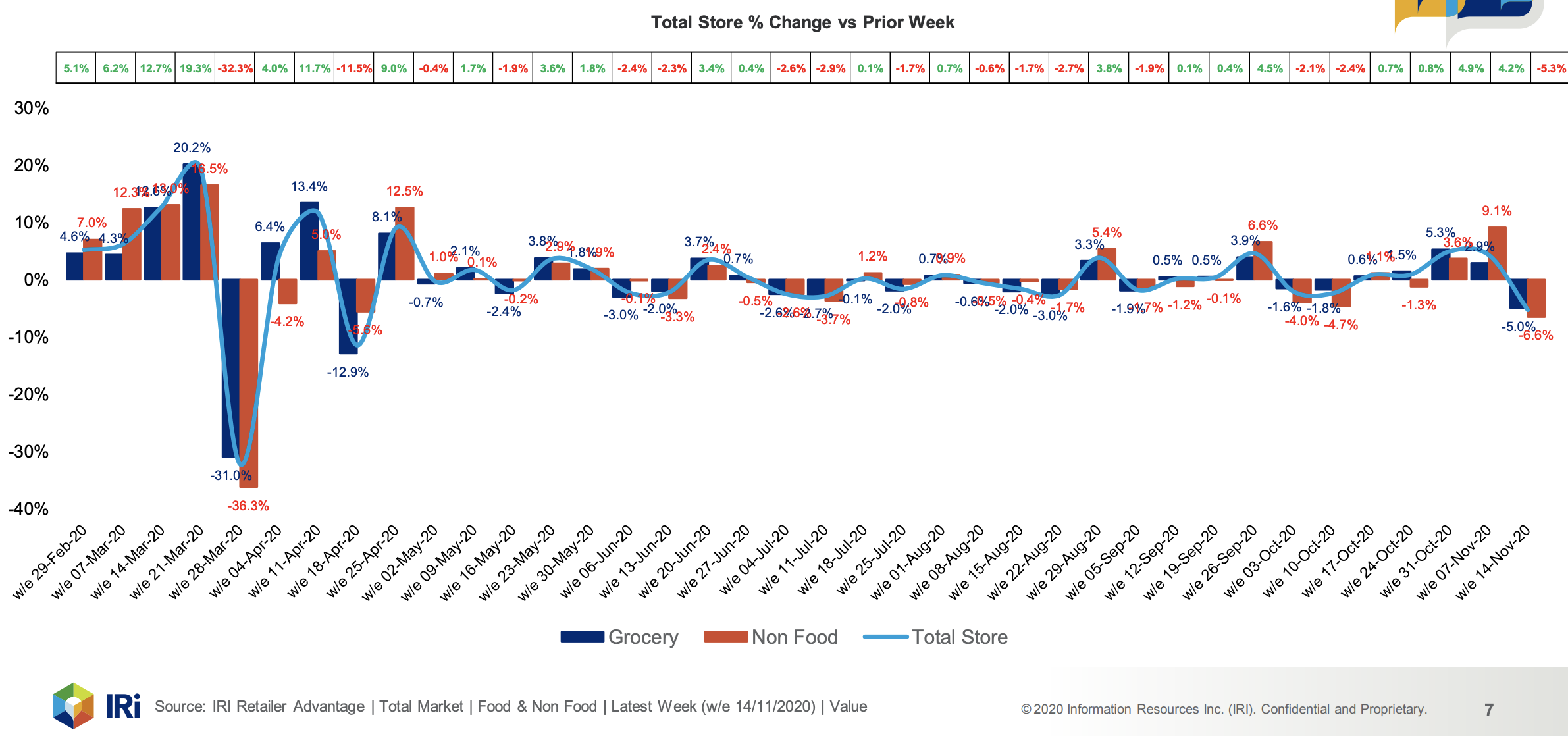

- After the high of last week caused by an element of panic buying as England entered its 2nd lockdown, this week’s sales dropped -5.3%.

