We know that information is vital during the current COVID-19 crisis to help fire up the engines of business, so we thought it would be helpful to share some insights from our IRI colleagues from around the world on the Impact of the Coronavirus on the FMCG industry, in the UK, Spain, Germany and New Zealand.

Key highlights are shown in this post, but download the full report for:

- Summary of UK performance

- UK update on COVID-19

- The new normal that FMCG Retailers and manufacturers anticipate

- An appendix with further details on the impact in:

- Spain

- New Zealand

- Germany

- Greece

Summary of UK performance

- UK lockdown entering 9th week and new restrictions come into effect 13th May

- In the latest weekly data to 9th May, which includes the recent VE day Bank Holiday Friday, sales reached £2.4b; £286m higher than the same time last year

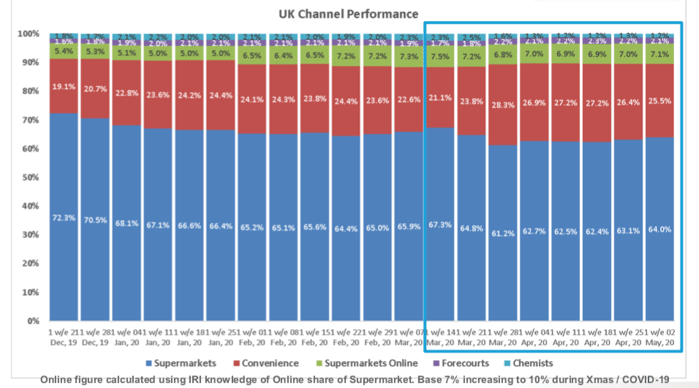

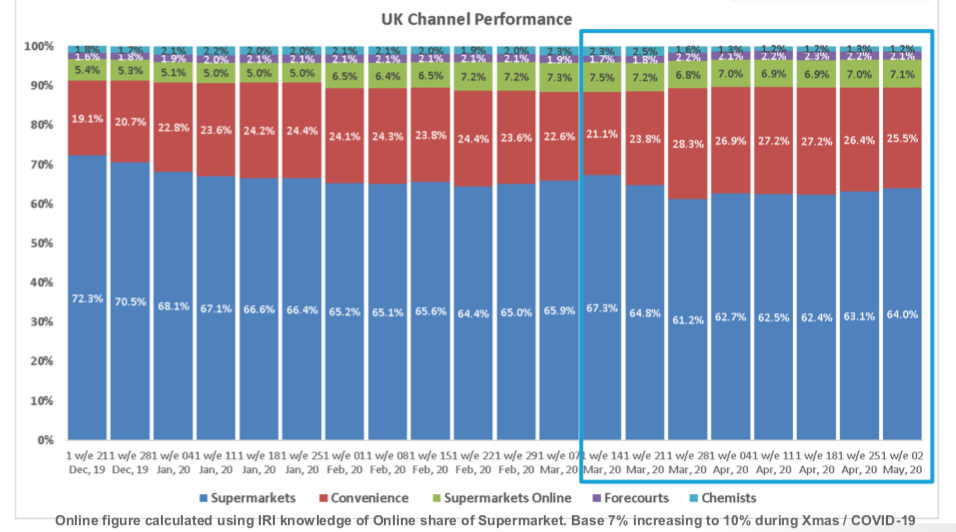

- Convenience & Online channels increase their importance in the UK retail environment as consumers purchasing habits evolve during lockdown.

- Whilst Total Market Value sales are in growth, only Grocery continues to grow in Unit sales growth as Non-Grocery sales maintain it’s decline

- The additional £286m Total Store sales is +13.6% vs year ago and is driven by an increased Grocery spend of £265m

- BWS, Ice Cream and Fresh Meats continue to feature in the top growing Sub-Categories as the Bank Holiday and On-Trade closure drive demand.

