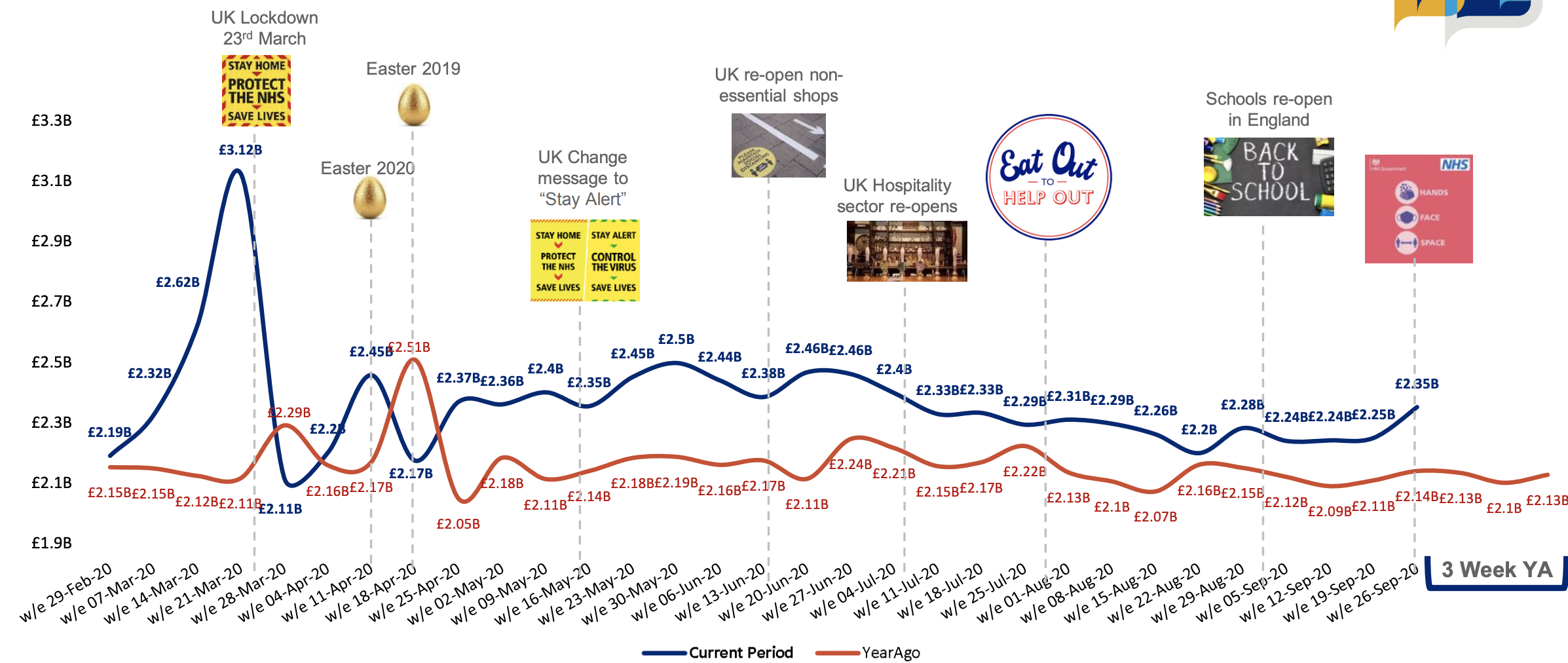

In the latest week, sales grew 4.5% on last week’s sales to £2.35b which is £211m higher than last year. The recent increases in COVID-19 cases and subsequent increased government restrictions being put in place have meant sales have increased; notably Toilet Tissues which grew 85% on last year and 59% on last week’s sales.

