Our 2020 Focus report provides a full insight into the extraordinary year we had. There are some big surprises, but on the whole the national economic condition is better than most analysts feared and a mini-boom might be expected once restrictions are eased again.

This Focus Report contains:

- Summary of UK Performance

- SalesOut MarketView

- SalesOut MarketView Ethical Report - Retail

Summary of UK Performance

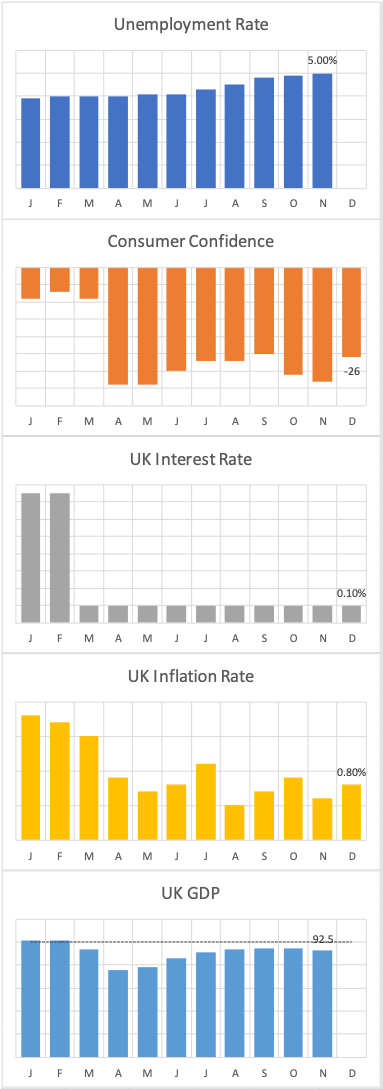

- Rising unemployment, whilst anticipated, is a major concern with post-Brexit uncertainty and stronger C19 restrictions continuing to stall any sign of recovery for early 2021

- There are currently 1.7m people unemployed in the UK (Aug-Oct 2020) but most believe this figure will be far higher once the government furlough scheme comes to an end