- The panic buying around Toilet Tissue, Laundry Detergents and Baby Milk appears to be impacting performance and they join Food to Go, In-Store Bakeries and Water in the sub categories seeing the greatest decline

UK impact and implications

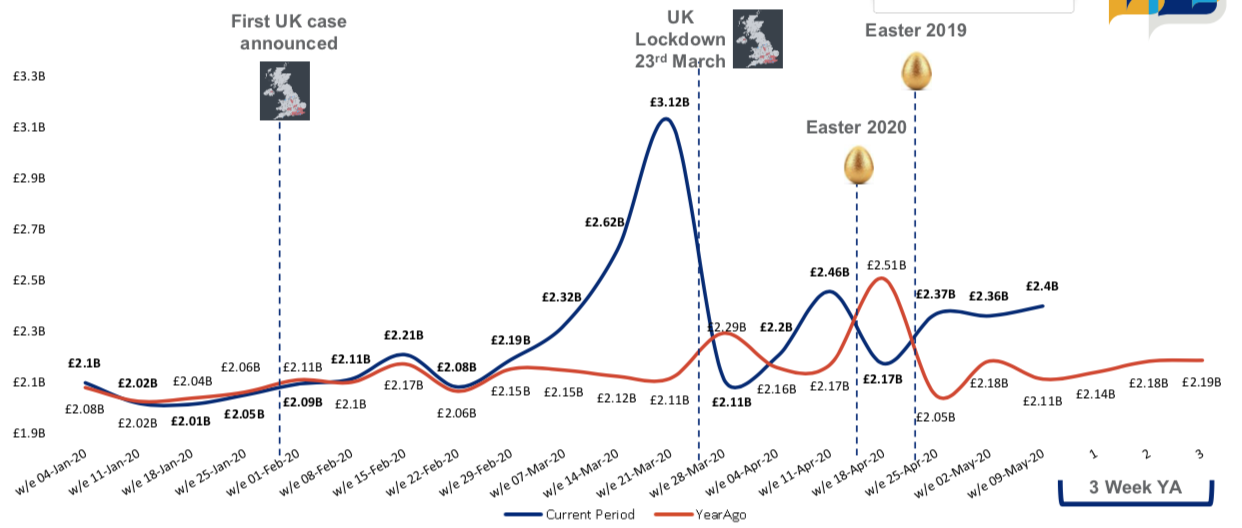

- First case in the UK was on the 31st January 2020 from someone that had recently returned from mainland China

- As of 9am on 18th May 2020, 1,887,051 people have been tested, of which 246,406 were confirmed positive. As of 5pm on 17th May 2020, of those tested positive across all settings in the UK, 34,796 have sadly died.

- The UK remains in Delay stage with Coronavirus spreading and a global pandemic continues