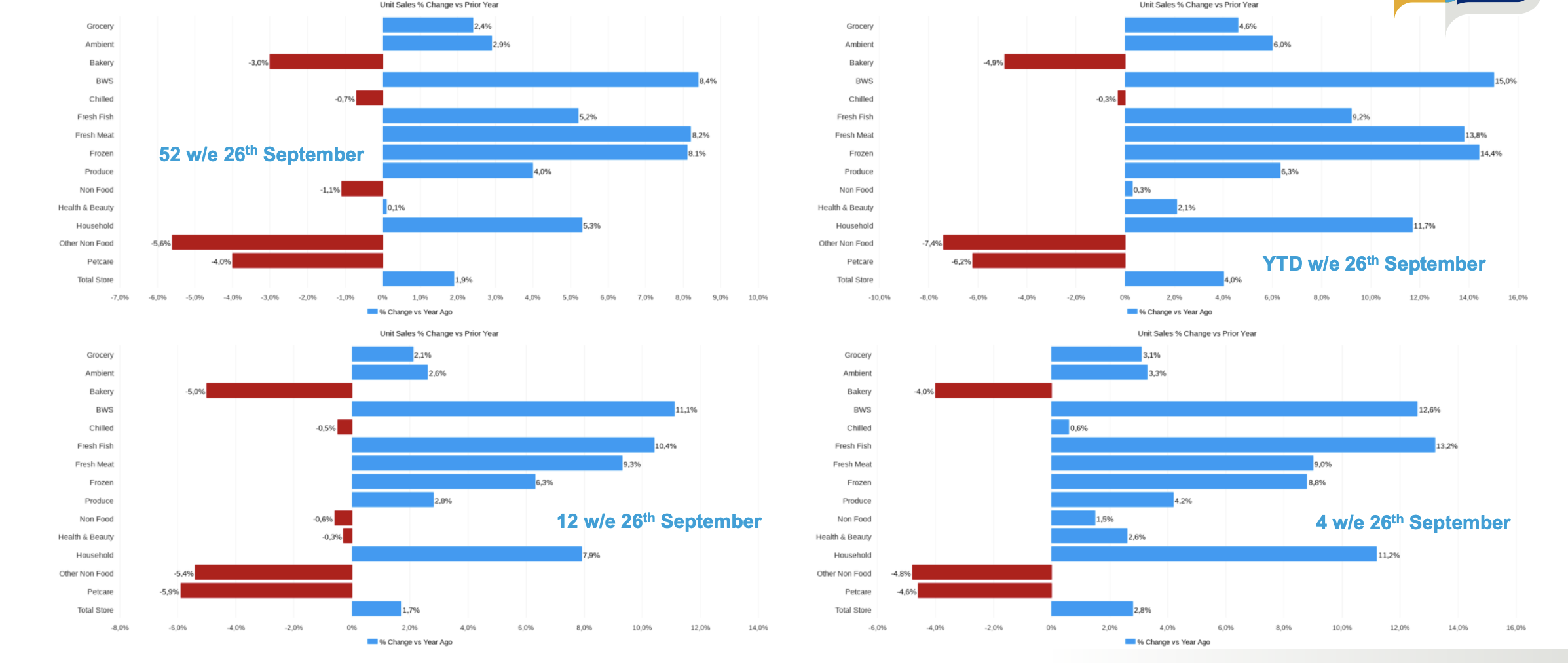

Total Store Unit sales growth in the latest 4w/e is +2.8% and has increased vs the latest 12w/e highlighting the growing signs of a 2nd wave, although not to same level as seen in March.

