This report contains:

- Summary of UK Performance

- UK update on COVID-19

- Total Market Overview

- Additional Support from IRI

- IRI White paper

- IRI Global Demand Index

Summary of UK Performance

- End of the 26th week of the UK lockdown and whilst Brexit causes concerns, the recent increase in COVID-19 cases in the UK are driving the performance of the FTSE 100. With the imminent increase in lockdown restrictions , there is the potential to see an increase in sales as consumers are advised to minimise contact with other people to slow the spread

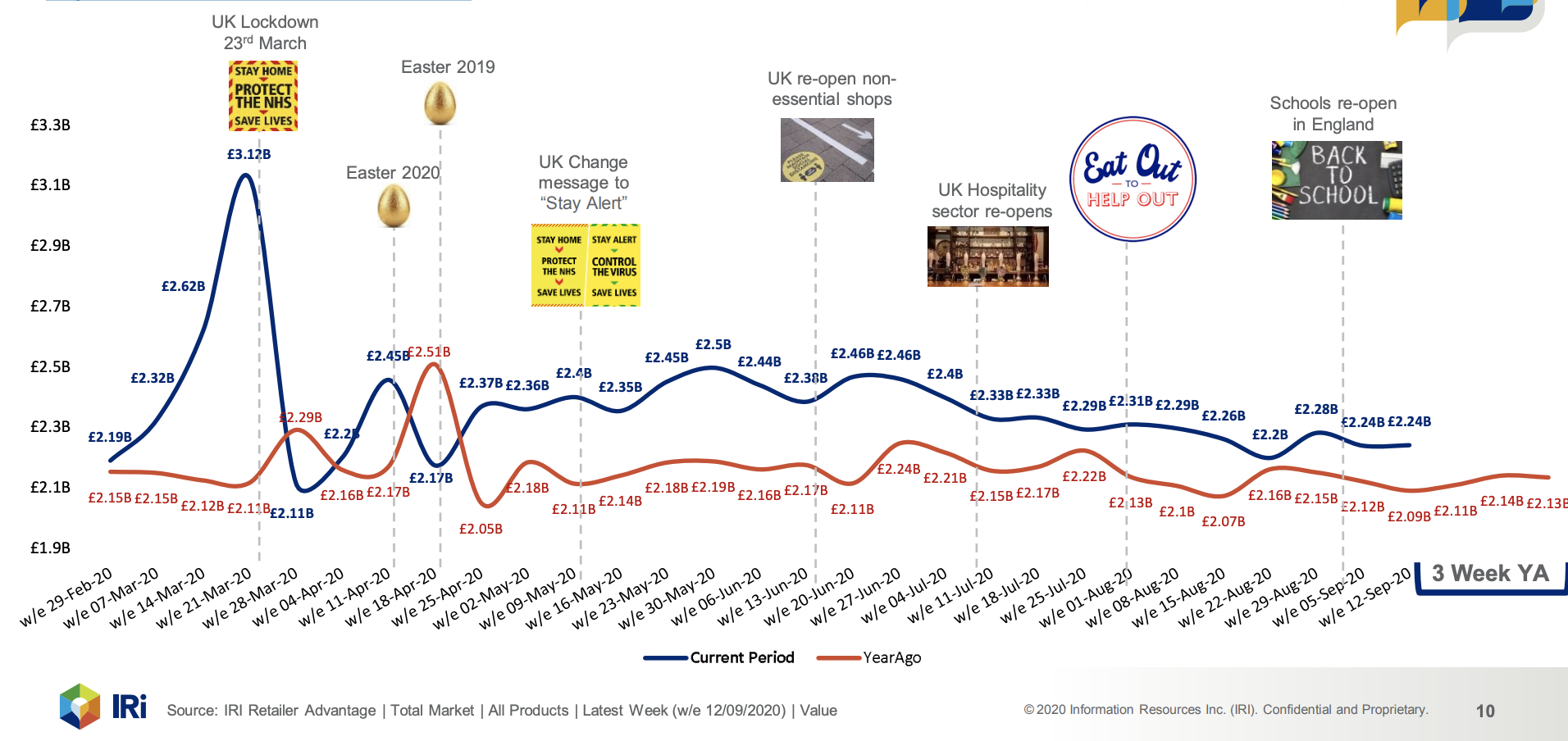

- In the latest week, sales reached £2.24b; £151m higher than the same time last year and in line with last weeks’ sales

