This flash report contains:

• UK Market Context

• Summary of UK Performance

• Category Performance

• Top Manufacturers

• Bottom Manufacturers

Summary of UK Performance

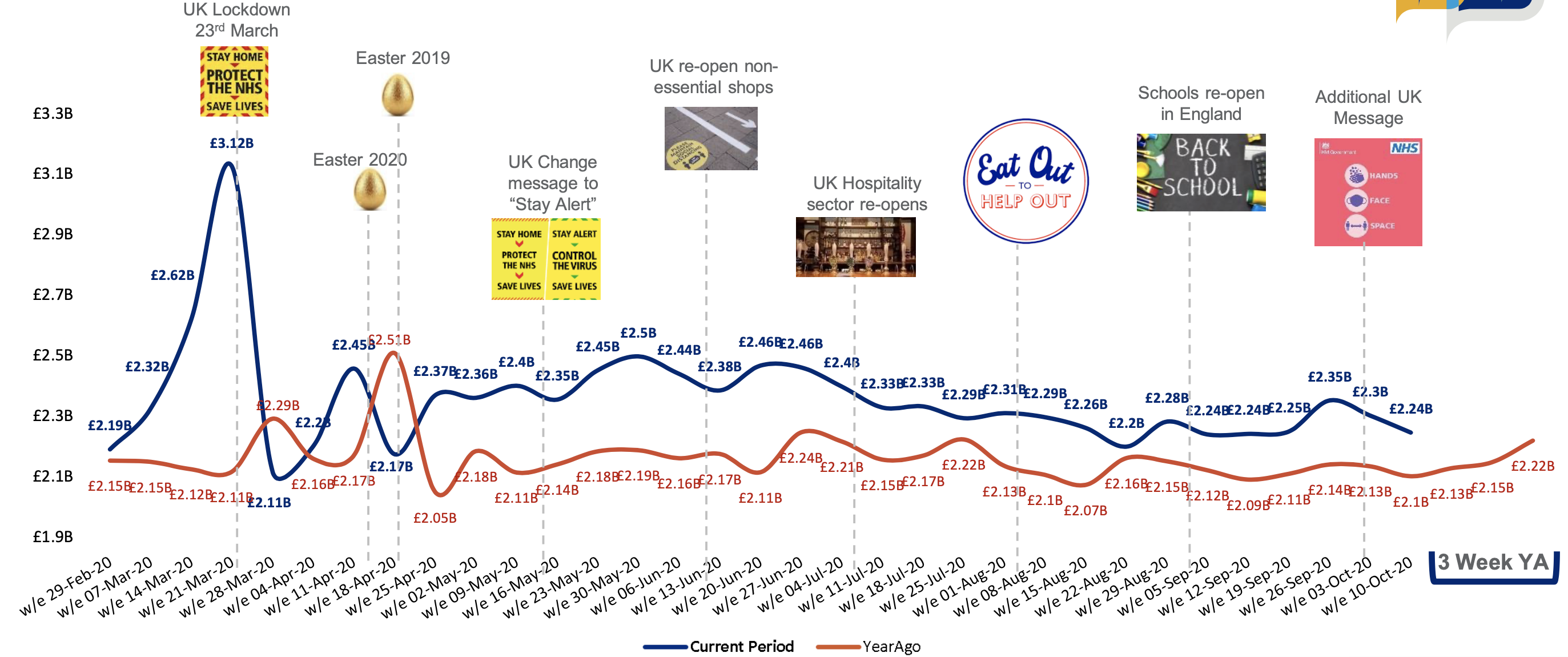

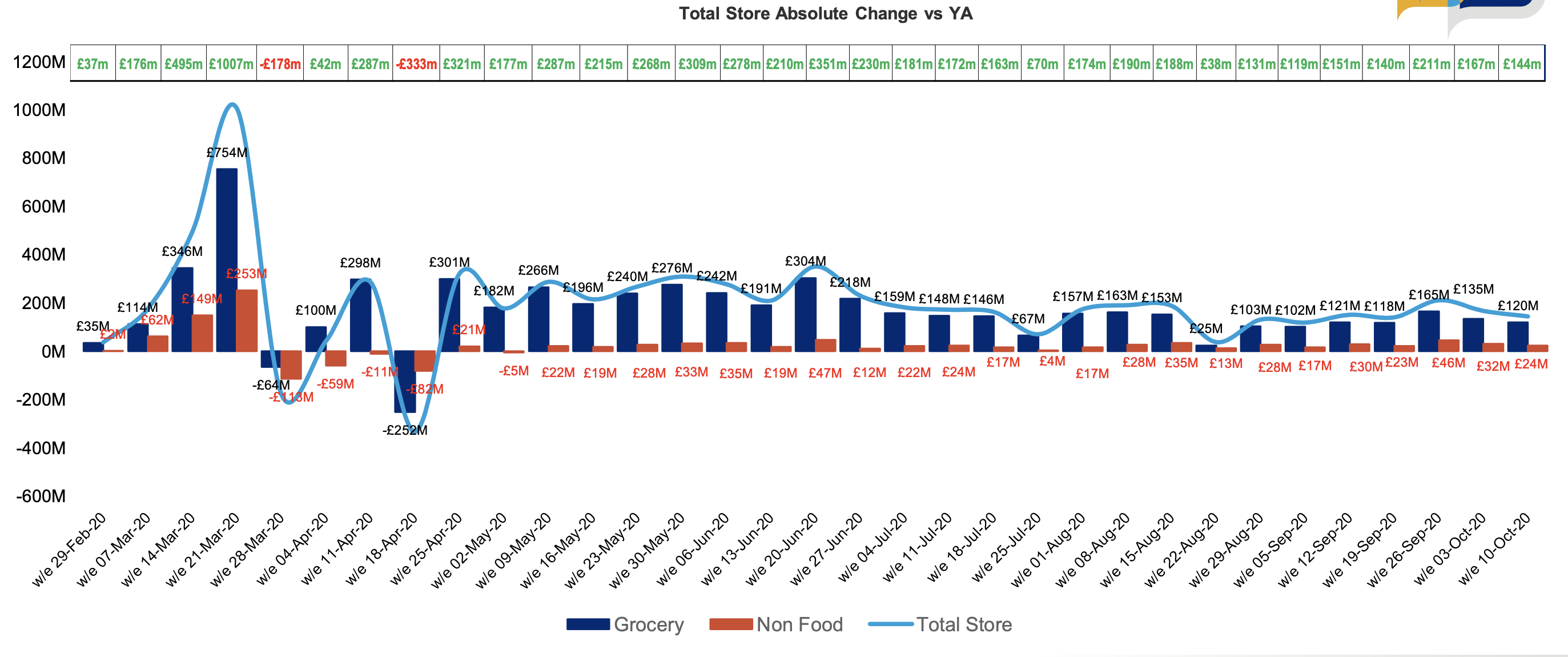

- This week's sales of £2.24b are still £144m ahead of last years’ driven by the continuing trend to eat and drink at home; a continuation of habits developed during lockdown. With greater local restrictions coming into force this week, it will be interesting to discover what impact they will have on next weeks’ sales.

- Of the additional £144m spent in the latest week, this was driven by an increased Grocery spend of £120m and £24m in Non Food.

- Tobacco, BWS and Pre-packed Fresh Cooked Meats / Fish, Carbonates and Ice Cream feature in the top growing Sub-Categories

- Worst performing Sub Categories remain those impacted by the continued lack of movement, so Food to Go categories; Sandwiches, In-Store Bakery Goods and Filled Rolls & Wraps as well as those impacted by closure of Deli and Fresh counters.

- Since the beginning of 2020 and predominantly since the start of COVID-19, UK Retailer sales are £6.471b higher than last year, driven by Ambient (+£1.88b) and BWS (+£1.79b)

