We know that information is vital during the current COVID-19 crisis to help fire up the engines of business, so we thought it would be helpful to share some insights from our IRI colleagues from around the world on the Impact of the Coronavirus on the FMCG industry, in the UK, Spain, Germany and New Zealand.

Key highlights are shown in this post, but download the full report for:

- A wider update on COVID-19 in the UK

- Detail on implications for Manufacturers and Retailers

- An appendix with further details on the impact in:

- Spain

- New Zealand – Italy

- Germany

- Greece

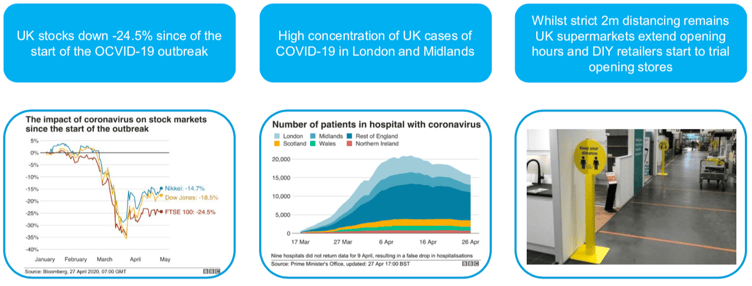

UK impact and implications

- First case in the UK was on the 31st January 2020 from someone that had recently returned from mainland China

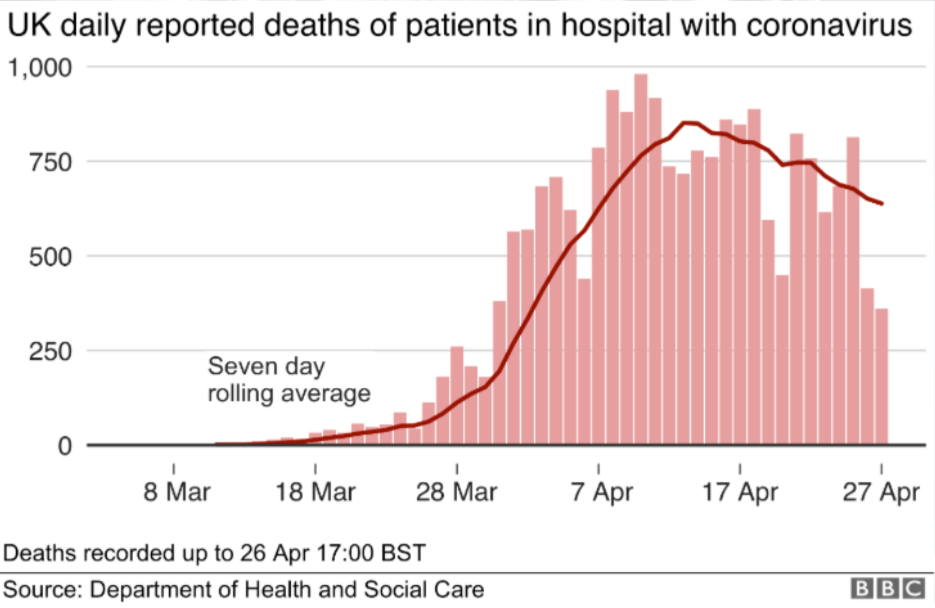

- As of 9am on 27th April 2020, 569,768 people have been tested, of which 157,149 were confirmed positive. As of 5pm on 26th April 2020, of those hospitalised in the UK who tested positive for coronavirus, 21,092 have died.

- The UK remains in Delay stage with Coronavirus spreading and a global pandemic continues