- This week’s sales had no major events to report other than a full week of children returning to schools, however we have seen increased restrictions come into place, these may help maintain retailer sales momentum

- Of the additional £151m spent in the latest week, this was driven by an increased Grocery spend of £121m and £30m in Non Food

- Current UK COVID-19 Alert Level has increased to 4, to signify an "epidemic is in general circulation; transmission is high or rising exponentially. Impact of potential government response to UK Retailer sales will be known in 2 weeks

- Whilst there is evidence of a slowdown across both Value and Unit sales, the recent weekly sales growth indicates it may be a while before we return to normal levels

- The Convenience and Online Channels have both benefitted from changing consumer shopping habits however in the latest data, Convenience figures show it accounts for 23.9% of Total sales similar to pre-COVID-19 figures

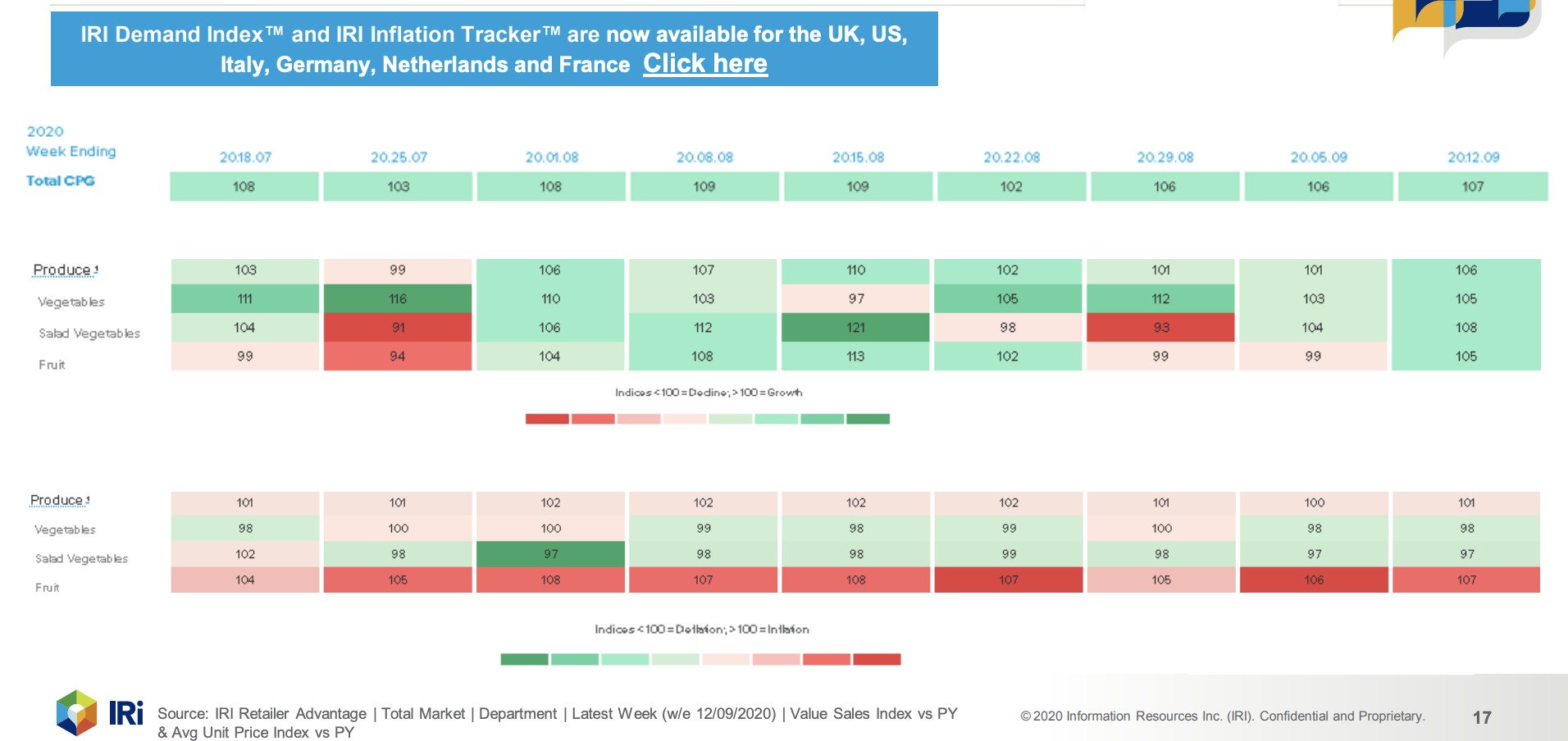

- IRI’s Inflation Tracker shows the level of inflation in Produce is behind all departments as we have seen Supermarkets focus on price cuts to benefit consumers, notably in Vegetables and Salad Vegetables