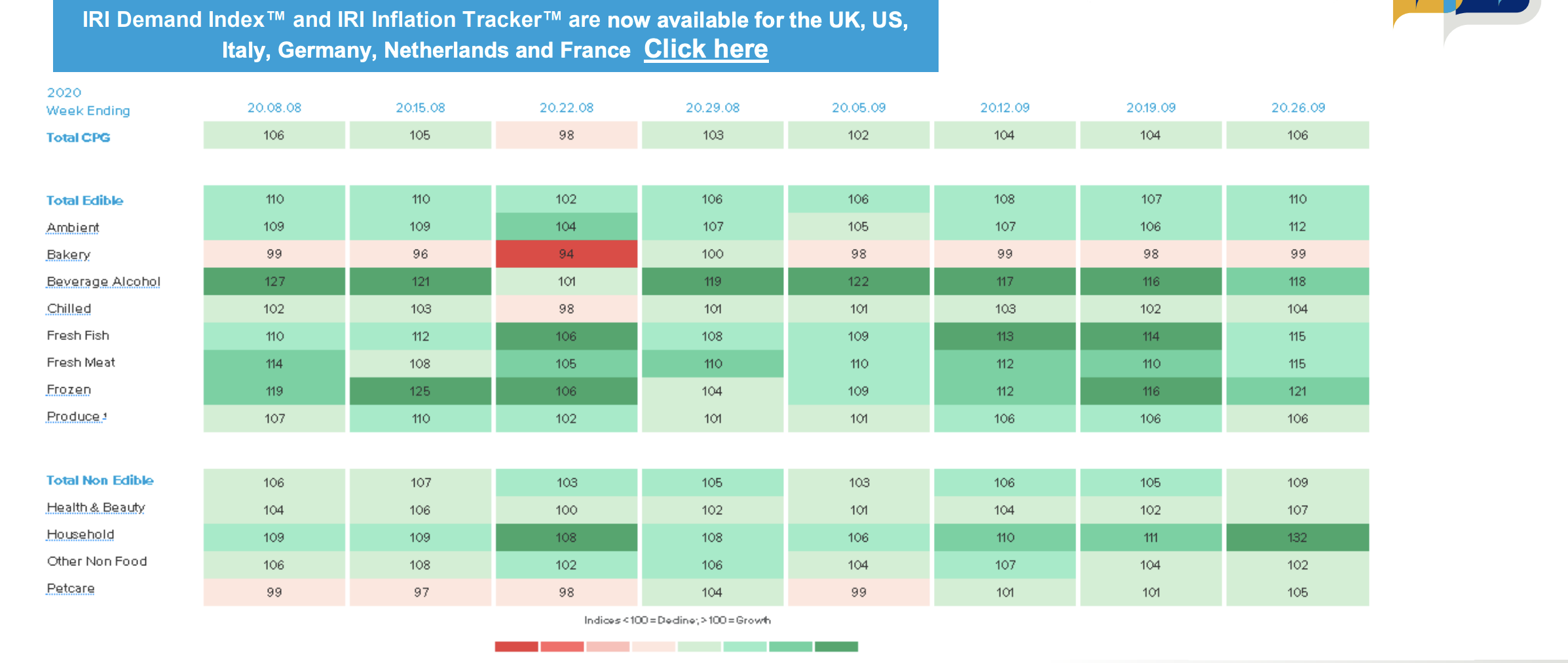

The recent increases in UK COVID-19 cases and subsequent increased government restrictions being put in place have meant demand for CPG products have increased.