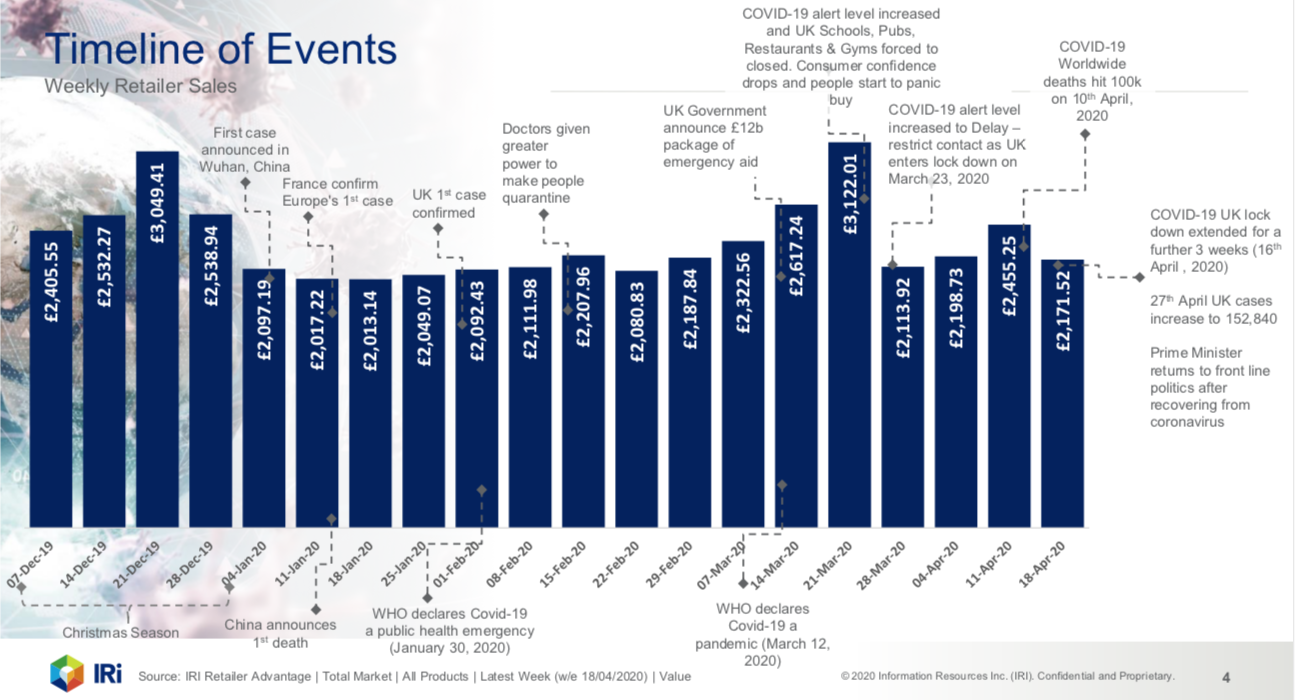

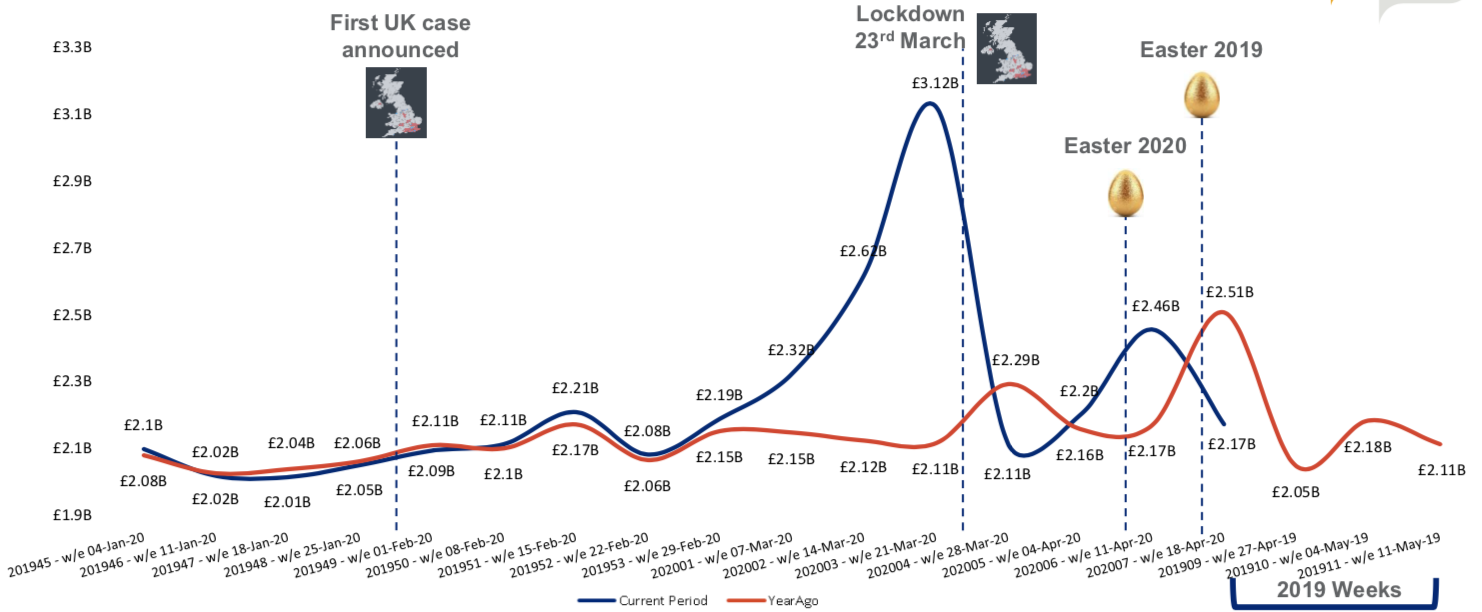

Weekly Retailer sales tracked as events proceeded

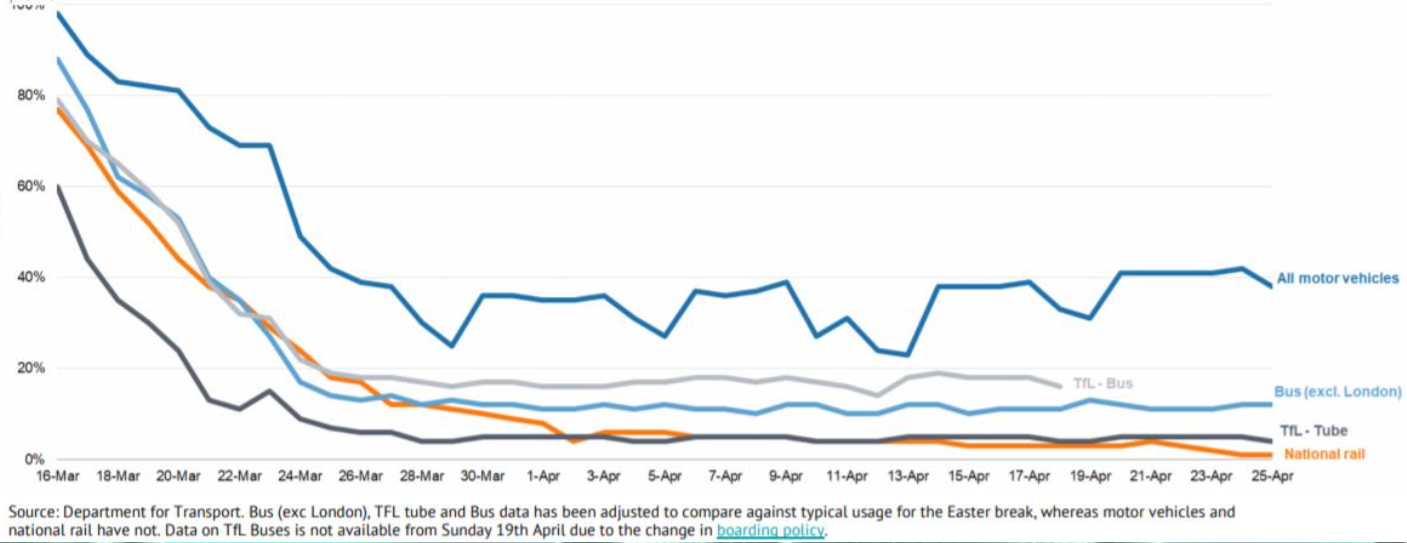

Transport usage change

Road traffic volumes on Saturday 25th April are 62% lower than the first week of February.