Total Market Sales Value

In the latest week, sales reached £2.24b which is £151m higher than last year and in line with last week’s sales. This week’s sales had no major events to report other than a full week of children returning to schools, however we have seen increased restrictions come into place, these may help maintain retailer sales momentum.

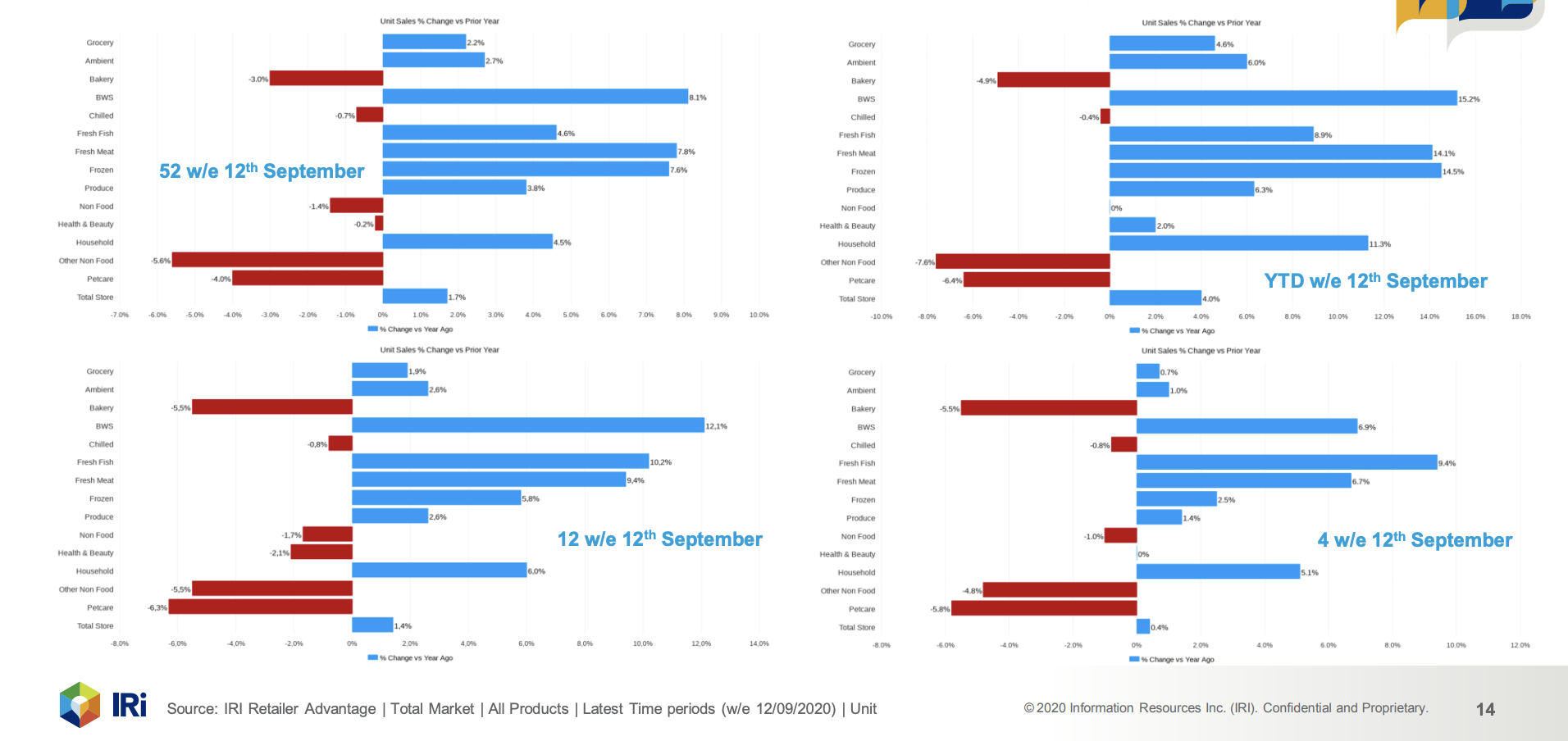

Total Store Unit sales growth in the latest 4 w/e is +0.4% however this has slowed compared to YTD which is +4.6% higher than last year.

