This report contains:

- Summary of UK Performance - Week 21

- UK update on COVID-19

- Total Market Overview

- Additional Support from IRI

- IRI White paper

- IRI Global Demand Index

Summary of UK Performance

- End of the 21st week of the UK lockdown and the impact of COVID-19 sees the UK economy shrink a sixth in size since pre-crisis. The FTSE 100 drops as markets continue to feel the impact of increased UK foreign travel restrictions with France joining the list of countries people must quarantine for 14 days on return.

- In the latest week, sales reached £2.29b; £190m higher than the same time last year but a drop of -0.6% on last weeks’ sales.

- Whereas we may have expected sales to dip due to the normal summer holiday period, combined with the effect of the Governments “Eat Out to Help Out”, we can assume this has been balanced out and sales momentum maintained in the UK due to reduced travel abroad and an increase in UK holiday ‘staycations’.

- The Household Finance Index from data company IHS Markit fell to 40.8 in August from 41.5 in July, dragged down by the biggest drop in job security since 2011.

- Whilst there is evidence of a slowdown across both Value and Unit sales, the recent weekly sales growth indicates it may be a while before we return to normal levels.

- The Convenience and Online Channels have both benefitted from changing consumer shopping habits however in the latest data, Convenience figures show it accounts for 24.5% of Total sales similar to pre-COVID-19 figures.

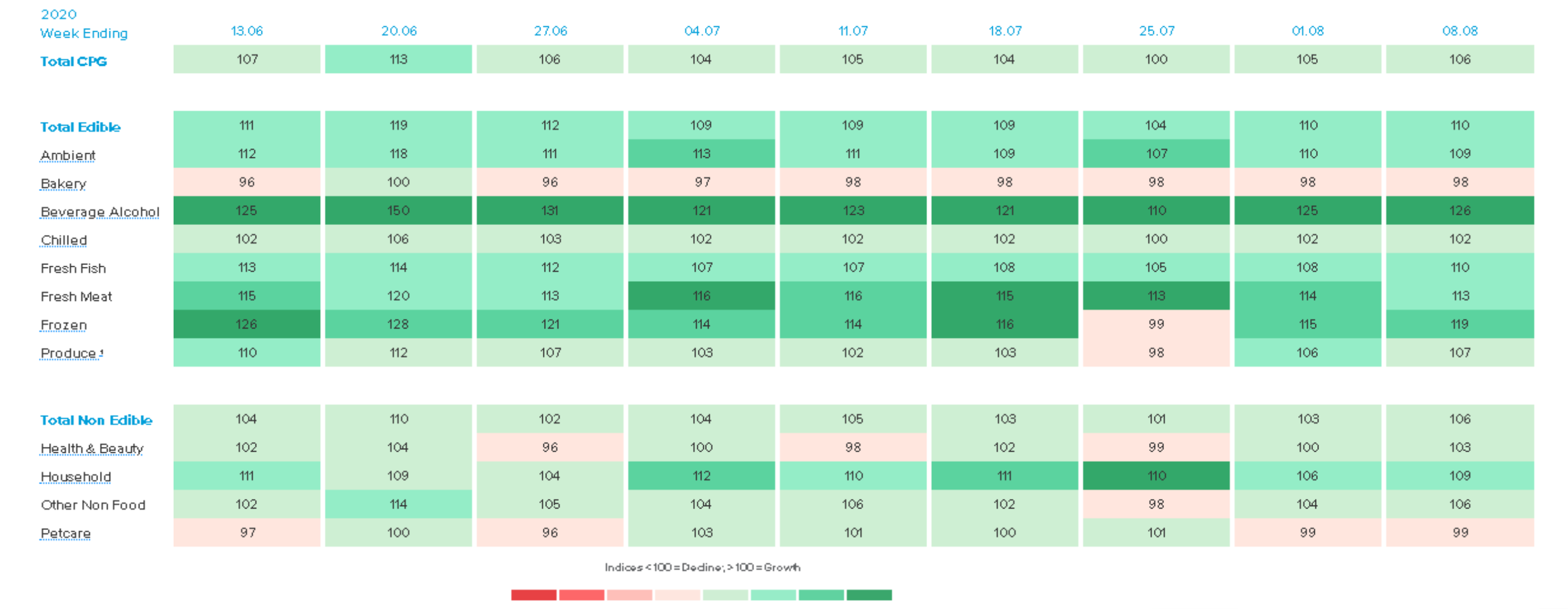

- IRI’s Inflation Tracker shows Fresh Fish is the only department to have lower prices than last year with Total CPG increasing to 104.