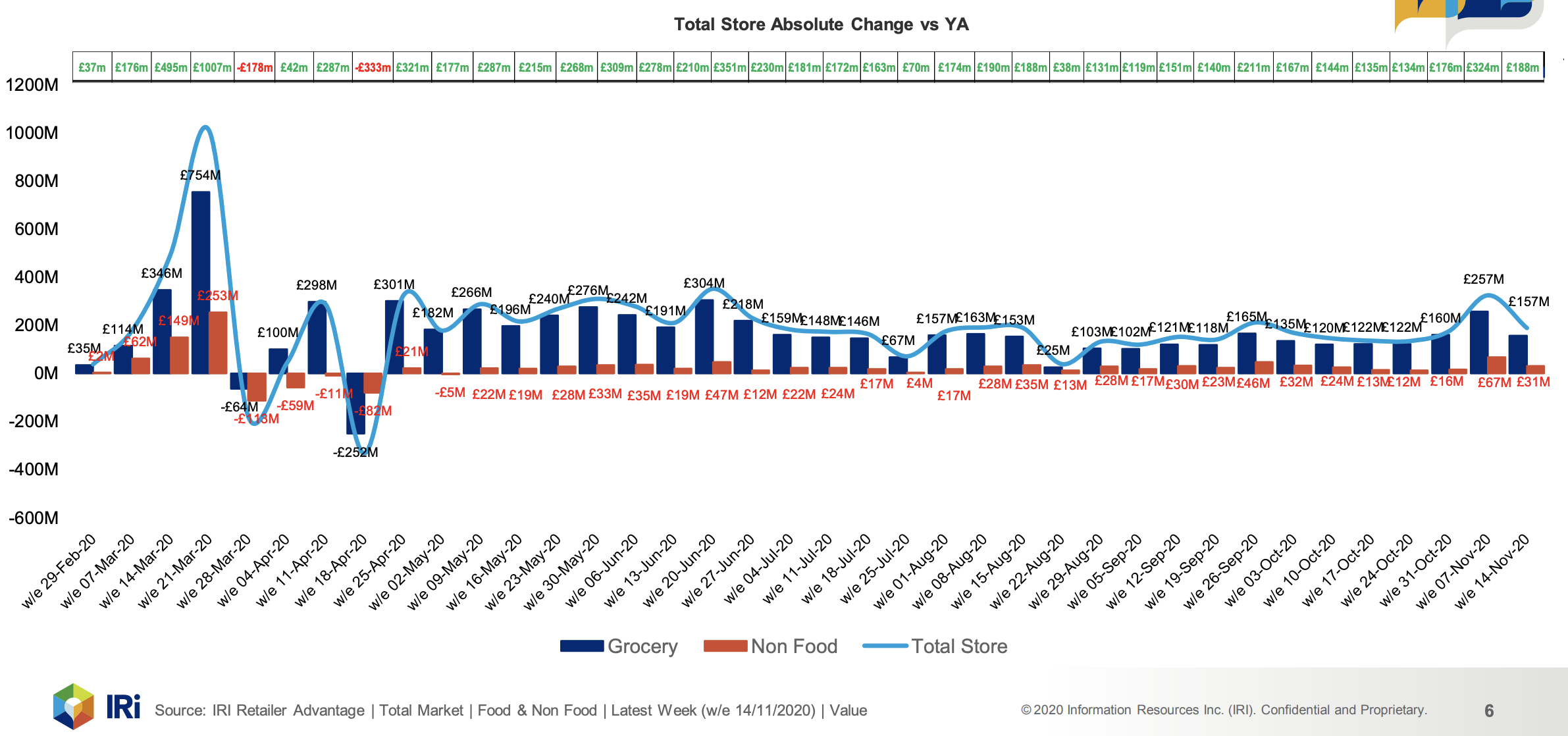

- However sales of £2.36b is £188m higher than the equivalent week last year. Demand for Eating at Home categories remains high but with restrictions being in place for months now, shoppers have been able to adapt, along with retailers and manufacturers.

- The additional £188m spent in the latest week was driven by Grocery spend of £157m and £31m in Non Food.

- Tracking of Christmas 2020: Based on the latest 7 weeks of sales, the Christmas categories in focus are +12.6% (£600m) ahead of last year. Whilst COVID-19 makes tracking the performance of Christmas difficult, we can see Seasonal Cakes are down, so not all categories are in growth.