Traffic volumes on Saturday 25th April have shown a small increase of 5 percentage points compared to the previous Saturday.

Rail and tube use are down by more than 96%.

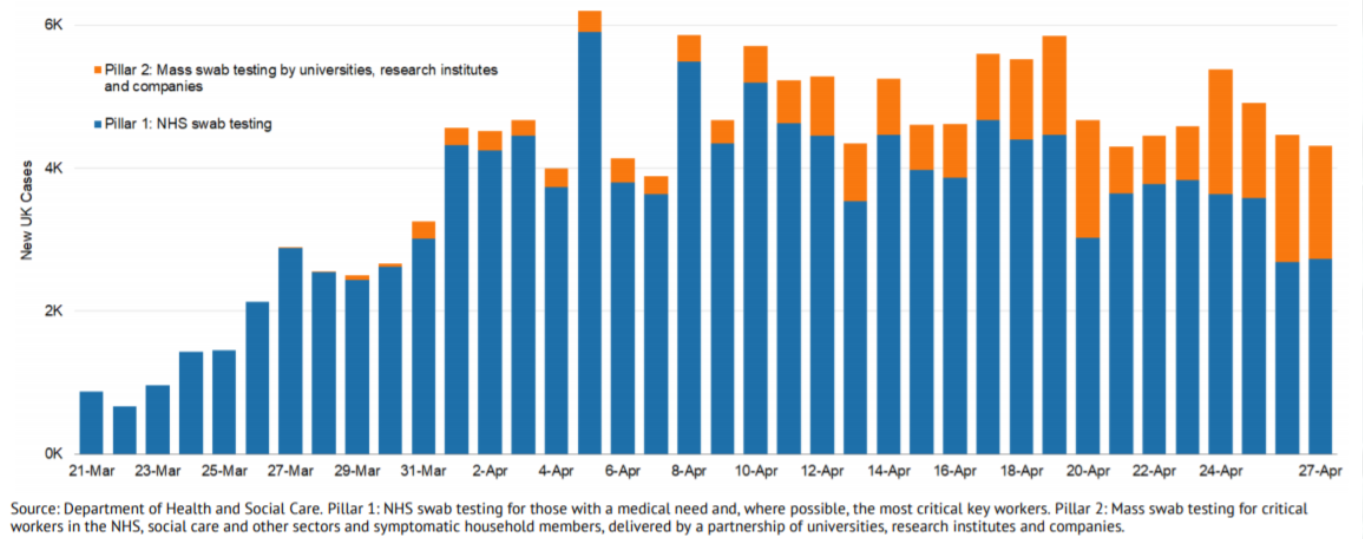

New cases (UK)

Cases are reported when lab tests are completed. This may be a few days after initial testing. While testing capacity is increasing, the number of cases has remained stable over the last 7 days, through there are likely many more cases than currently recorded here.

End of week 4 of the UK lockdown and the country’s restricted movement and strict 2m social distancing remains in place

Sales in the latest week are down vs last year due to Easter phasing but are ahead of the week that proceeded Easter in 2019

Source: IRI Retailer Advantage | Total Market | All Products | Latest Week (w/e 18/04/2020) | Value