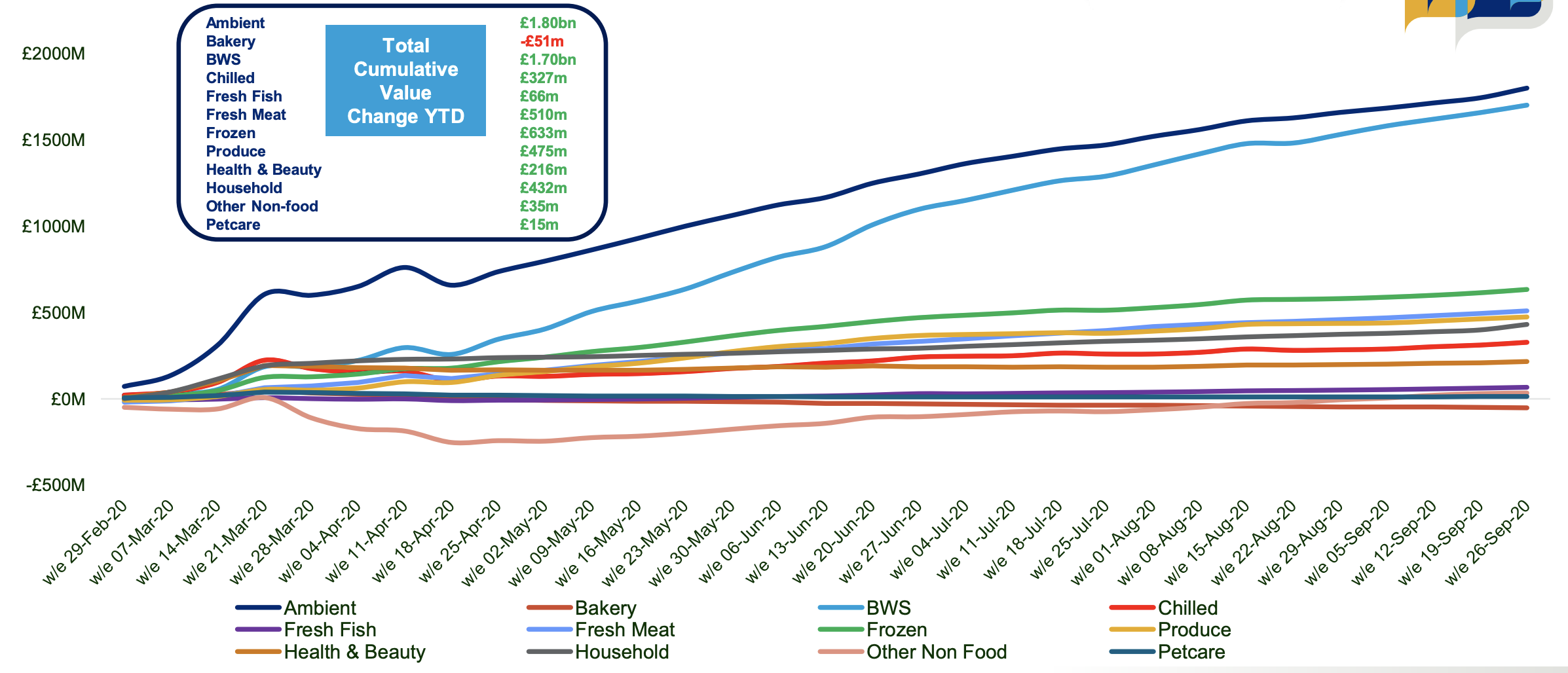

Since the beginning of 2020 and predominantly since the start of COVID-19, UK Retailer sales are £6.160b higher than last year, driven by Ambient (+£1.80b) and BWS (+£1.70b)

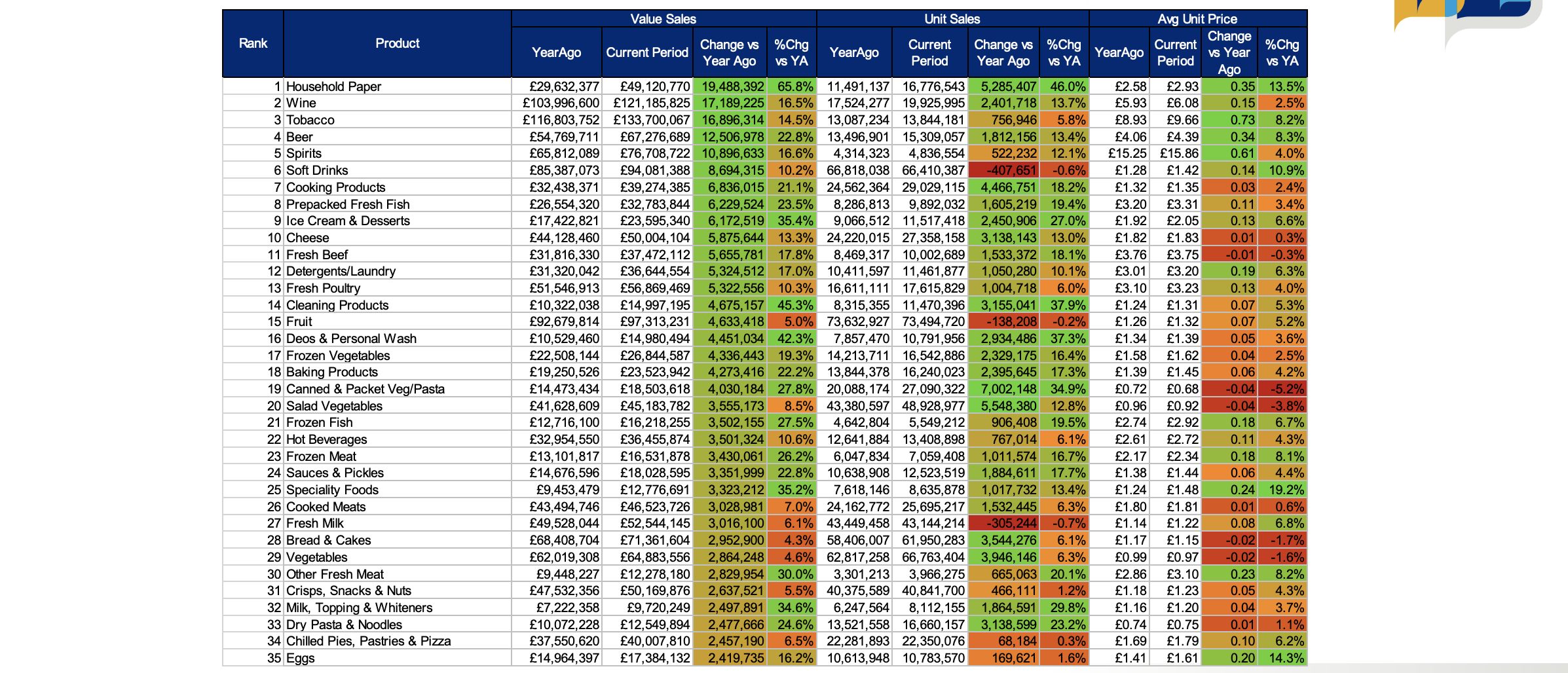

Top 35 Categories based on Value Change for the Latest Week.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}