- Since the beginning of 2020 and predominantly since the start of COVID-19, UK Retailer sales are £7.431b higher than last year, driven by Ambient (+£2.14b) and BWS (+£2.04b)

Total Market Sales Value

After the high of last week caused by an element of panic buying as England entered its 2nd lockdown, this week’s sales dropped -5.3% to £2.36b. However, sales stand £188m higher than the equivalent week last year. Demand for Eating at Home categories remain high but with restrictions being in place for months now, shoppers have been able to adapt, along with retailers and manufacturers.

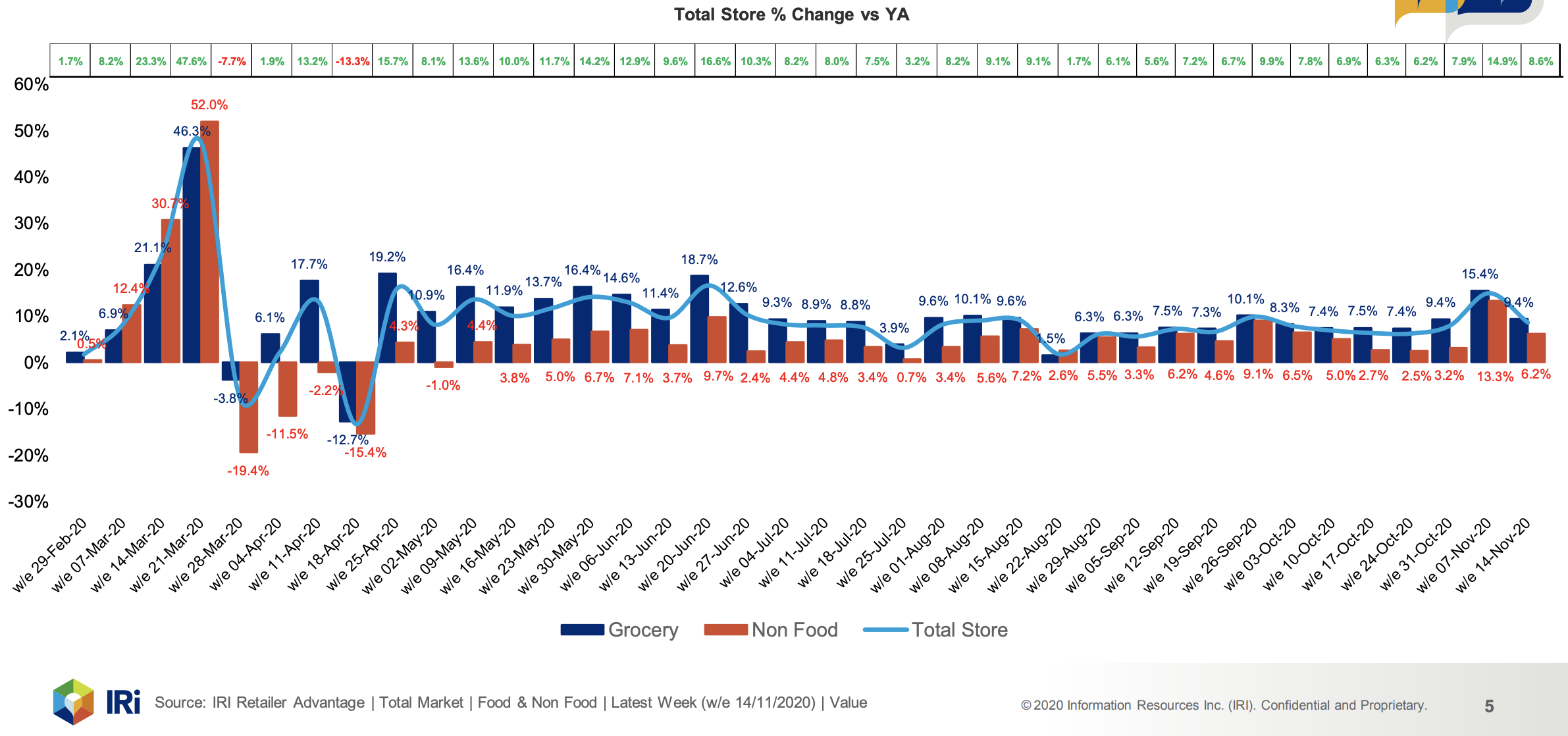

Total Store sales grew +8.6% vs year ago with Grocery growth +9.4% and Non Food growth +6.2%.