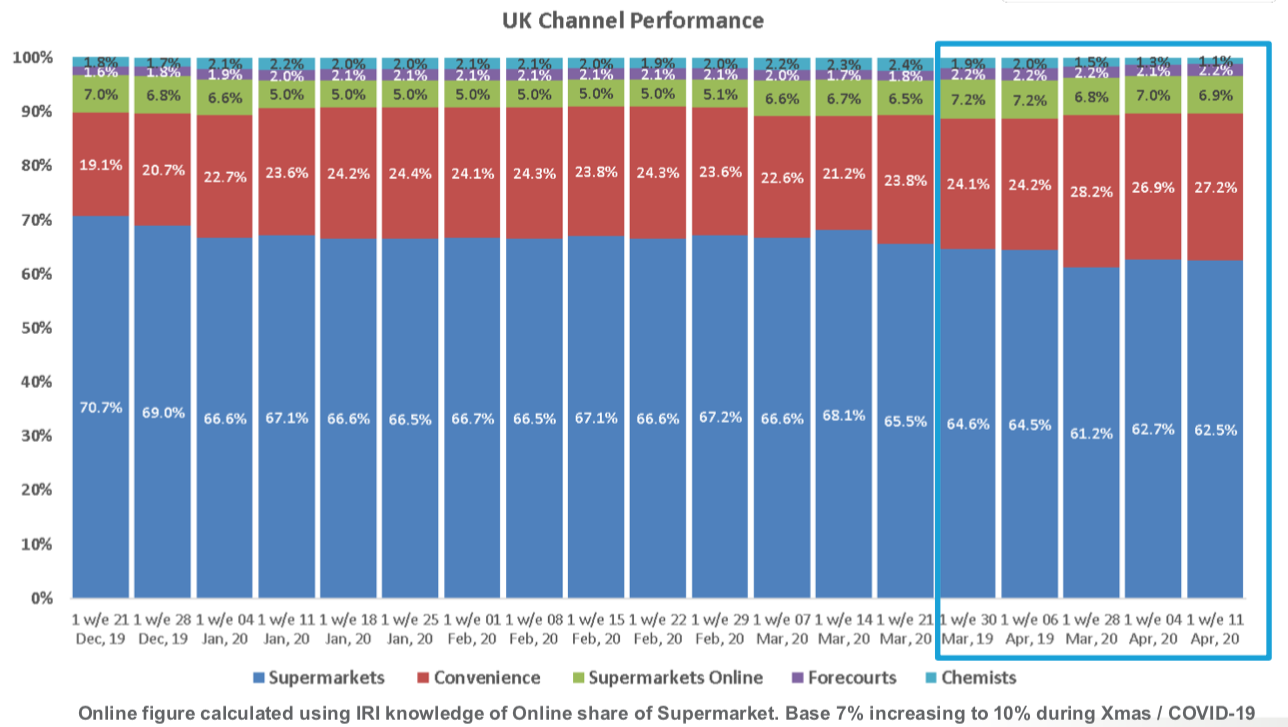

Convenience channel increases its importance in the UK retail environment as consumers purchasing habits evolve during lockdown.

Source: IRI Total Store | Total Market | Category | Latest Week (w/e 11/04/2020) | Value

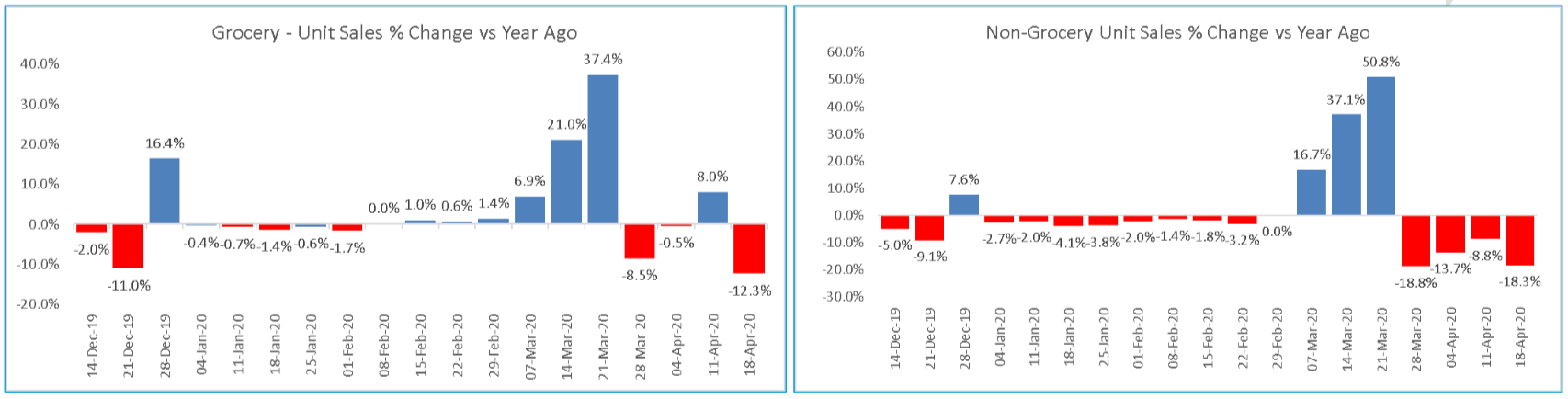

Easter 2019 drives latest weekly Grocery Unit sales down, whilst Non-Grocery Unit sales continue to decline

While deodorants, Personal Wash and Cleaning Products are in growth in Non-Grocery, the lockdown has meant many categories have become less relevant