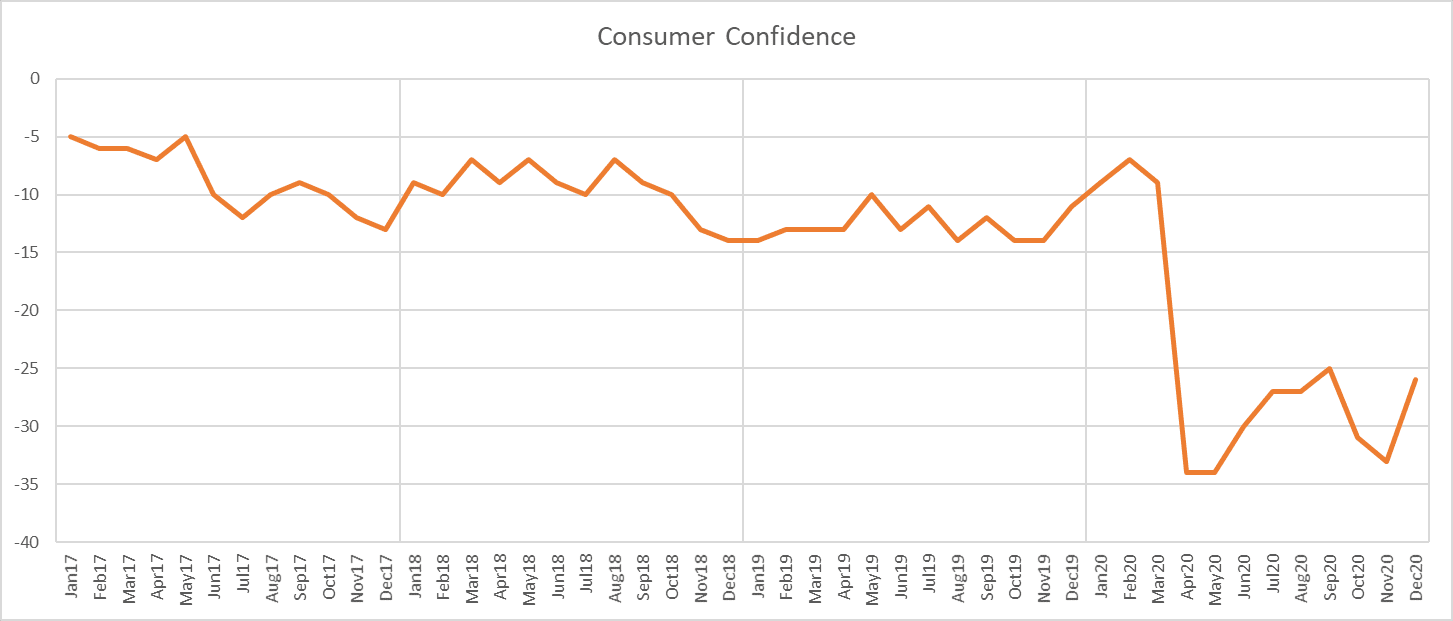

- Consumer confidence certainly improved following the Dec19 general election, but the trend is now reflective of increasing or decreasing lockdown restrictions

- Declining UK inflation has been driven primarily by reduced spending rates in general grocery and clothing products. In the last 3 months, the poorest performing areas are Food/Bev (-0.9%), Restaurants (+0.1%), Transport (+0.8%), compared to 2020 Q1

- Lockdown 1 saw consumers increase spending to stock up on food (essentials), alcohol and on restaurant (take-aways)

- A constant in 2020 was for increased spending in recreation and culture experiences (in the home?)

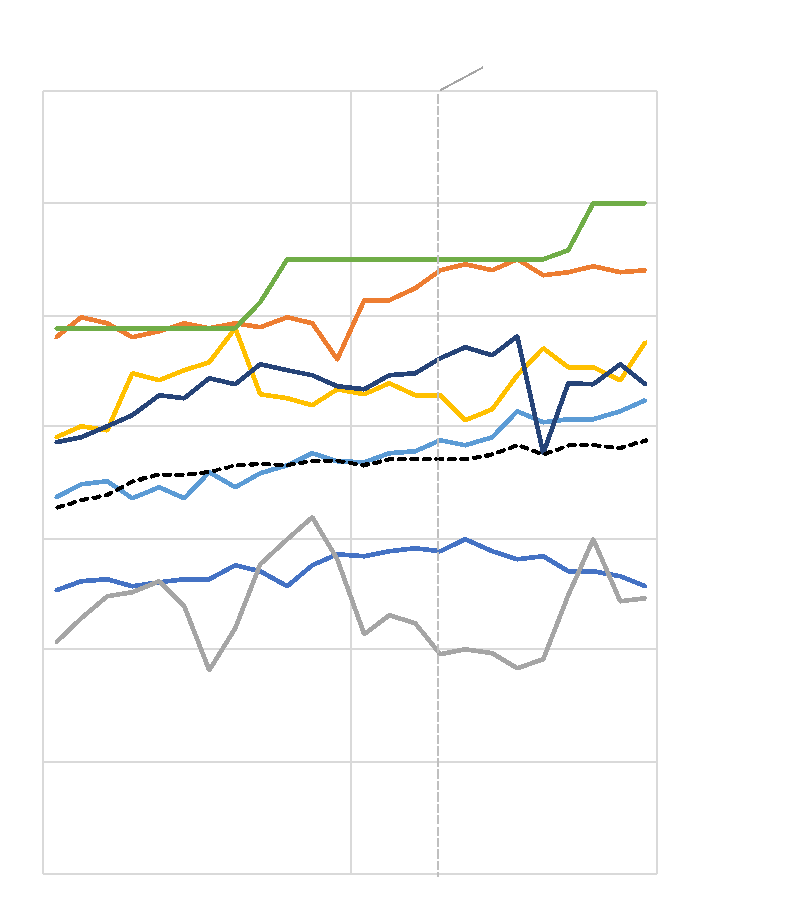

UK consumer confidence grows as Boris is confirmed Prime Minister then falls:

Declining UK inflation has been driven primarily by reduced spending rates in general grocery and clothing products.

In the last 3 months the poorest performing areas are Food/Beverages (-0.9%), Restaurants (+0.1%), Transport (+0.8%), compared to 2020 Q1.