An Additional £188m has been spent in the latest week driven by Grocery spend of £157m and £31m in Non Food.

Overall sales fell -5.3% this week compared to last week with Grocery sales down -5.0% and Non Food sales down -6.6%.

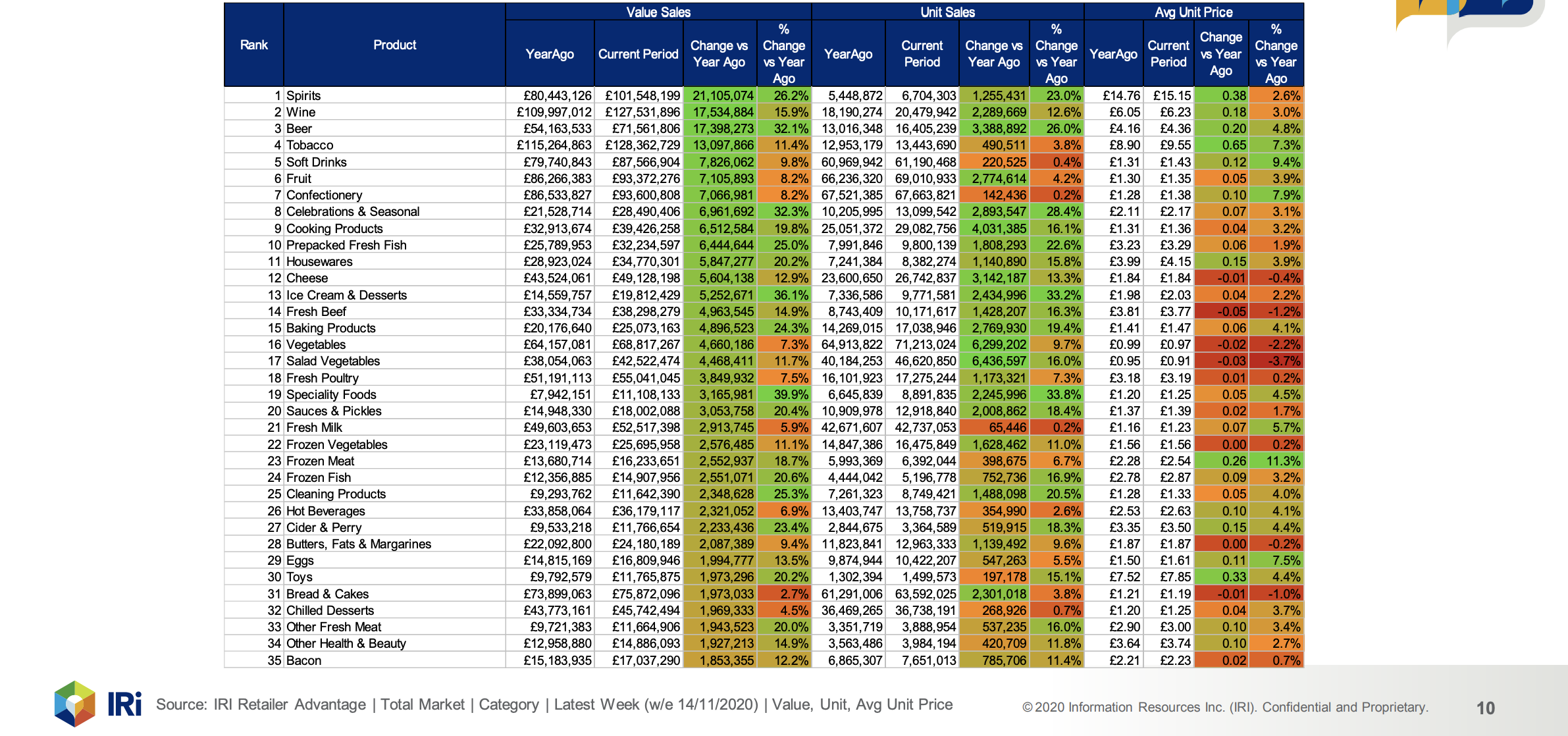

Top 35 Categories based on Value Change for the Latest Week