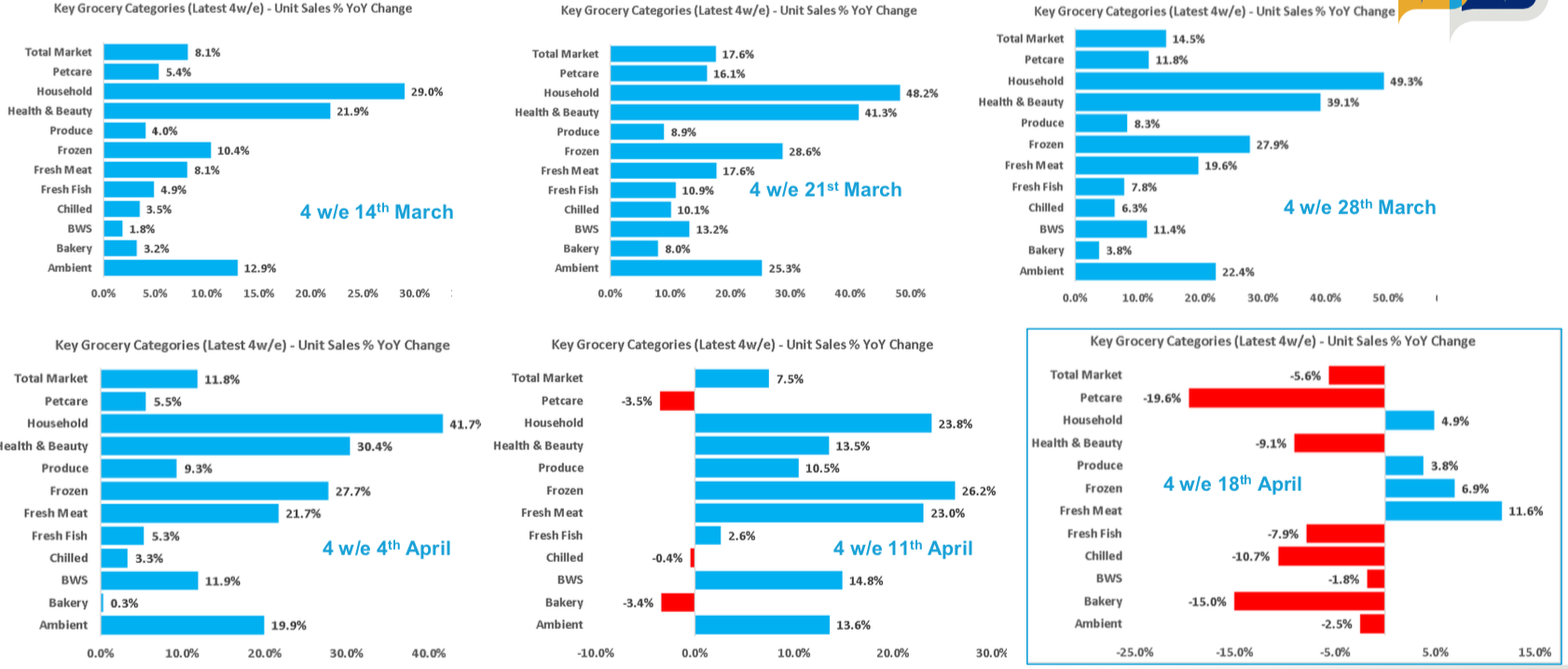

Source: IRI Retailer Advantage | Total Market | All Products | Latest 4w/e (w/e 18/4/2020) | Unit

In the latest weekly update of the 4w/e performance, with all categories in Unit sales decline in the latest week, this is impacting the overall performance

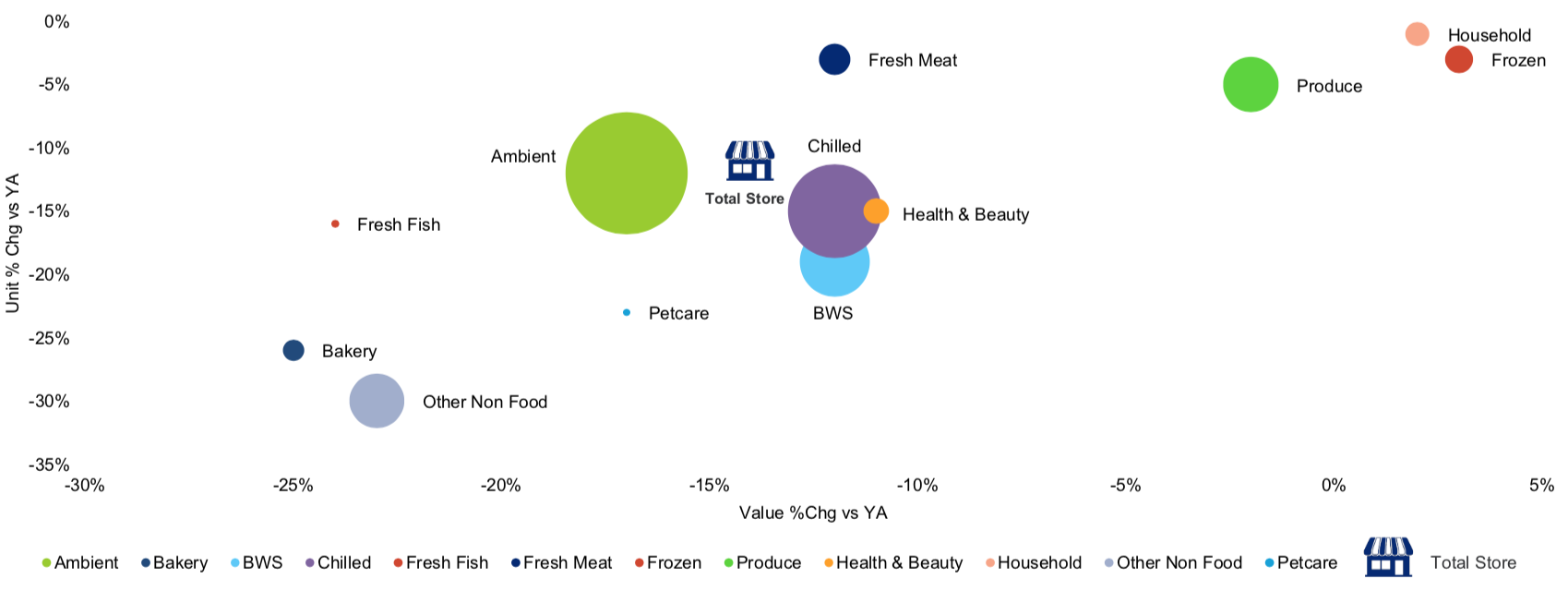

Only Household and Frozen in Value growth in the latest week when looking at Units and Value % Change

Size of bubble: Current Value Sales for week ending 18/04/2020

Source: IRI Retailer Advantage | Total Market | Department | Latest Week (w/e 18/04/2020) | Value & Unit % Change