Focus on Produce – Interestingly the level of inflation in Produce is behind all departments as we have seen Supermarkets focus on price cuts to benefit consumers, notably in Vegetables and Salad Vegetables.

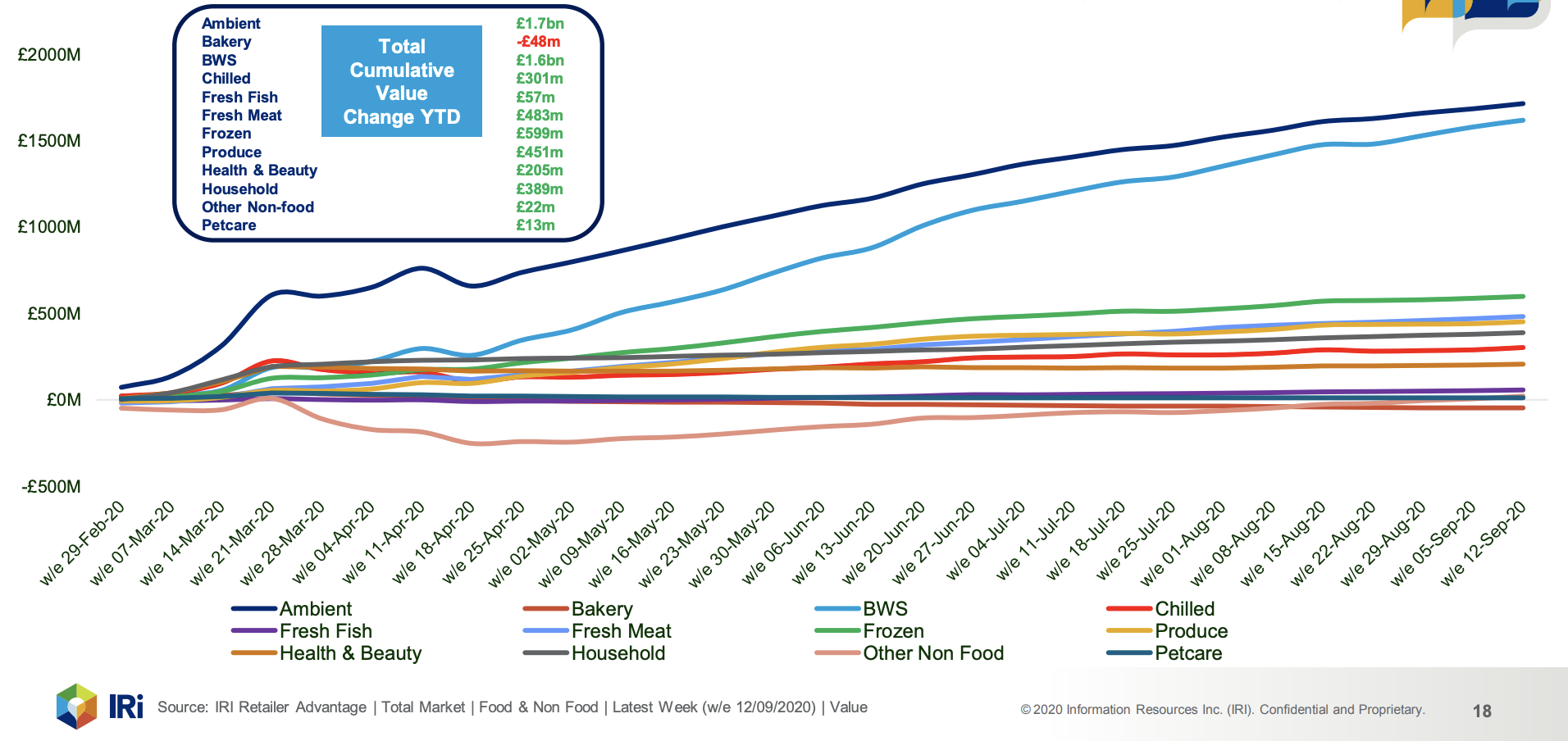

Since the beginning of 2020 and predominantly since the start of COVID-19, UK Retailer sales are £5.808b higher than last year, driven by Ambient (+£1.7b) and BWS (+£1.6b).