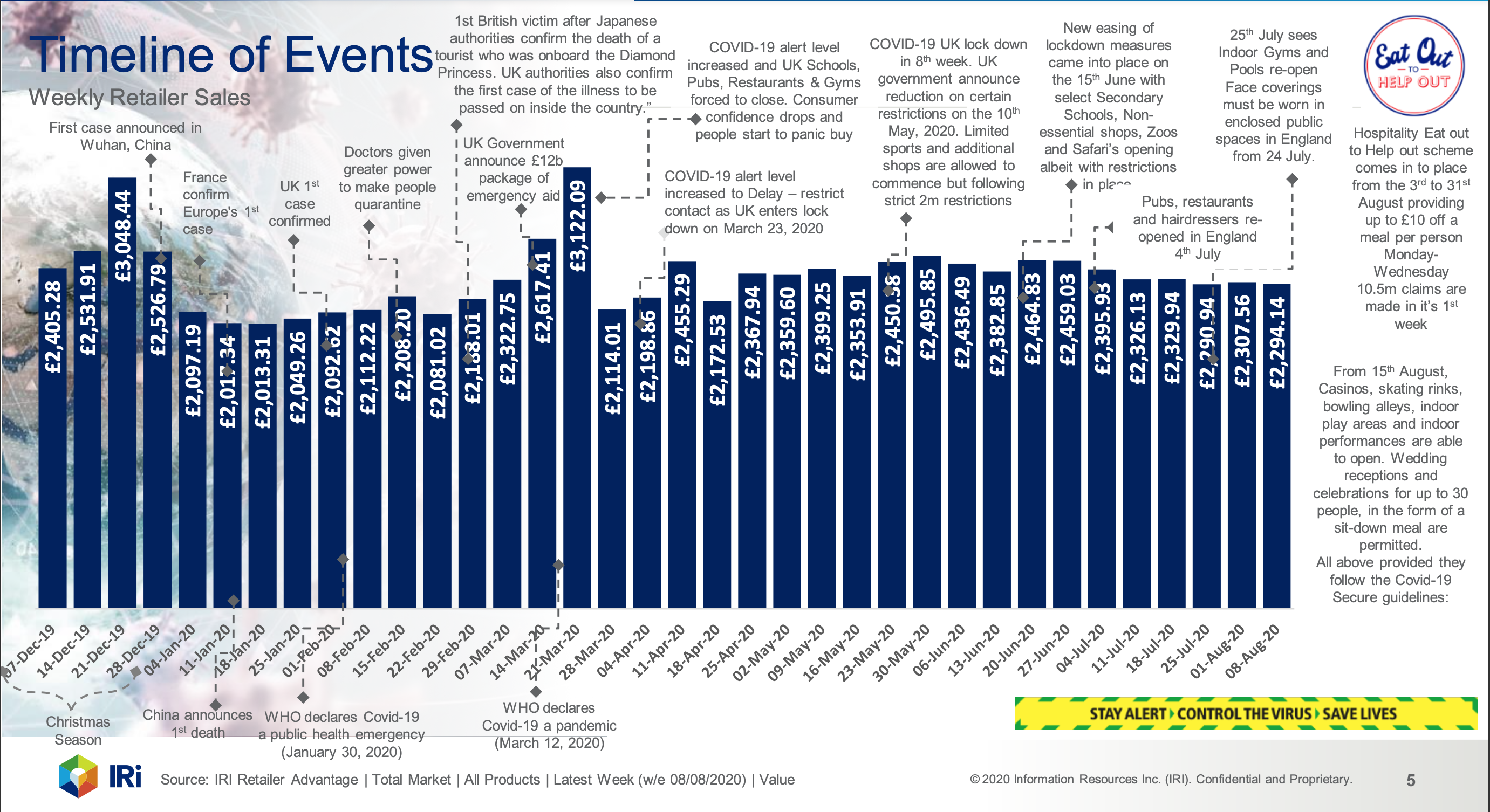

Timeline of Events

End of the 21st week of the UK lockdown and the impact of COVID-19 sees the UK economy shrink a sixth in size since pre-crisis. The FTSE 100 drops as markets continue to feel the impact of increased UK foreign travel restrictions with France joining the list of countries people must quarantine for 14 days on return.

- FTSE 100 fell in the latest week as Airline, Travel and Oil companies fall on the back of increased restrictions impacting international travel. France notable inclusions to global travel restrictions along with Spain that the UK government ask people to quarantine for 14 days when returning to the UK.

- The Household Finance Index from data company IHS Markit fell to 40.8 in August from 41.5 in July, dragged down by the biggest drop in job security since 2011. The index measures households' overall perceptions of financial wellbeing and signalled a further, slightly sharper, deterioration in the financial situation of UK households which may last for the foreseeable future.

- Output suffered a record slump of 20% in April - the first full month of the lockdown - but recovered some growth in May which accelerated in June as more sections of the economy gradually re-opened. The ONS says that, as of the end of June, the economy remained a sixth smaller than it was pre-crisis.