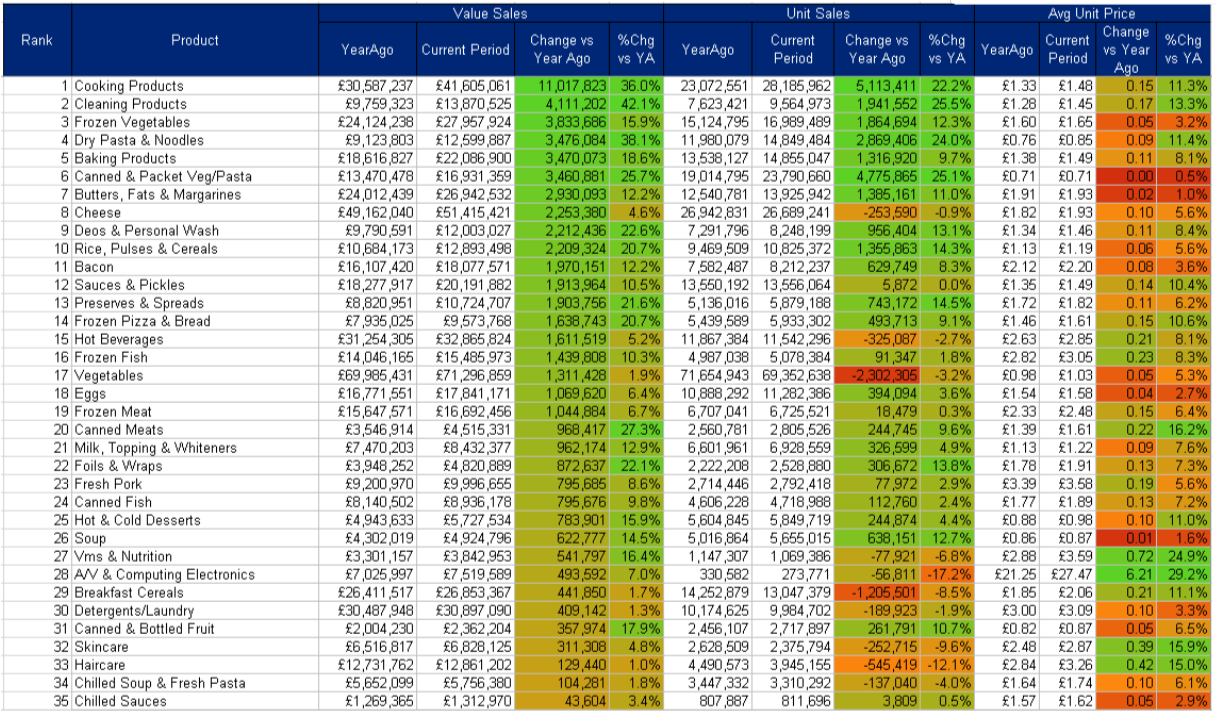

Top 70 Categories based on Value Change for the Latest Week

Source: IRI Retailer Advantage | Total Market | Category | Latest Week (w/e 18/04/2020) | Value, Unit, Avg Unit Price