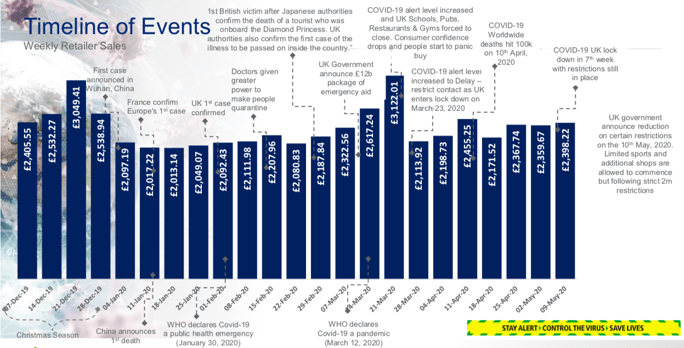

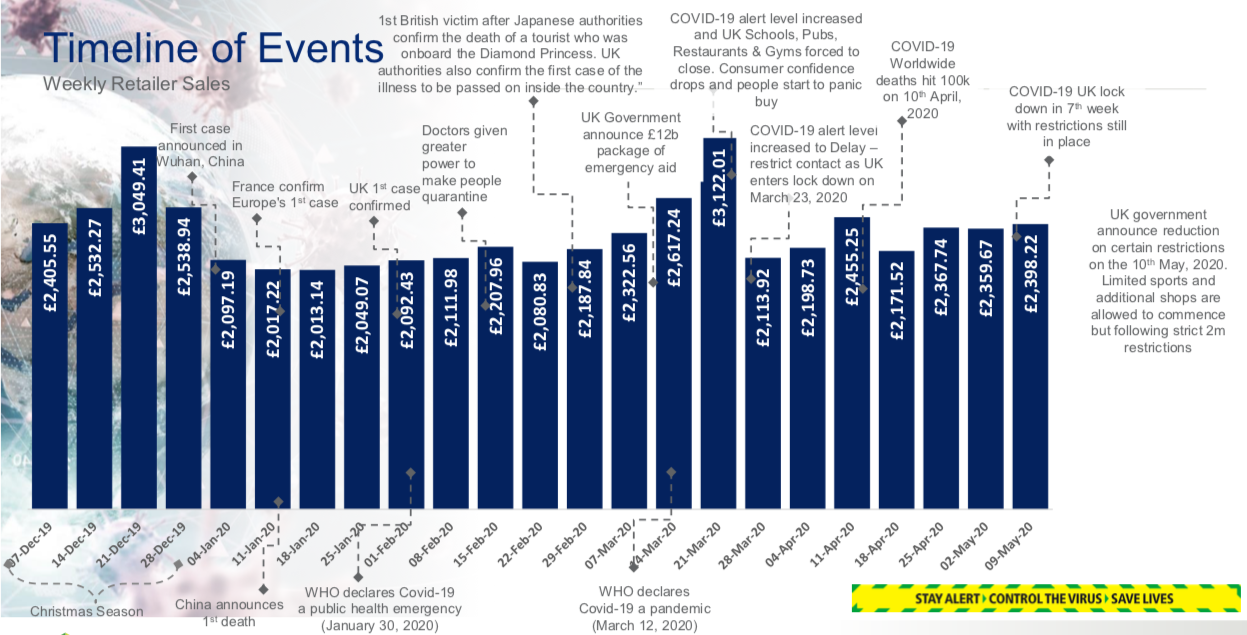

Timeline of events

Source: IRI Retailer Advantage | Total Market | All Products | Latest Week (w/e 9/05/2020) | Value

While we can review past events...

COVID-19 Is a Crisis Like No Other

While we can learn from past recessions and crises, COVID-19 is unique in that it has changed the day-to-day existence of nearly everyone.

Source: IRI US Analysis

Source: IRI US Analysis

End of week 8 of the UK lockdown and the changes in England start to be implemented. The strict 2m social distancing remains in place which industries have to work around

Total Market Value Sales – In the latest week, which includes the recent VE day Bank Holiday Friday, sales reached £2.4b; £286m higher than the same time last year

Source: IRI Retailer Advantage | Total Market | All Products | Latest Week (w/e 09/05/2020) | Value

Convenience & Online channels increase their importance in the UK retail environment as consumers purchasing habits evolve during lockdown.

Source: IRI Total Store | Total Market | Category | Latest Week (w/e 02/05/2020) | Value