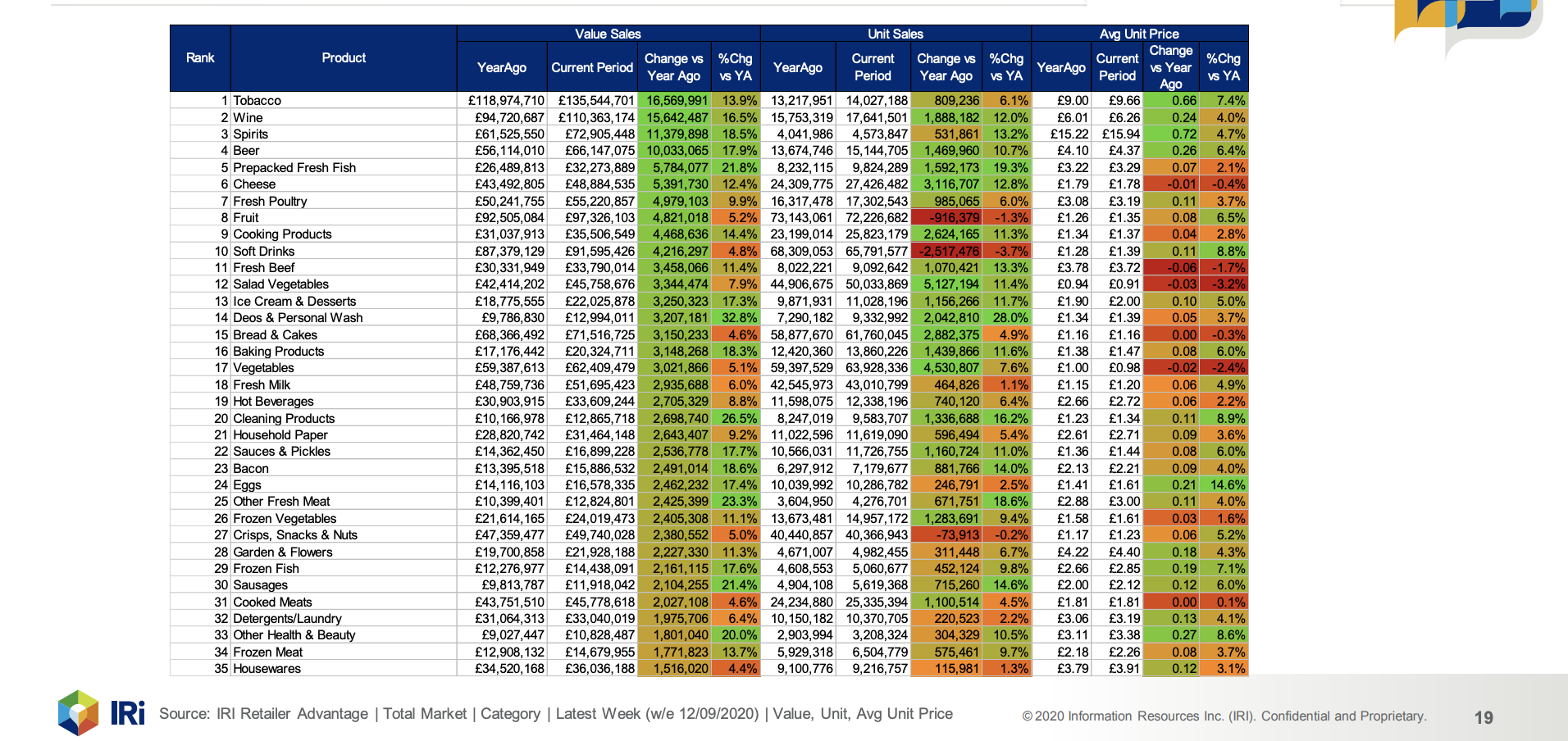

Top 35 Categories based on Value Change for the Latest Week.