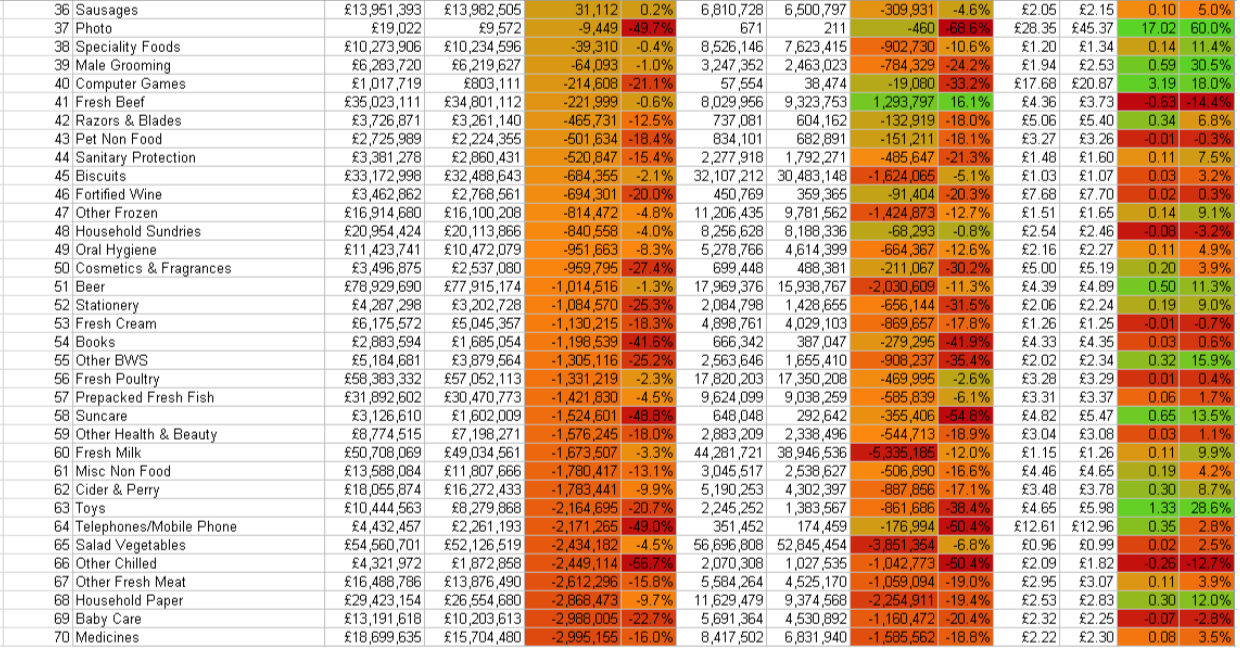

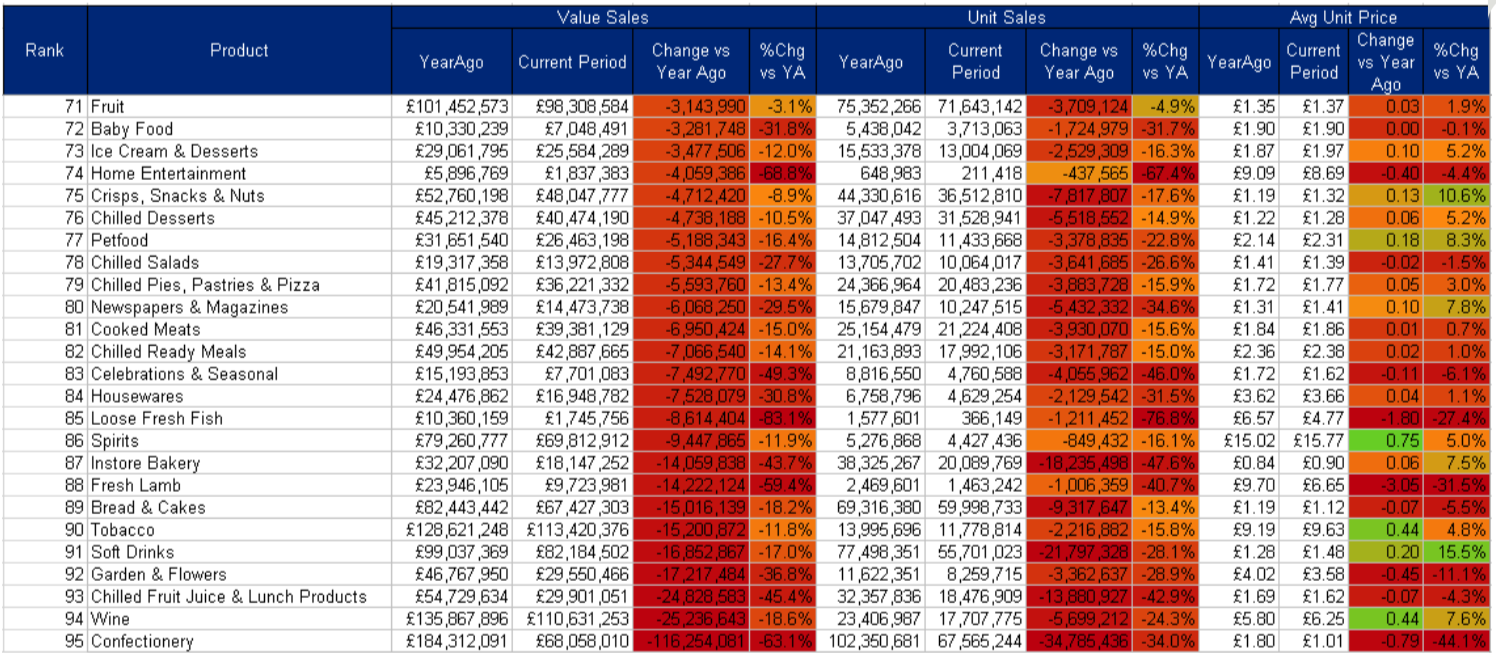

Bottom 25 Categories based on Value Change for the Latest Week

Source: IRI Retailer Advantage | Total Market | Category | Latest Week (w/e 18/04/2020) | Value, Unit, Avg Unit Price