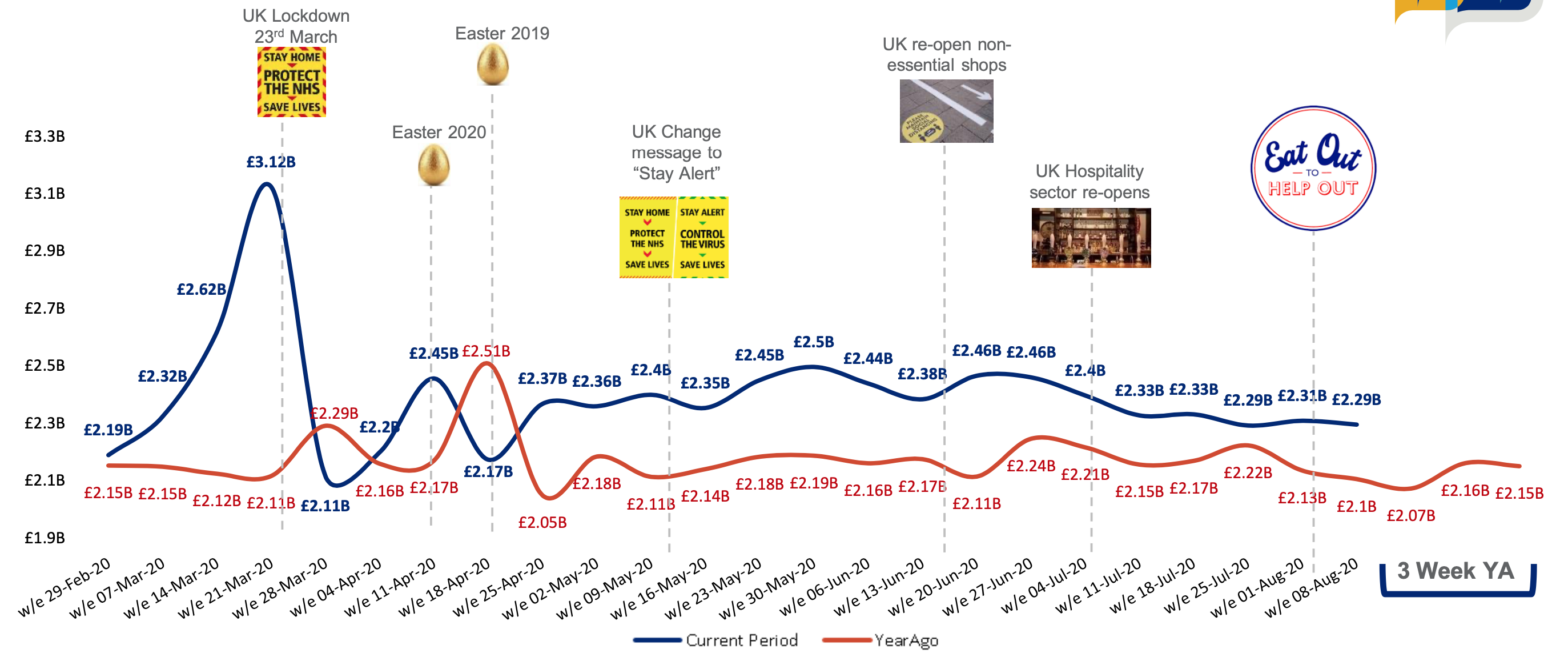

Total Market Sales Value

In the latest week, sales reached £2.29b which is £190m higher than last year and now we are in the summer holiday period, sales are expectedly down from previous weeks. There is no evidence yet that the Governments “Eat Out to Help Out” has impacted sales, even though 10.5m claims have been made. The overseas travel restrictions will likely result in an increase in UK holidays or “Staycations” which may help maintain the sales momentum.

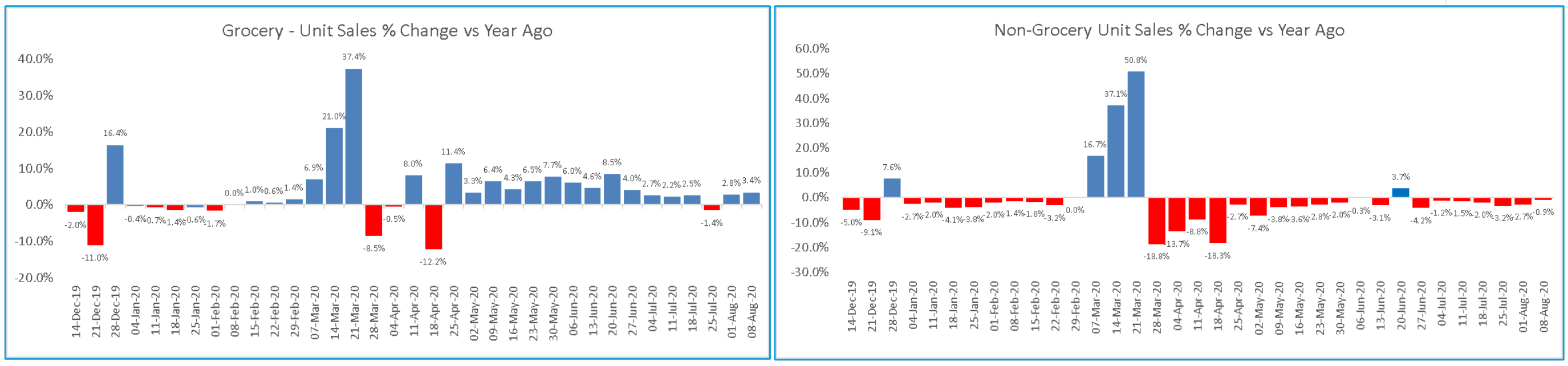

Grocery Unit sales (+3.4%) returned to growth vs PY whilst Non-Grocery Unit sales (-0.9%) remains down in the latest week, the trend has improved compared to recent weeks.

- BWS Unit sales growth (+21%) and Frozen (+7.0%) responded to the warmer weather and compares favourably vs last year when more foreign holidays would traditionally impact demand.

- Health & Beauty Unit sales (0.0%) improved on previous weeks as the warm weather meant sales in Suncare increased. Deodorants and Personal hygiene continue to perform ahead of last year but Male Grooming and Razors/Blades are down as restrictions reduce the need to maintain appearances.

