This report contains:

- Summary of UK Performance

- UK update on COVID-19

- The new normal that FMCG retailers and manufacturers expect after COVID-19

- Appendix: Focus on:

- Spain

- Greece

- New Zealand

SUMMARY OF UK PERFORMANCE

- End of the 18th week of the UK lockdown and the FTSE 100 drops as markets concerned over longer term impact on economy with suggestions it could take till 2024 for the UK to return to pre-COVID-19 levels

- In the latest week, sales reached £2.33b; £163m higher than the same time last year and in line with last weeks sales +0.1%

- Sales are +7.5% higher on the same time last year and the reopening of the hospitality sector does not appear to have impacted Grocery sales… so far

- Of the +7.5% growth in Total Store sales vs year ago, Grocery sales increased +8.8% and Non Food +3.4%

- Of the additional £163m spend in the latest week, this was driven by Grocery +£146m and +£17m in Non Food

- Since the beginning of 2020 and predominantly since the start of COVID-19, UK Retailer sales are £4.704b higher than last year, driven by Ambient (+£1.4b) and BWS (+£1.3b) departments

- Tobacco, BWS, Fresh Meats/Fish, First Aid (Face Masks) and Personal Wash feature in the top growing SubCategories

- UK Lockdown measures continue to impact the demand for Food to Go categories; Sandwiches, In-Store Deli’s, Water and Newspapers

- The Convenience and Online Channels have both benefitted from changing consumer shopping habits however in the latest data, Convenience figures show it accounts for 24.8% of Total sales similar to pre-COVID-19 figures

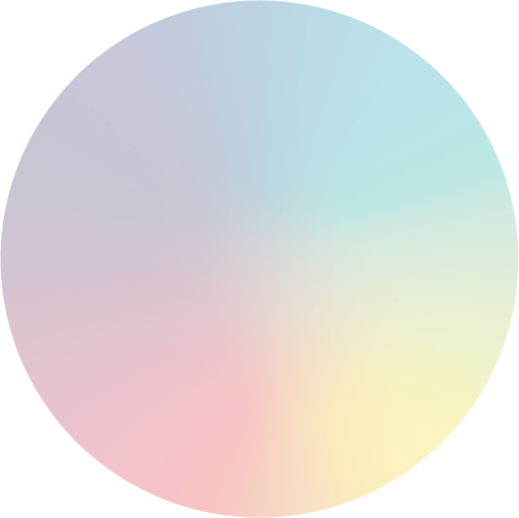

TIMELINE OF EVENTS

End of the 18th week of the UK lockdown and the FTSE 100 drops as markets concerned over longer term impact on economy with suggestions it could take till 2024 for the UK to return to pre-COVID-19 levels

- FTSE 100 fell in the latest week as investor braced for disappointing economic updates

- UK retail sales were near pre-lockdown levels in June, as the reopening of shops released pent-up demand

- Forecasters are warning the UK economy could take until 2024 to return to the size it was before lockdown. Analysis from the EY Item Club, which uses a similar economic model to the Treasury, suggests unemployment will rise to 9% from 3.9%.

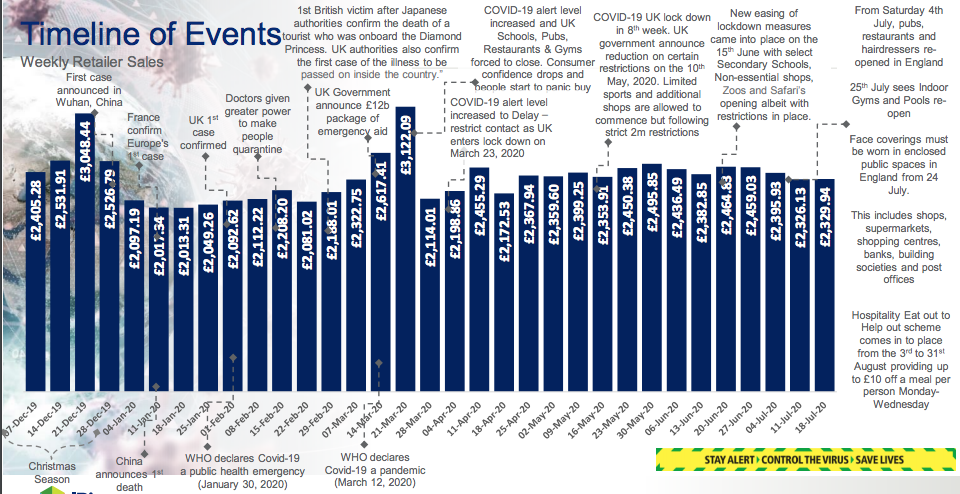

Total Market Value Sales – In the latest week, sales reached £2.33b which is £163m higher than last year. Sales are +7.5% higher on the same time last year and the reopening of the hospitality sector does not appear to have impacted Grocery sales… so far