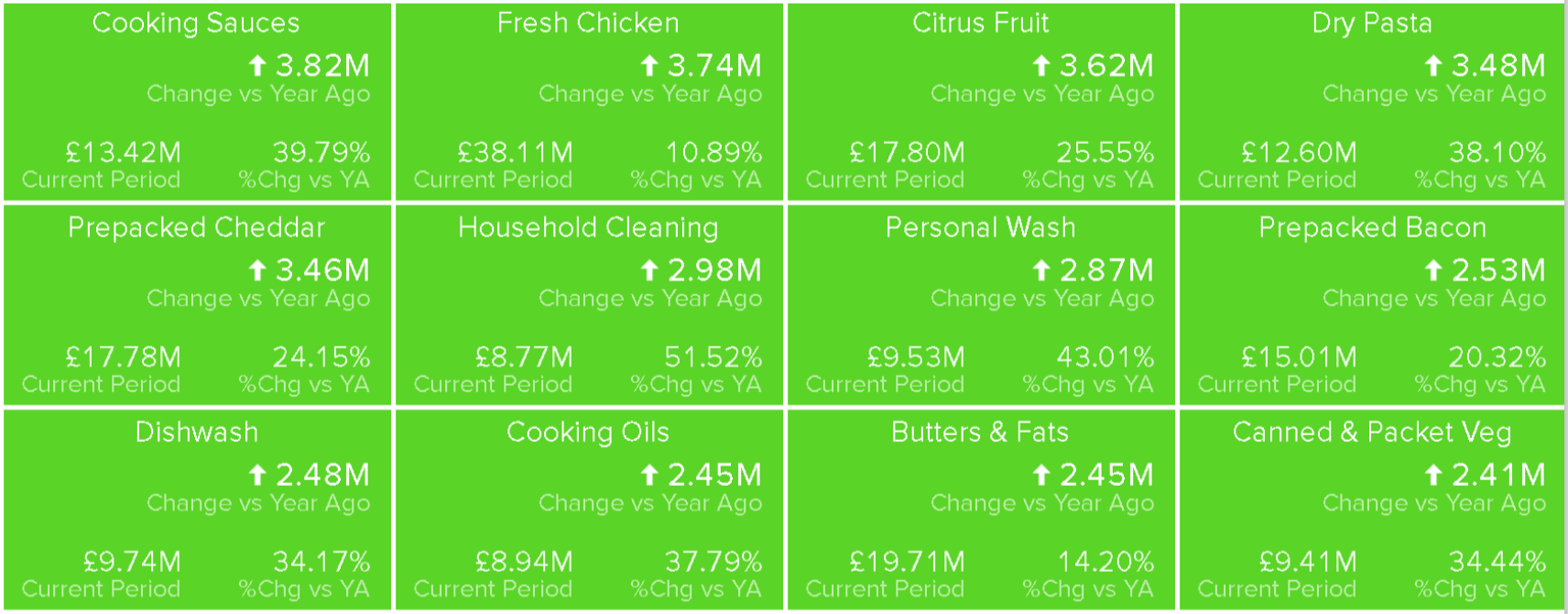

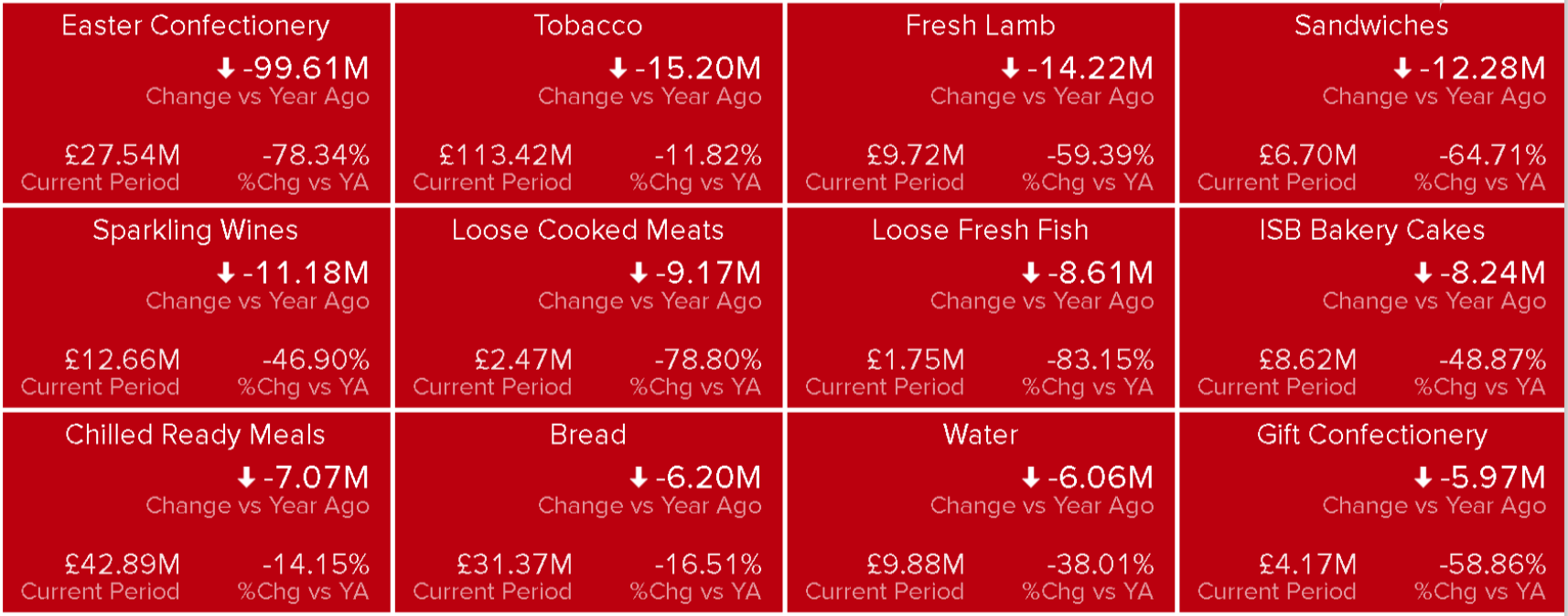

Top 12 categories, and 12 sub-categories

Ambient categories feature heavily in this week’s Top 12 Sub-categories based on Actual Value Change as people continue to eat in during lockdown. Easter phasing drives the decline in Easter Confectionary however lunchtime occasions continue to feature in the Sub Categories seeing the greatest decline.

Source: IRI Retailer Advantage | Total Market | Sub-Category | Latest Week (w/e 18/04/2020) | Value

Implications for CPG Manufacturers

Demand Planning / Supply Chain

- Adjust production to consumer demand shocks and potential short term and long-term scenarios. Consumers may demand more for health prevention and cleaning in the short term, and may reduce demand for some categories like cosmetics and haircare as consumers work from home and restrict socializing.

- Account for potential of weak Easter season, as social distancing takes hold. Seasonal meals might be off the table, sales of seasonal confectionery treats may suffer.

- Consider role in and demand for “fun” products and engagement strategies as consumers spend more time at home and stress levels increase.

- For impulse categories, determine ways to trigger demand online, as shoppers reduce in-store visits.

- Review and plan for likely supply-chain impacts, especially for raw materials that originate in China and other highly impacted countries. As the impact of shuttered facilities takes hold, shortages and logistical bottlenecks will become an issue.

Marketing

- Consider shifting advertising to social and digital channels (vs. out of home) as consumers shift their entertainment hours to sources they can access from home.

- Keep a close pulse on consumer sentiment and adjust communications accordingly.

- Assess long-term impact to consumer behaviour and brand perceptions after crisis, e.g., potential negative

perceptions of brands brought during the pandemic, etc.

Channel / Distribution

- Prepare for a dramatic increase in online demand, particularly within pure-play and home delivery, but click & collect will also jump substantially; may have a lasting effect post-crisis.

- Closely monitor impact to the Convenience channel, which will likely be negatively impacted by more consumers working from home and less travel, as well as Foodservice, which will be challenged by “cocooning” but can partially combat with frictionless delivery.

Merchandising

- Determine appropriate promotion and pricing strategy to balance consumer demand changes, perception of brand during the crisis, and impact of increased supply costs.

Implications for CPG Retailers

Inventory Planning

- Closely plan inventory and monitor out-of-stocks in high-demand categories (e.g., cleaning, preventive health, sports drinks) by geography by phase of COVID-19 impact.

- Anticipate drop in sales of stock-up items as replenishment will take time.

- Plan for potential weakness across Easter holiday categories, particularly holiday meal items as shoppers may forgo large family celebrations.

Merchandising

- Assure shoppers that the items they need are available, including placement of high-demand items in front lobby displays and circulars.

- Explore co-promotion and co-display opportunities across high-demand categories.

- Plan for a potential economic downturn by altering promotions (e.g., more at the beginning of the month), stocking more opening price point items, etc.

- Consider value and pricing proposition vs. competition as some retailers may invest more in lower prices to attract customers.

Shopping Experience

- Communicate plans in place to ensure cleanliness of store (e.g., paid leave for sick workers, availability of free hand sanitiser for shoppers etc.) and alleviate customer worries about visiting the store.

- Ensure seamless online experience and ramped-up fulfilment capabilities as home delivery and click & collect rapidly accelerate.