IRI’s Demand Index

Total CPG increase to 106 compared to last year as demand for BWS (126) Frozen (119)and Household (109) increased on continued restrictions

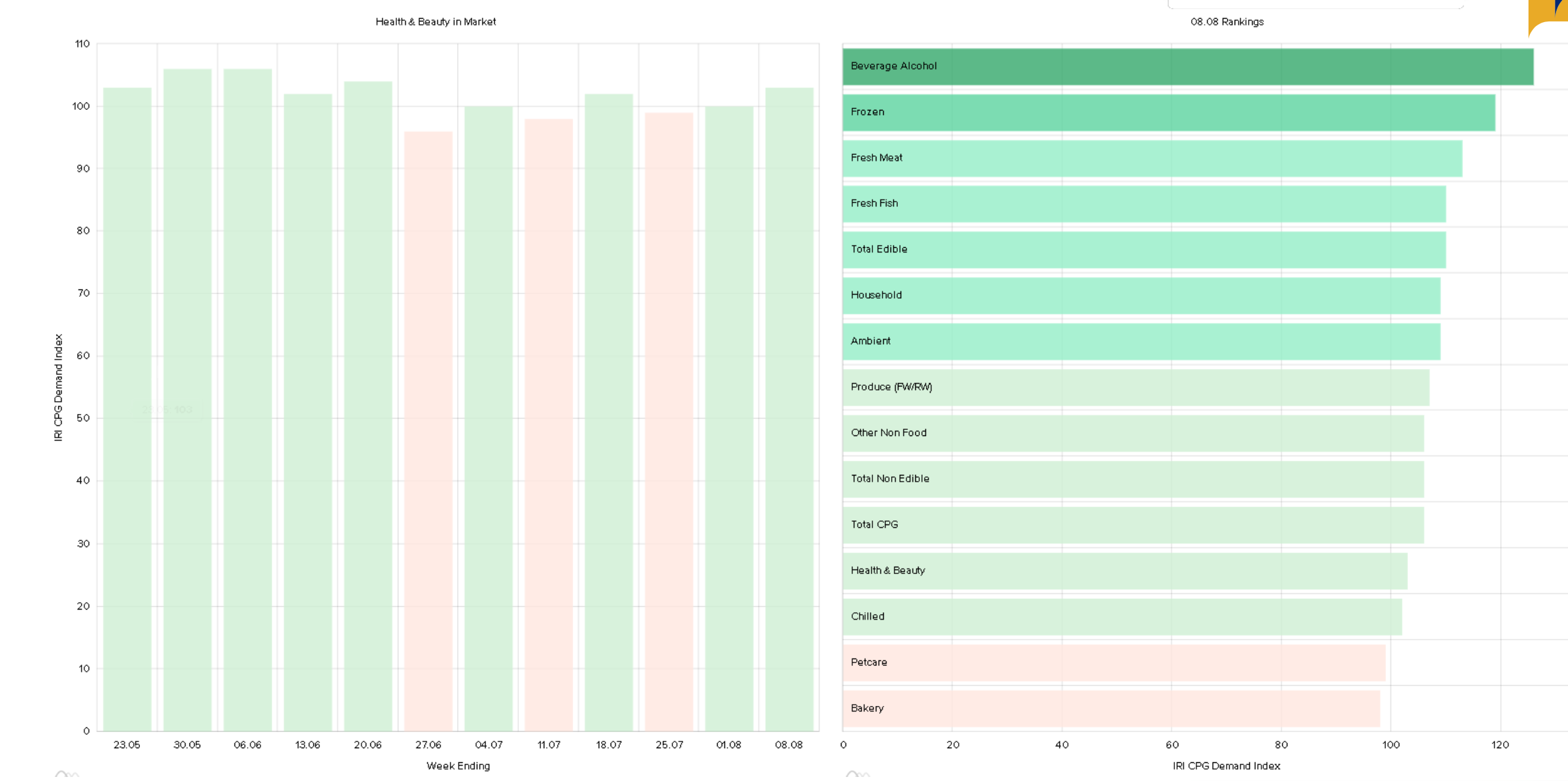