- Lockdown 1 saw consumers increase spending to stock up on food (essentials), alcohol and on restaurant (take-aways)

- A constant in 2020 was for increased spending in recreation and culture experiences in the home

- Spending on transport increases fairly quickly as lockdown restrictions are eased

- Restaurant expenditure (on take-aways) held up under lockdown 1 but EOTHO in August introduced a dramatic reduction followed by lower spending levels

- With fewer opportunities to go out socially, spending on clothing slowed throughout 2020 up to the period of fewer restrictions between August and October

SalesOut MarketView

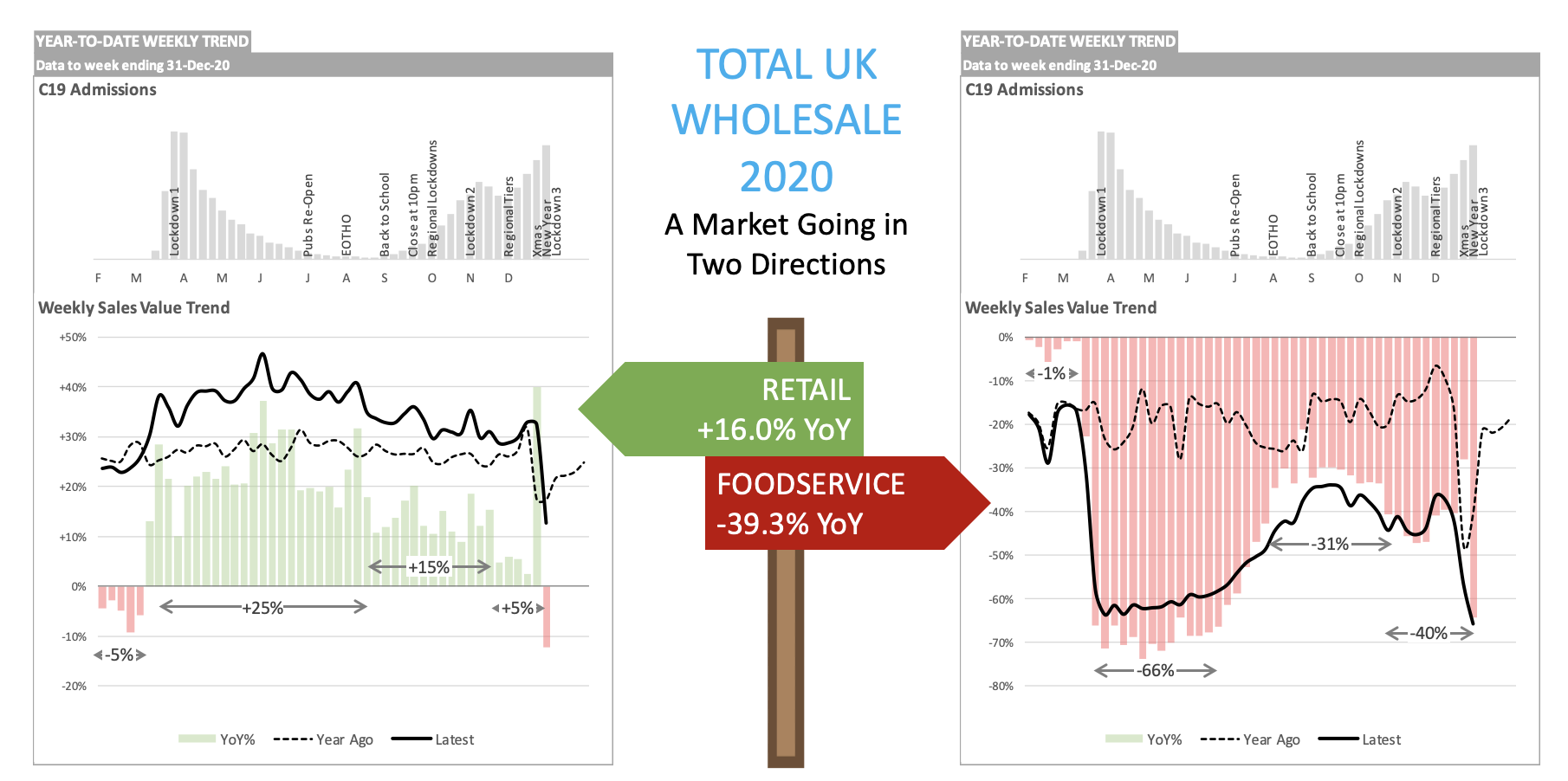

The big dichotomy for UK wholesale is that Covid-19 restrictions created a strong boost for convenience retailers, but all-but-closed the OOH sector, especially hospitality.