Total Market Sales Value

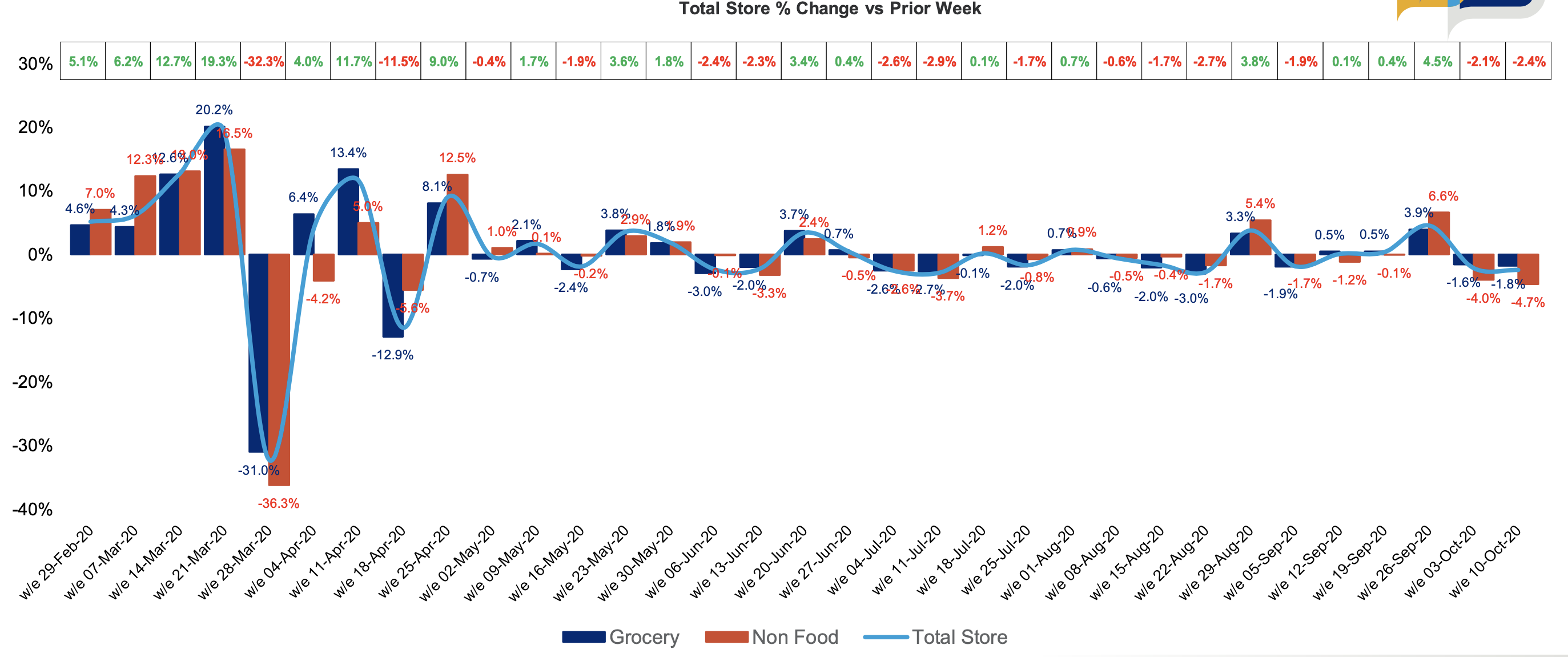

Even with the increase in COVID-19 cases, we’ve seen a -2.4% decline in sales compared to last week. This week's sales of £2.24b are still £144m ahead of last years’ driven by the continuing trend to eat and drink at home; a continuation of habits developed during lockdown. With greater local restrictions coming into force this week, it will be interesting to discover what impact they will have on next weeks’ sales.

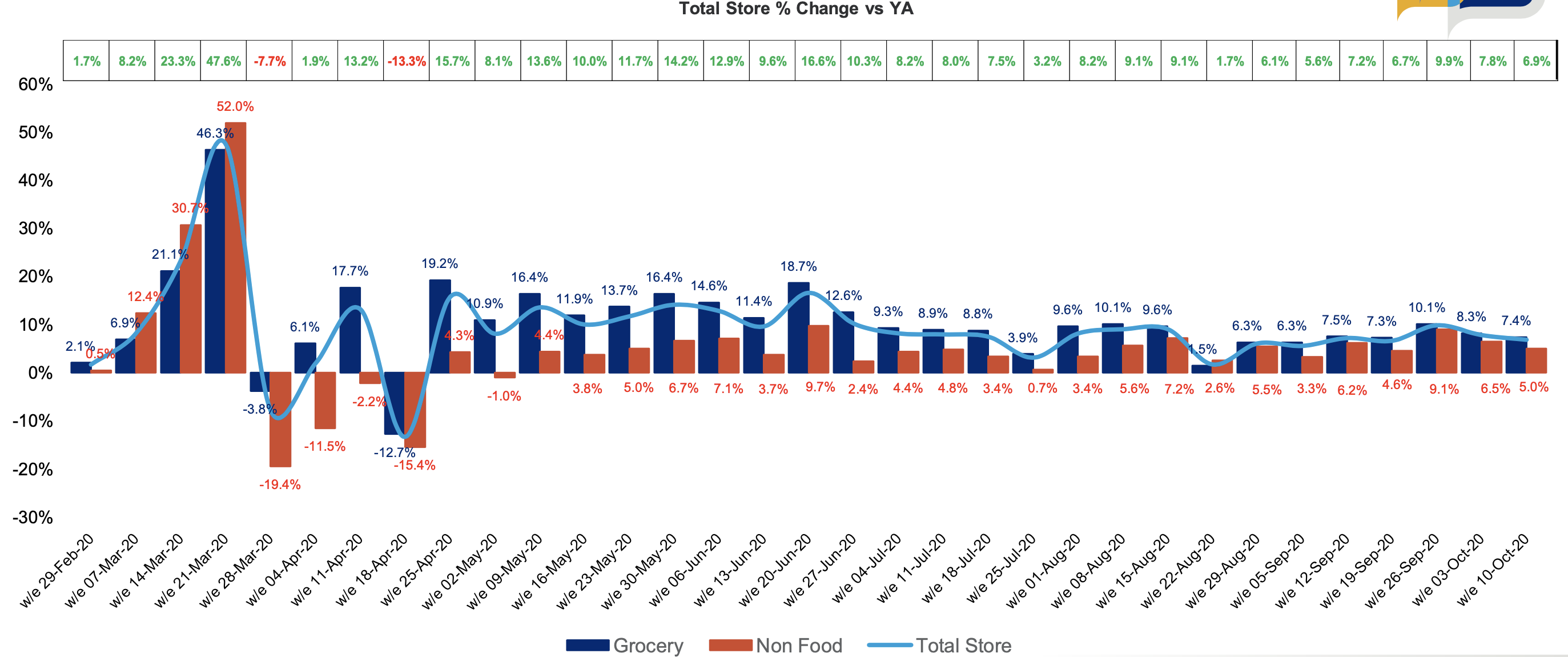

Total Store sales +6.9% vs year ago with Grocery growth +7.4% and Non Food growth +5.0%

An Additional £144m has been spent in the latest week driven by an increased Grocery spend of £120m and £24m in Non Food

Overall sales fell -2.4% this week compared to last week with Grocery sales down -1.8% and Non Food sales down -4.7%