Focus on Health & Beauty

recent Demand Index slightly ahead of last year helped by Suncare and Skincare

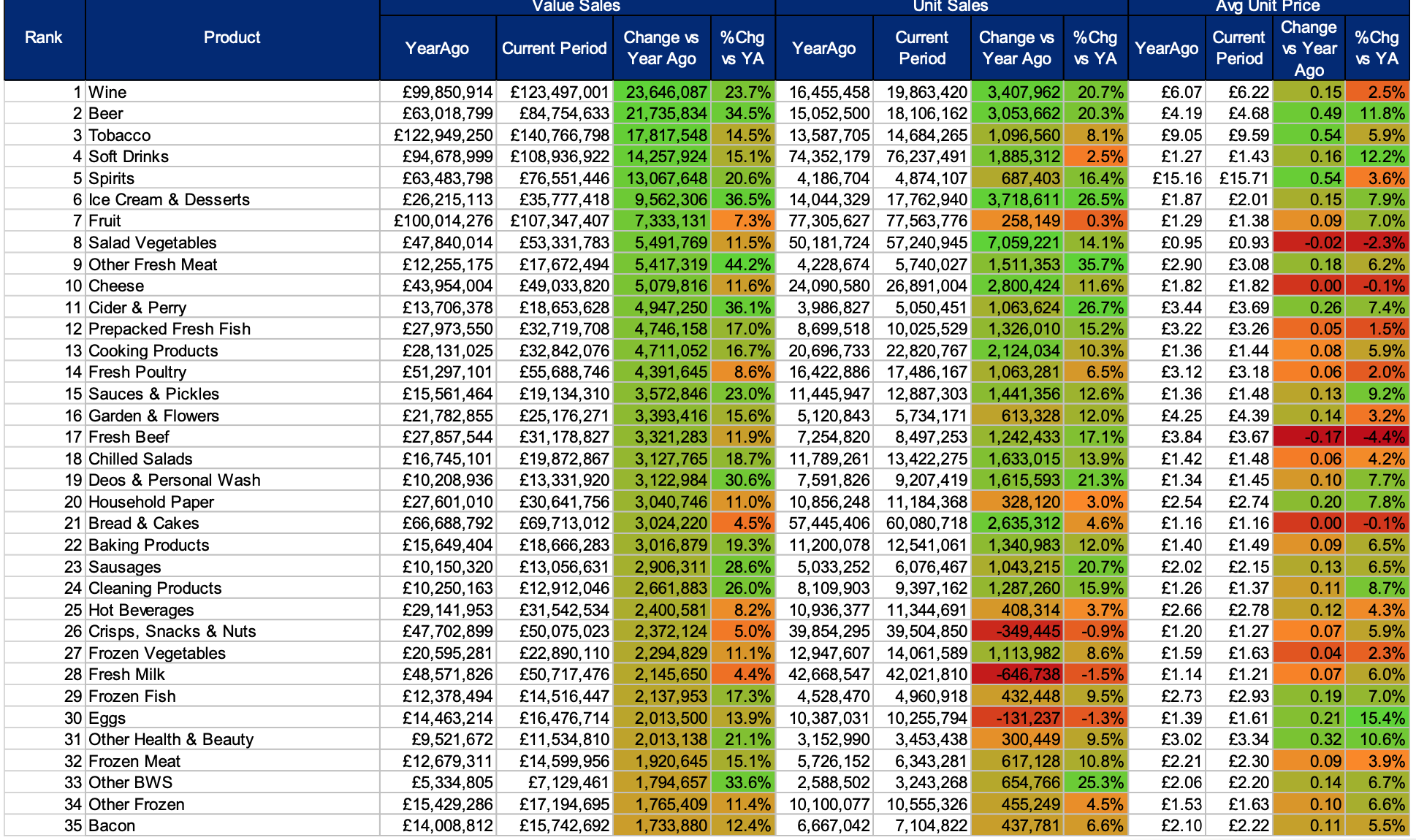

Top 35 Categories based on Value Change for the Latest Week