Over time, the early increased sales has slowed for convenience, driven by fewer restrictions, more home delivery slots and pressure from the multis. But, the sector has pulled a newer audience who may have been surprised at range, price, availability and experience. The challenge now is how to keep as much of the new audience as possible.

Foodservice is under some strong restrictions, and over time it is becoming clear that a “return to normal” is highly unlikely, especially for many office based workers.

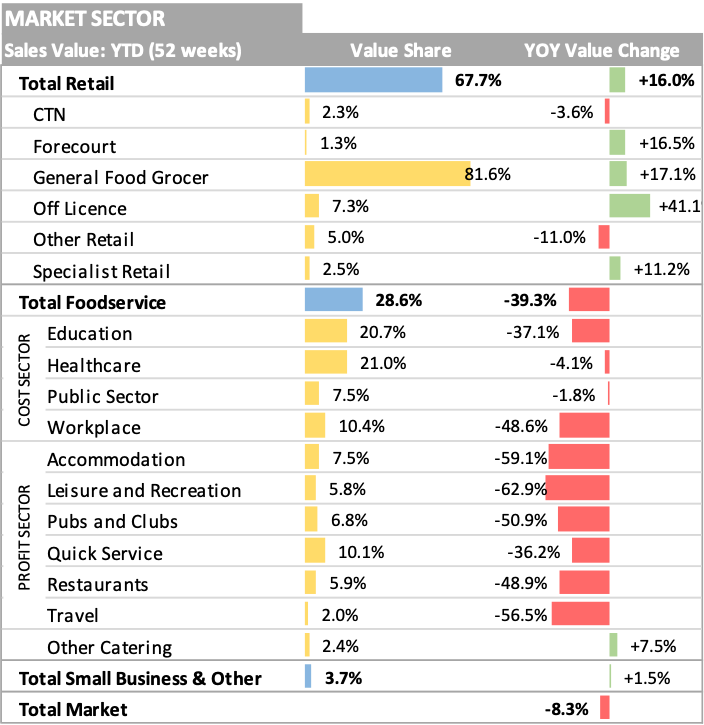

The Retail channel currently accounts for a little more than two-thirds of sales through UK wholesale but, in more normal times, this would be 55%:

- Fewer commuting trips but benefiting from local convenience grocery trips

- Significant benefit from the closure of hospitality, especially pubs

- Big C19 Lockdown 1 benefit. Consumers ‘forced’ into local stores allaying many fears of range, availability, price and overall experience

- Meals continue, but offer changed to on-site packed lunch

- Driven by office-based workforce and not manufacturing

- Take-away and home-delivery boom, but far fewer passing trade occasions for cafes