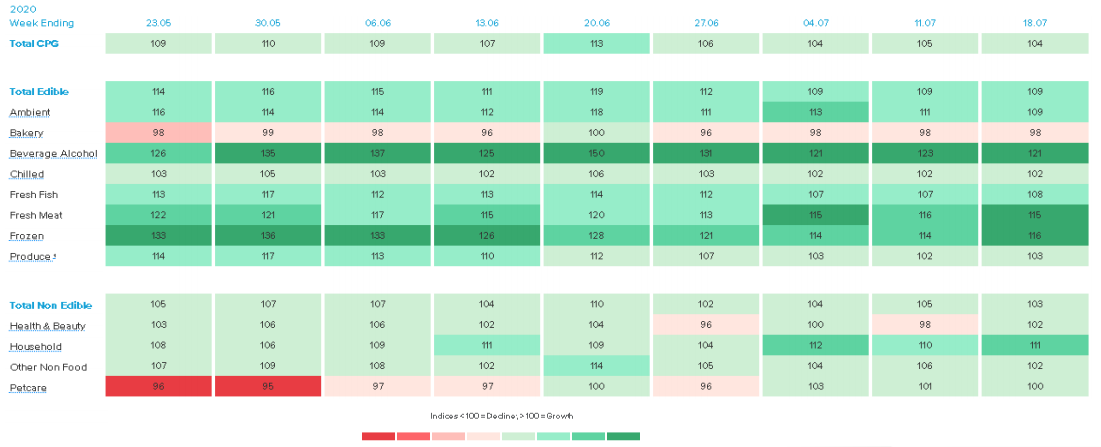

IRI’s Demand Index sees Bakery as the only department indexing down vs last year in Value sales with Total CPG at 104

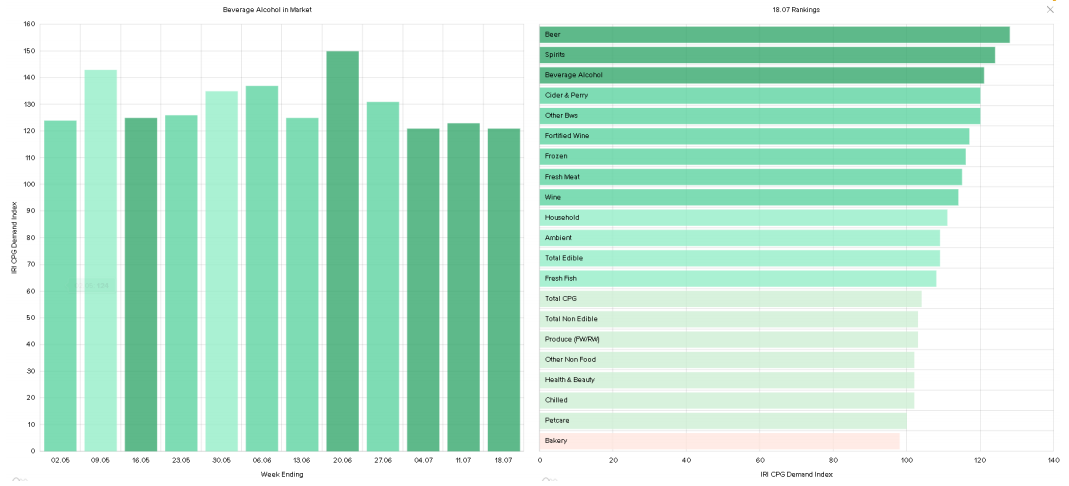

Focus on BWS – recent Demand Index level has remained static around 120 and all BWS Categories are delivering growth ahead of last year particularly Beer, Spirits and Cider/Perry

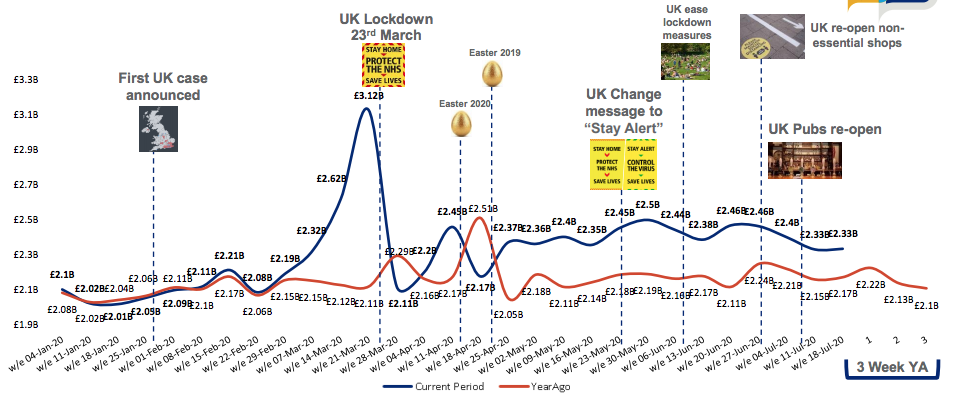

Top 35 Categories based on Value Change for the Latest Week