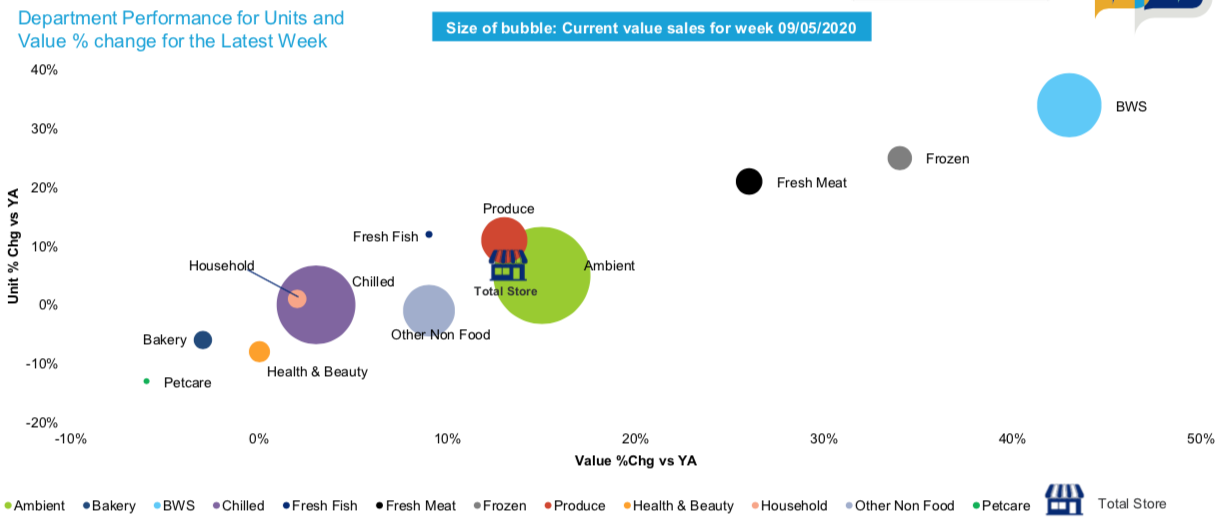

BWS, Frozen and Fresh Meat sales continue to drive greatest growth across both Unit and Value. Petcare and Bakery continue to be impacted with declines across both Unit and Value

Source: IRI Retailer Advantage | Total Market | Department | Latest Week (w/e 09/05/2020) | Value & Unit % Change

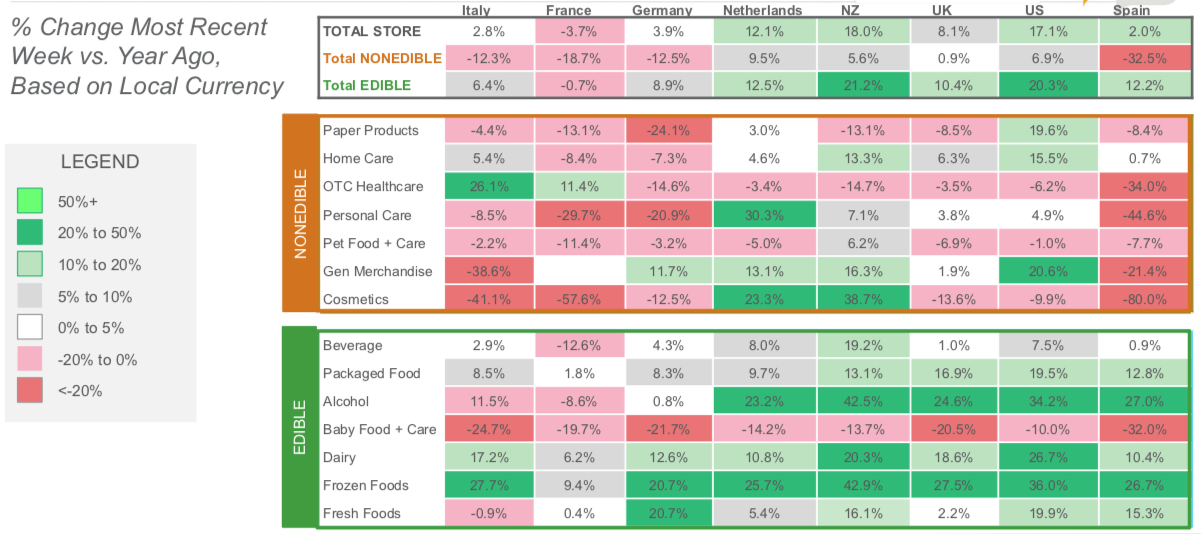

UK following a similar trend across the markets with growth in Edible and slower growth or declining sales in Non-Edible

Source: IRI POS data Week Ending May 3, 2020 vs. year ago / Note: Exact product categorization varies slightly by country

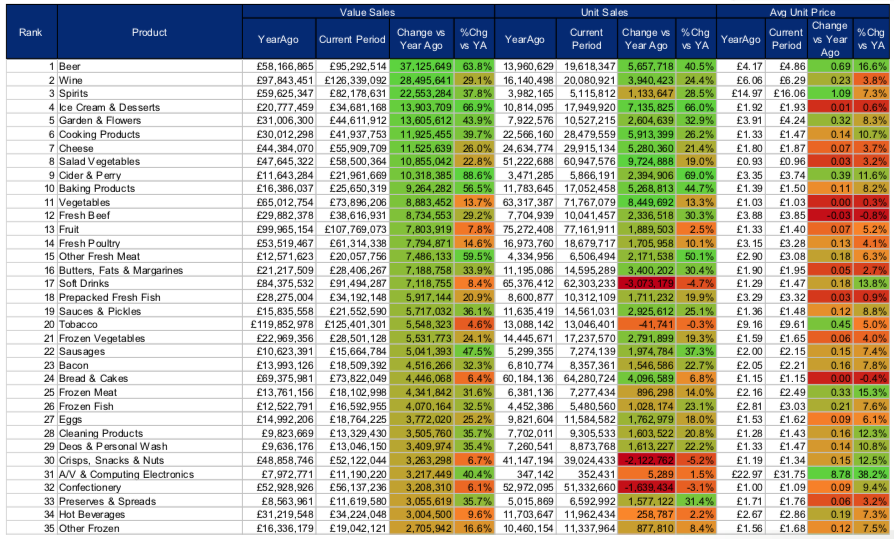

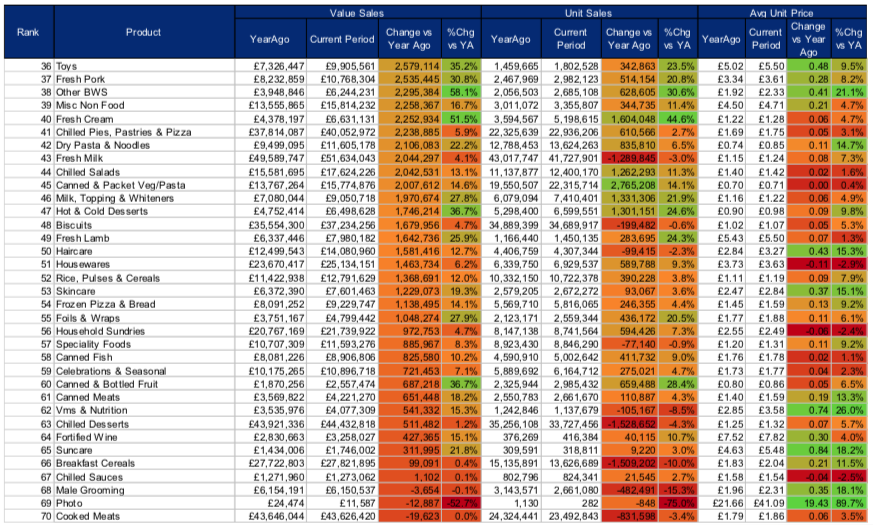

Top 70 Categories based on Value Change for the Latest Week

Source: IRI Retailer Advantage | Total Market | Category | Latest Week (w/e 09/05/2020) | Value, Unit, Avg Unit Price

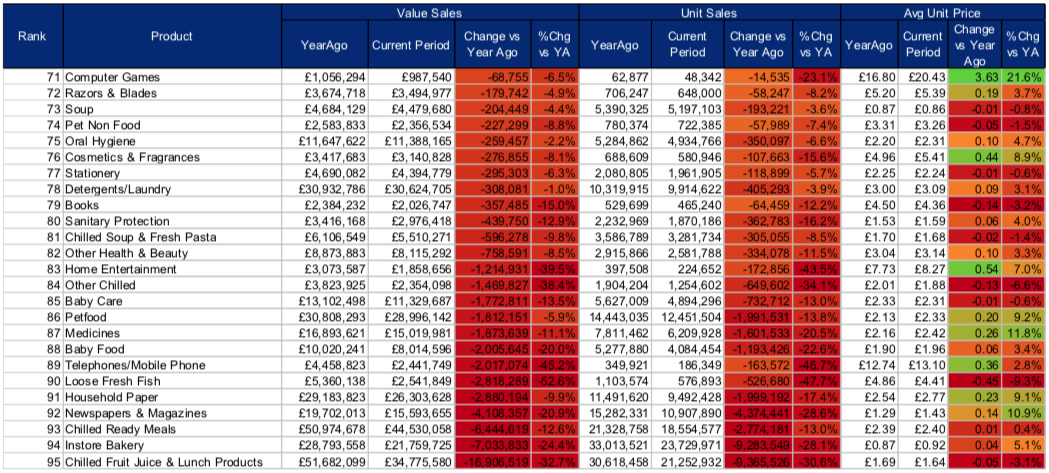

Bottom 25 Categories based on Value Change for the Latest Week

Source: IRI Retailer Advantage | Total Market | Category | Latest Week (w/e 09/05/2020) | Value, Unit, Avg Unit Price