- Patient and inmate feeding continues

- Enforced closures for core hospitality on-site meals

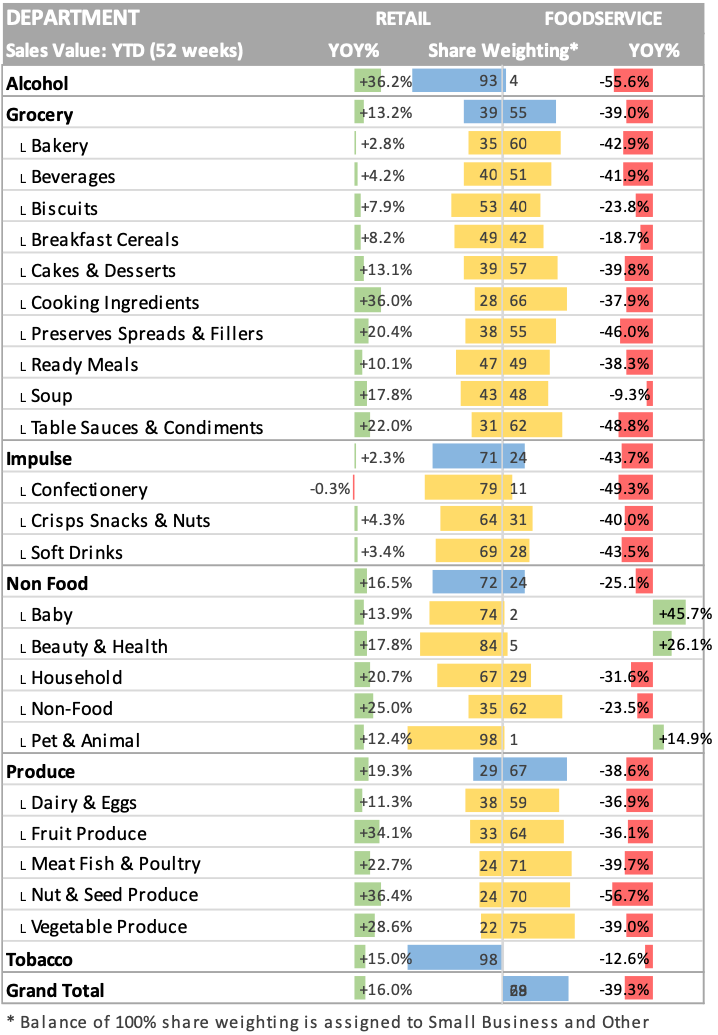

- Heavily weighted to the retail channel, Alcohol sales have boomed for UK (retail) wholesalers

- Perhaps surprisingly, Impulse products have seen no signs of strong retail growth this year

- Fewer commuting to work trips and lunch-deals appear to be the main drivers of this

- A strong notable behaviour has been a dramatic reduction in the sales of “singles” vs. some uplift for “sharing”

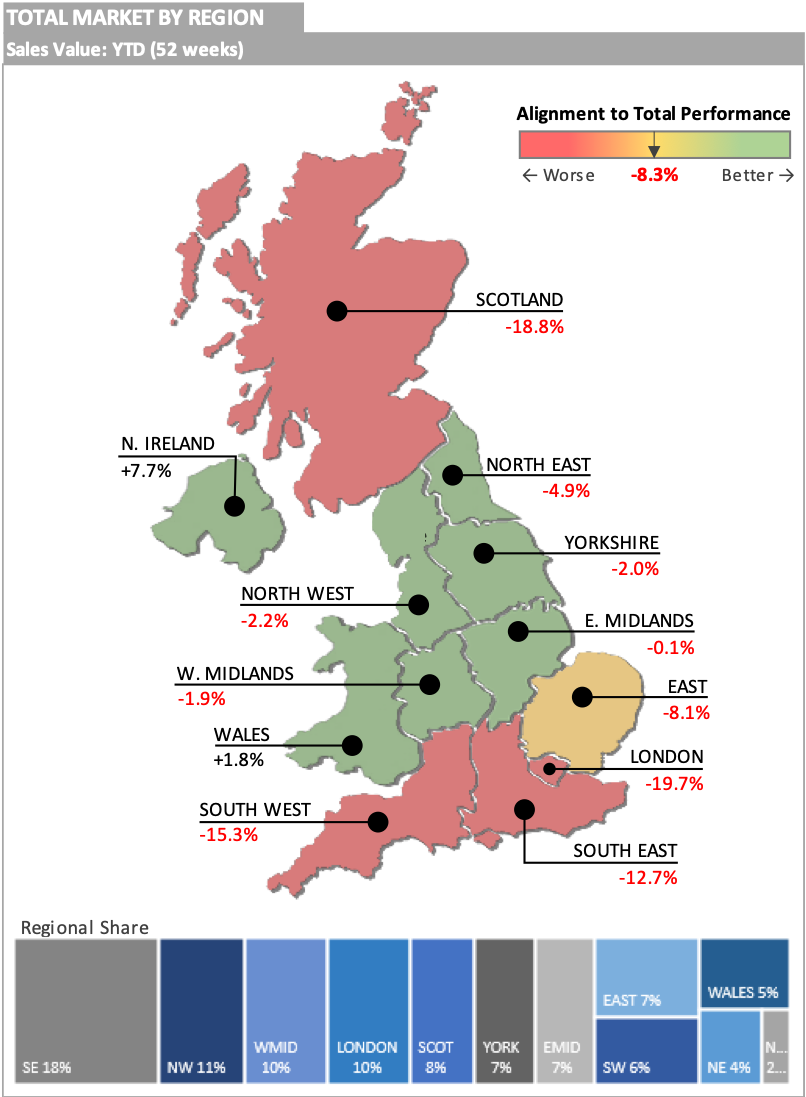

The UK regions that have generally under-performed tend to be those where tourism and holiday makers visit the most:

The latest central scenario forecast for inbound tourism to the UK in 2020 is:

- A decline of 76% in visits to 9.7 million

- A decline of 80% in spending to £5.7 billion

- This would represent a loss vs the pre-COVID forecast of 32.3 million visits and £24.7 billion spending

