This report contains:

- Summary of UK Performance

- UK update on COVID-19

- Total Market Overview

- Additional Support from IRI

- IRI White paper

- IRI Global Demand Index

SUMMARY OF UK PERFORMANCE

- End of the 20th week of the UK lockdown and the FTSE 100 drops as markets continue to monitor the cancellation of lockdown restrictions and localised lockdowns, whilst unemployment levels rise as fears grow over the expected recession. However there are positive signs as over 10.5m meals are claimed in the 1st week of the “Eat out to Help out” scheme

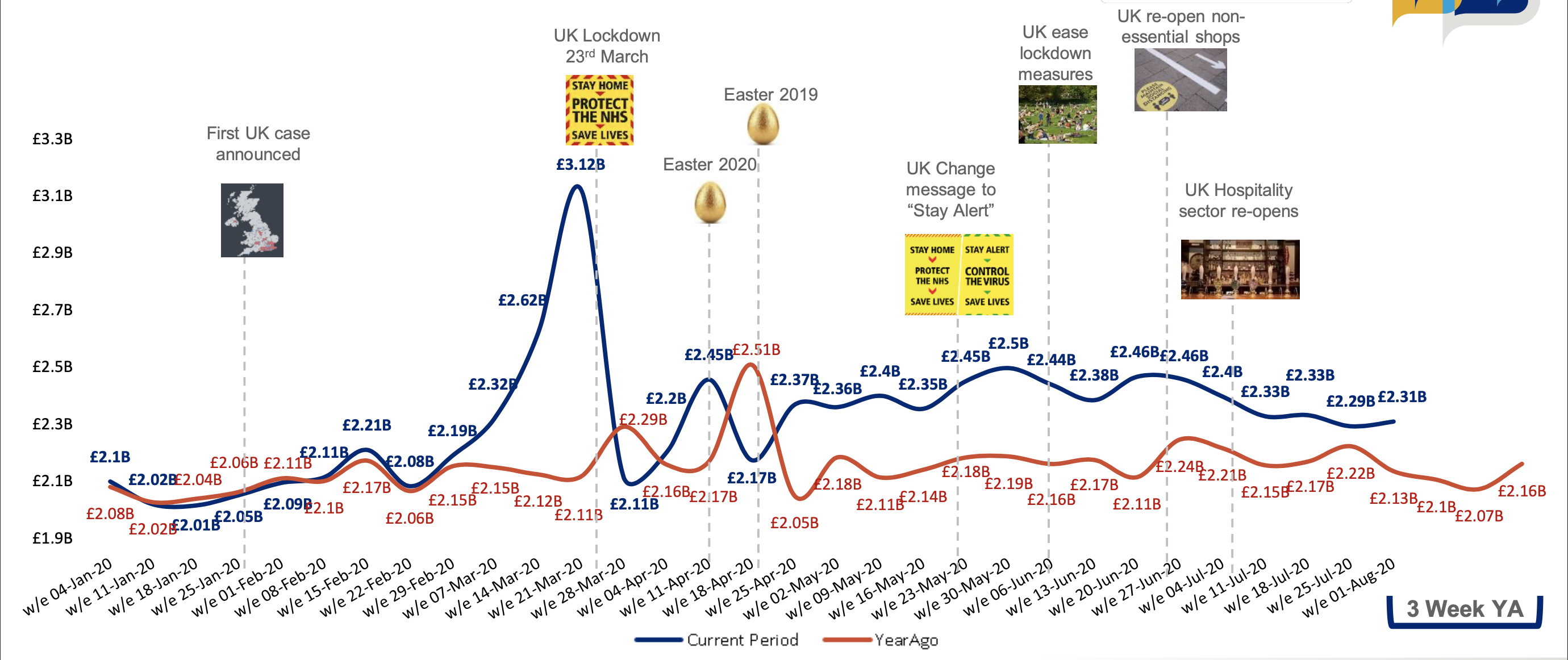

- In the latest week, sales reached £2.31b; £174m higher than the same time last year and an increase of +0.7% on last weeks’ sales

- Whilst we enter the summer holiday period, with travel restrictions in place, there is likely to be an increase in UK holidays or people staying at home which may help maintain the sales momentum. However now the “Eat out to Help out” scheme has started in the hospitality sector, it’s potential impact on Grocery sales will be clearer in the coming weeks

- Since the beginning of 2020 and predominantly since the start of COVID-19, UK Retailer sales are £4.947b higher than last year, driven by Ambient (+£1.5b) and BWS (+£1.4b) departments although both departments growth has reduced in the latest week

- Whilst there is evidence of a slowdown across both Value and Unit sales, the recent weekly sales growth indicates we may have more time before we return to normal levels

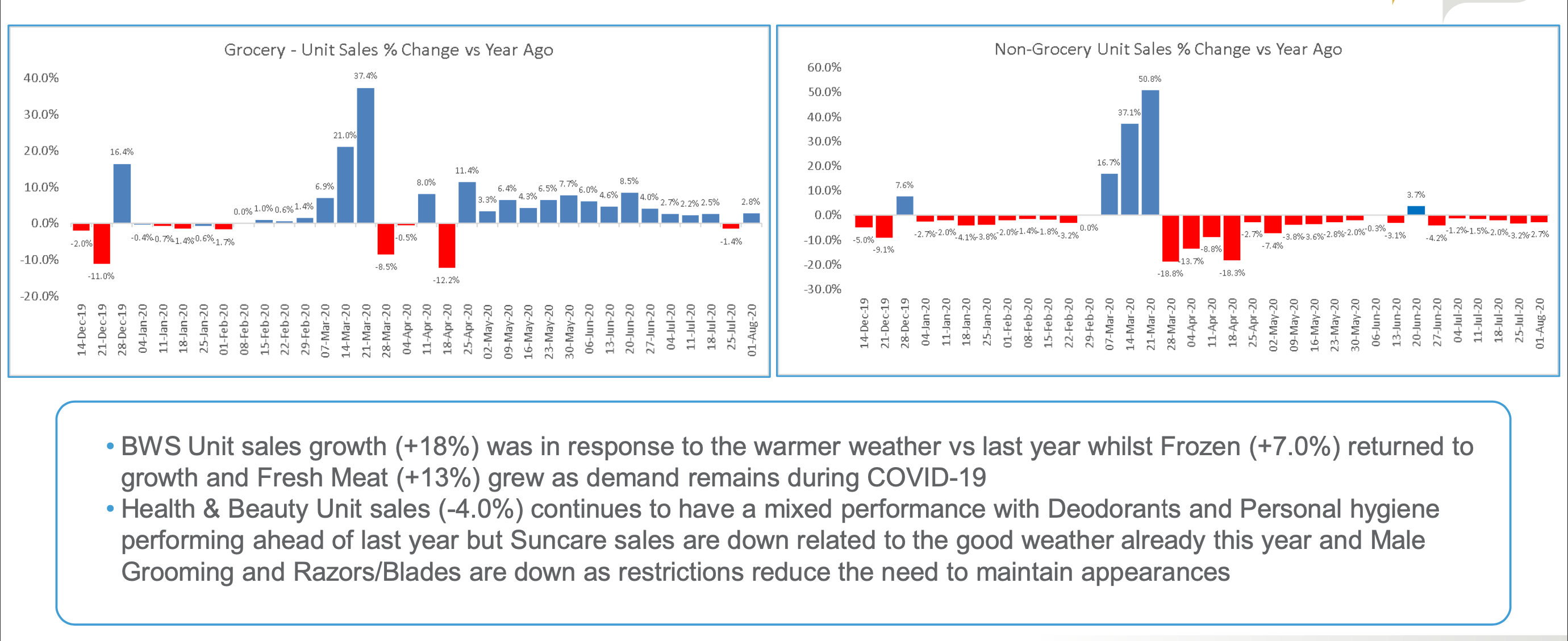

- Of the +8.2% growth in Total Store sales vs a year ago, Grocery sales increased +9.6% and Non Food +3.4%

- Of the additional £174m spend in the latest week, this was driven by Grocery +£157m and Non Food +£17m

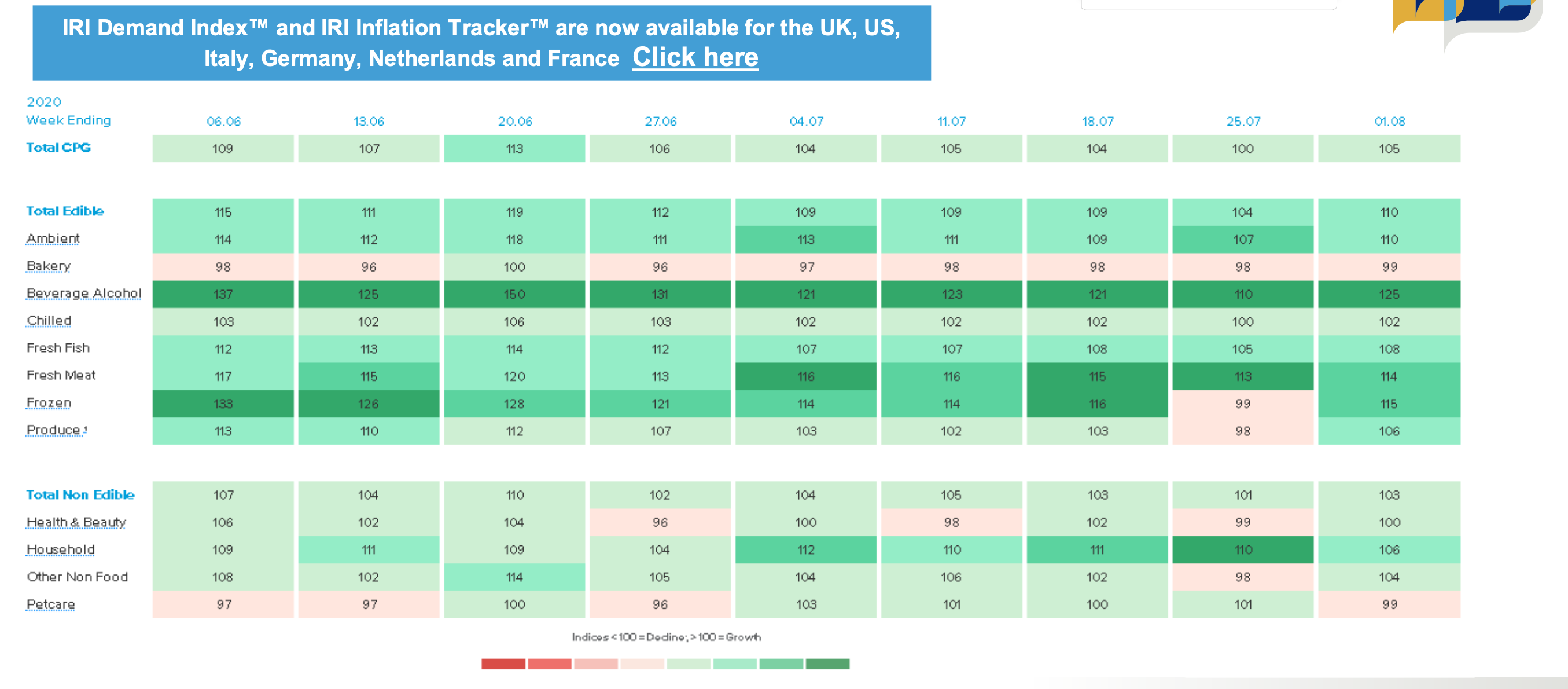

- US sales are indexing higher than other markets. Italy sales are below last years demand whilst most European markets have returned to levels in line with last year

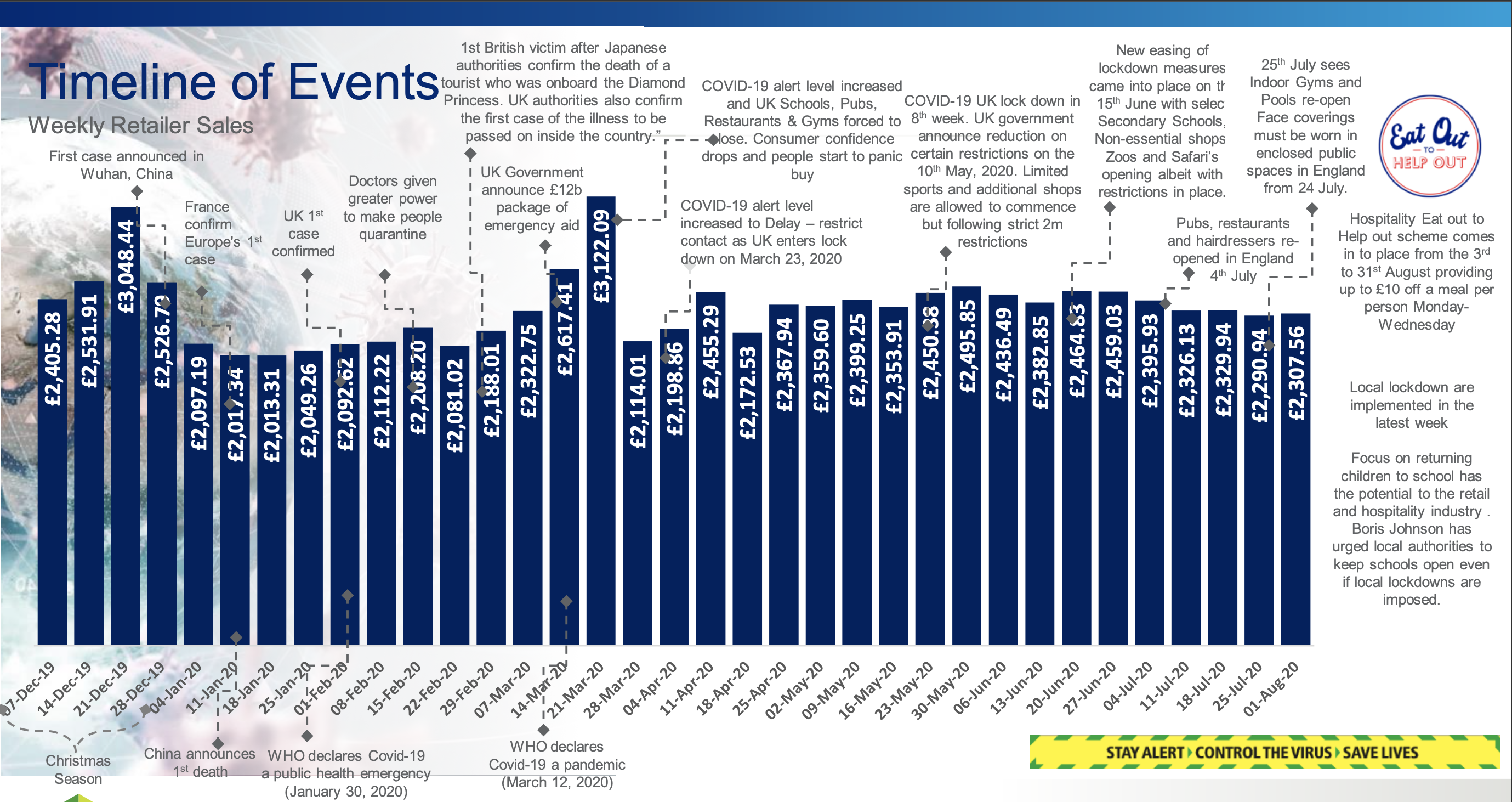

TIMELINE OF EVENTS

End of the 20th week of the UK lockdown and the FTSE 100 drops as markets continue to monitor the cancellation of lockdown restrictions and localised lockdowns, whilst unemployment levels rise as fears grow over the expected recession. However there are positive signs as over 10.5m meals are claimed in the 1st week of the “Eat out to Help out” scheme

- FTSE 100 fell in the latest week as it reacted to the Global rises in COVID- 19 cases and the cancellation of some restrictions being relaxed combined with localised lockdowns as cases start to rise

- HMRC said that, as of 9 August, it had received 10,540,394 claims under the scheme

The scheme, which is intended to boost the struggling hospitality sector, the government pays for 50% of a meal eaten at a cafe, restaurant or pub on a Monday, Tuesday or Wednesday

The government has set aside £500m to fund the policy

- As COVID-19 plunges Britain into what is expected to be the deepest recession on record

Few sectors have been spared as the collapse in demand takes its toll on industries from car making and double glazing to ferries and restaurants

Total Market Value Sales – In the latest week, sales reached £2.31b which is £174m higher than last year and whilst an increase on last week, sales are down from the levels seen over previous weeks. Whilst we enter the summer holiday period, with travel restrictions in place, there is likely to be an increase in UK holidays or people staying at home which may help maintain the sales momentum.

Grocery Unit sales (+2.8%) returned to growth vs PY whilst Non Grocery (-2.7%) Unit sales remain down in the latest week, a consistent trend since April

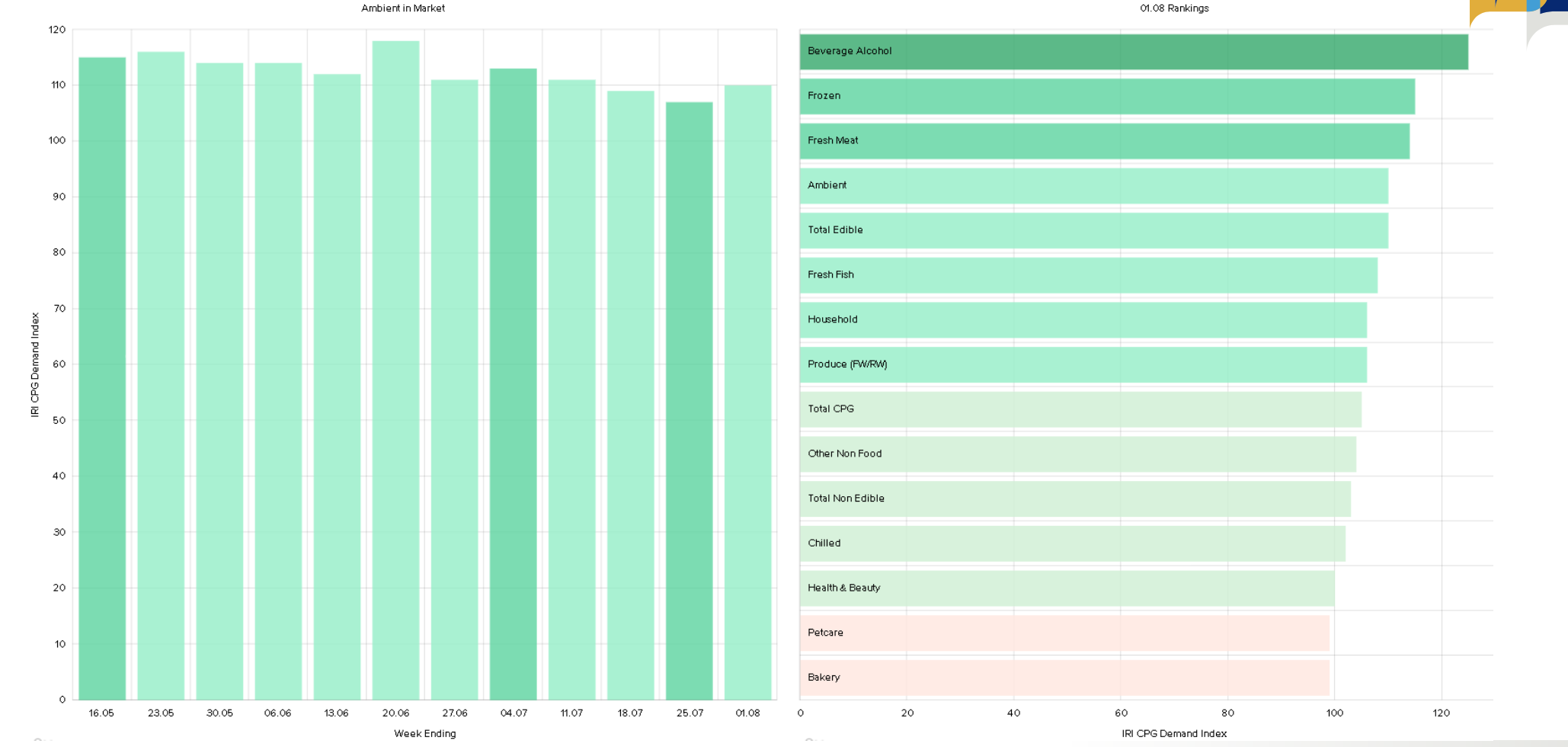

IRI’s Demand Index sees Total CPG increase to 105 compared to last year as demand for BWS (125) and Frozen (115) increased on continued restrictions

Focus on Ambient – recent Demand Index level whilst still ahead of last year has dropped to the 110 in the last 4 weeks

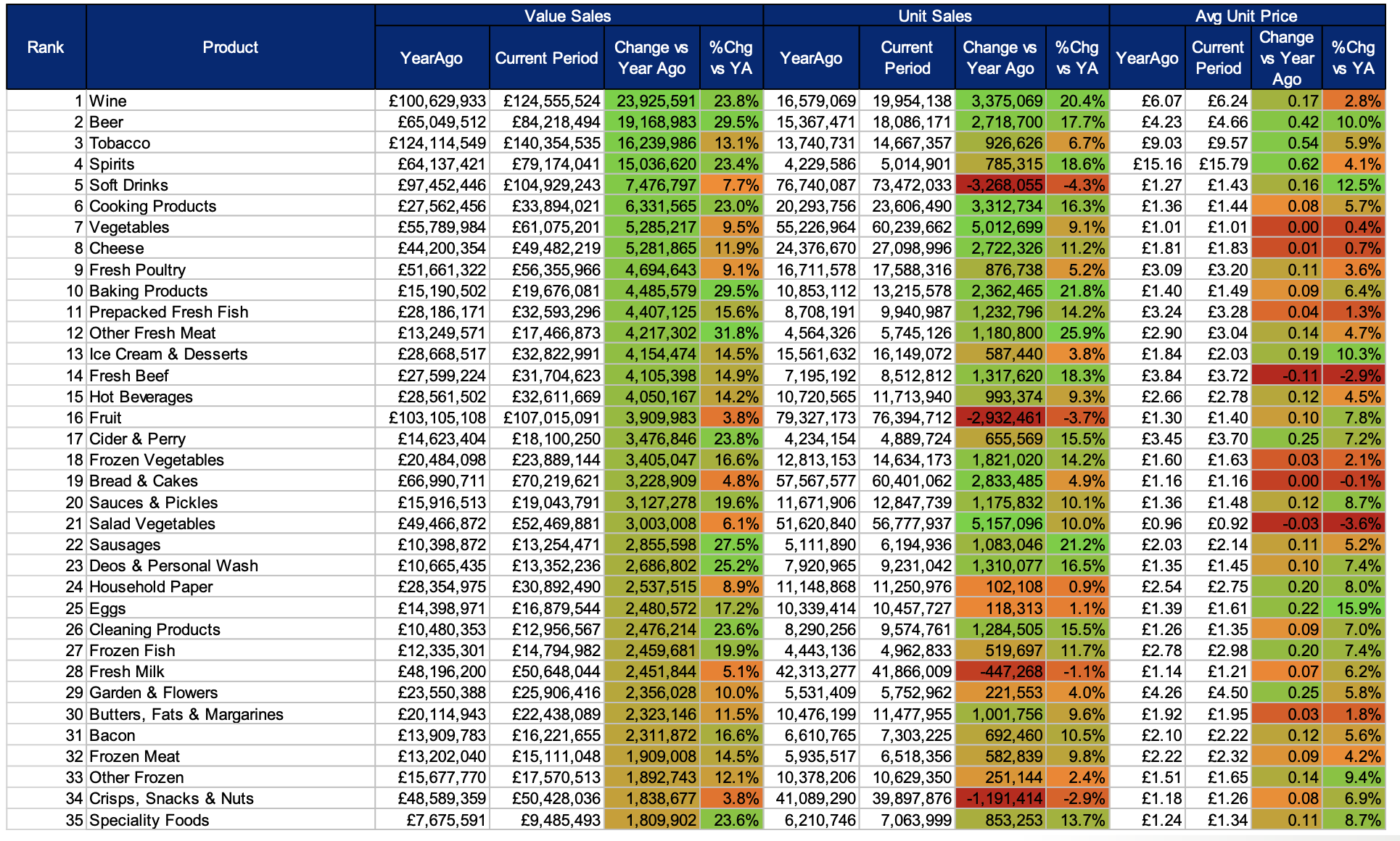

Top 35 Categories based on Value Change for the Latest Week

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}