2021 forecast (Jan21):

- The latest revised central scenario for inbound tourism in 2021 is:

- 11.7 million visits, up 21% on 2020 but only 29% of the 2019 level

- £6.6 billion to be spent by inbound tourists, up 16% on 2020 but only 23% of the 2019 level

- This is a significant downgrade from the original forecast for 2021, which was run in early December 2020

The negative impact of (office based) businesses, especially in city centres, cannot, and must not, be underestimated:

- London continues to see the biggest negative impact due to Covid-19 for the UK wholesale sector

- City centre convenience retail has not seen the sales uplift “boost” seen everywhere else

- By far the strongest trading month for Foodservice in 2020 was September, which followed the government EOTHO scheme

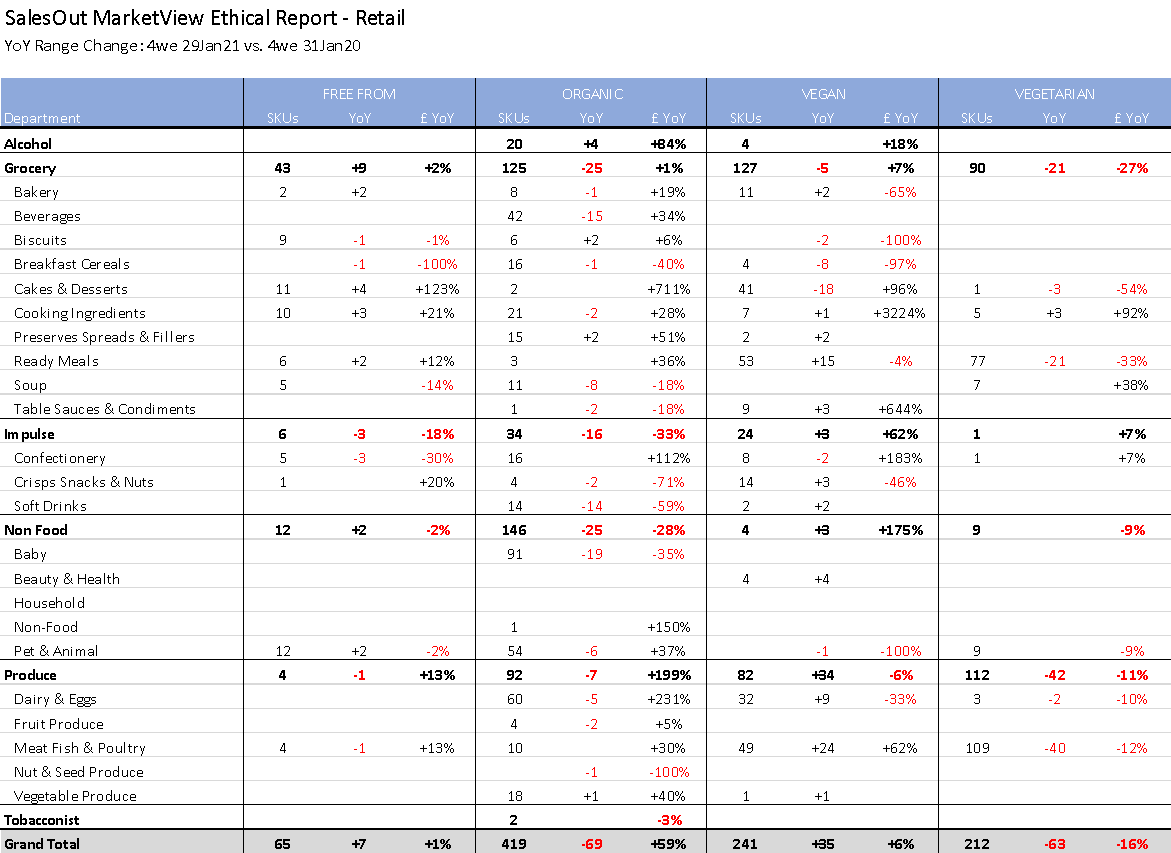

SalesOut MarketView Ethical Report - Retail

The continuing rise of Vegan and Vegetarian products within the wholesale channel was not dampened even by the Covid pandemic. Manufacturers across the market continue to release NPD focussed on these two areas – and we see no reason why this type of rollout should slow down for 2021: