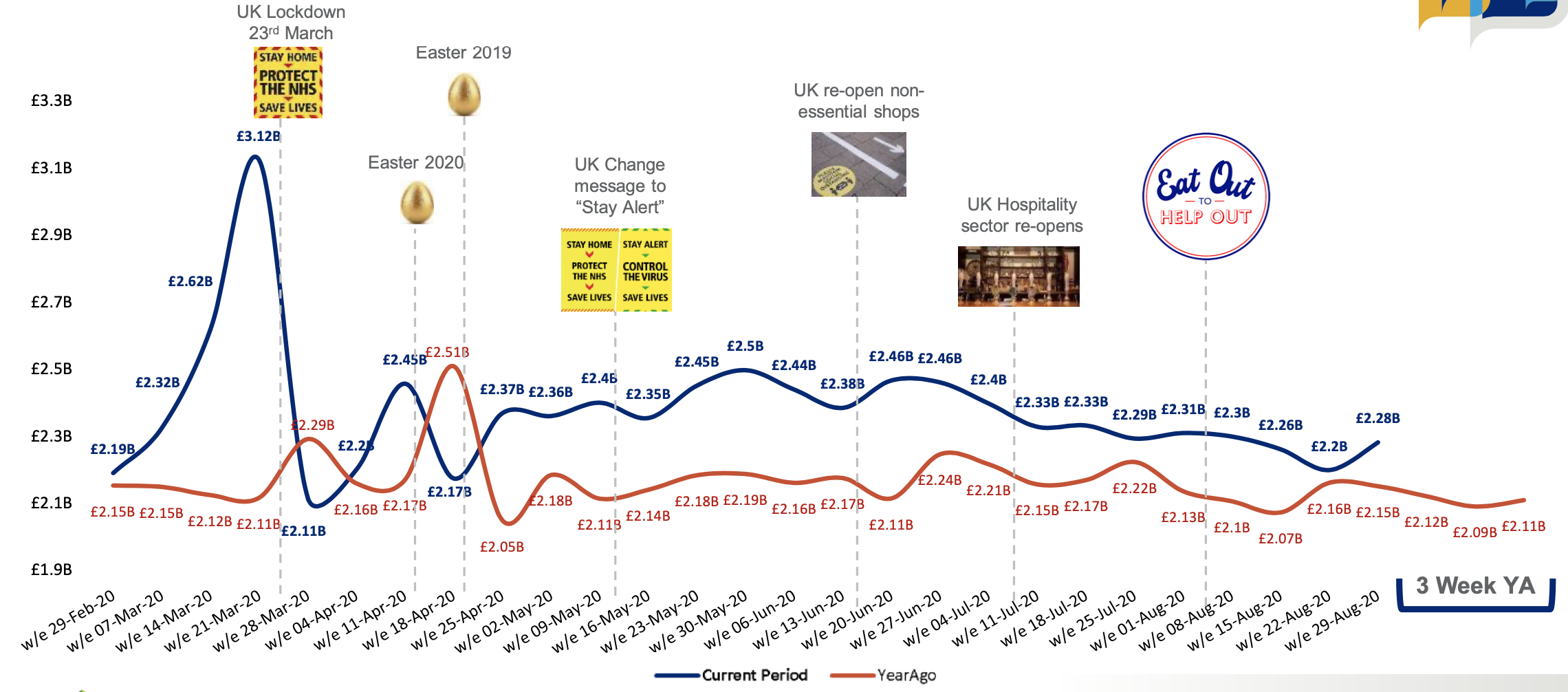

In the latest week, sales reached £2.28b which is £131m higher than last year. This week's sales have benefited from the phasing of the Bank Holiday which was a week later compared to last year, although last year we had warmer weather. The “Eat Out to Help Out” scheme ends in August and we know this has been successful with 64m meals claimed in the first 3 weeks. With the scheme ending on Monday and schools returning this week, it will be interesting to see what impact this has on next weeks sales.

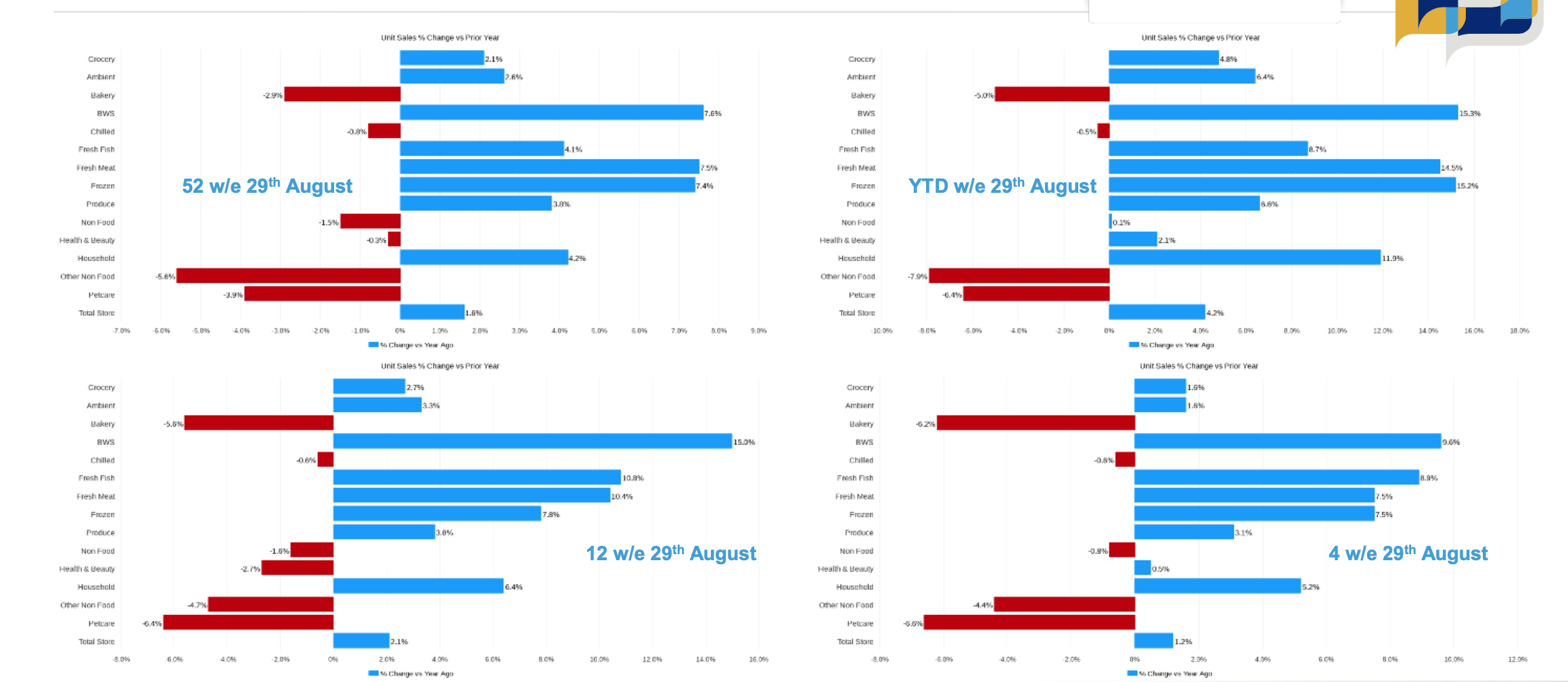

Total Store Unit sales growth in the latest 4 w/e is +1.2% however this has slowed compared to YTD which is +4.2% higher than last year

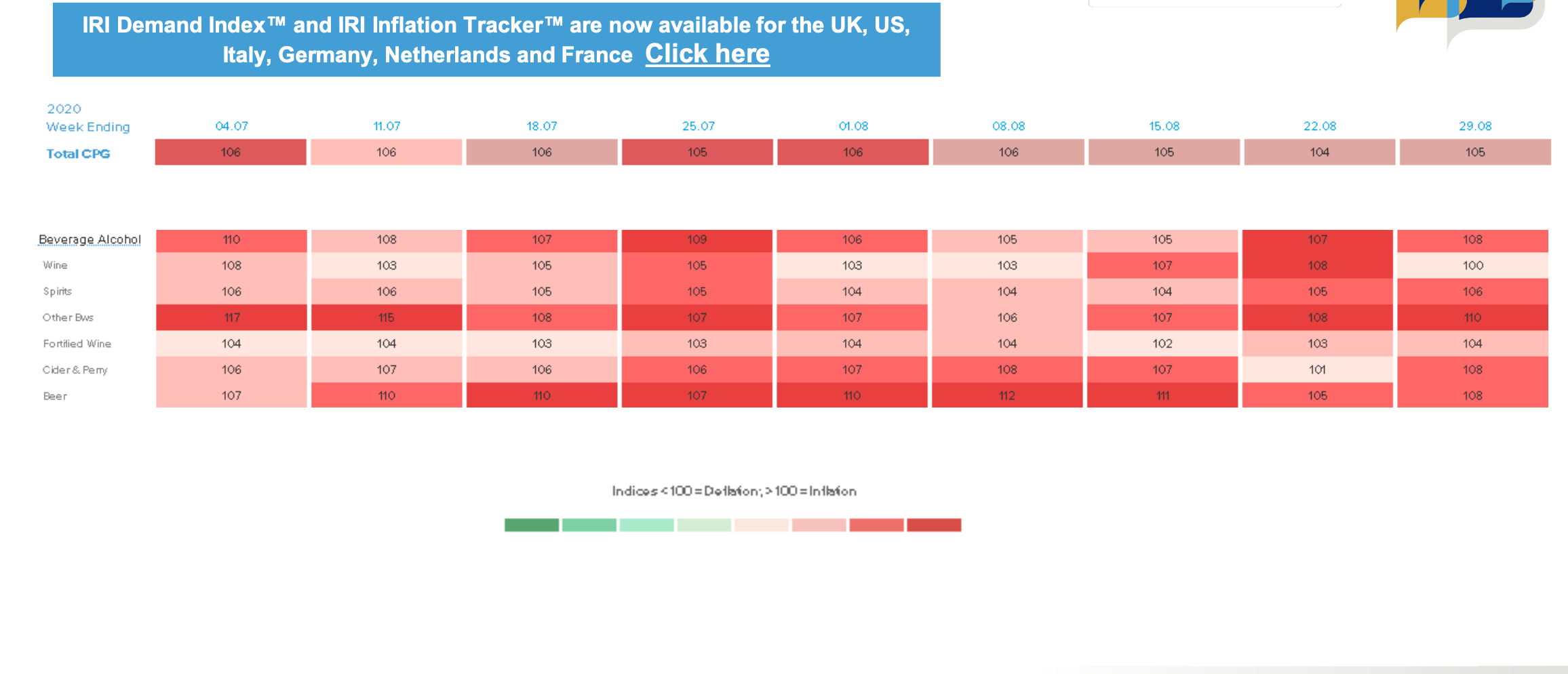

Focus on BWS – IRI’s Inflation Tracker shows Wine (100) prices are in line with last year whilst Beer (108) CIDER & Perry (108) and Spirit (106) have seen increased prices compared to last year with Total BWS increasing to 108

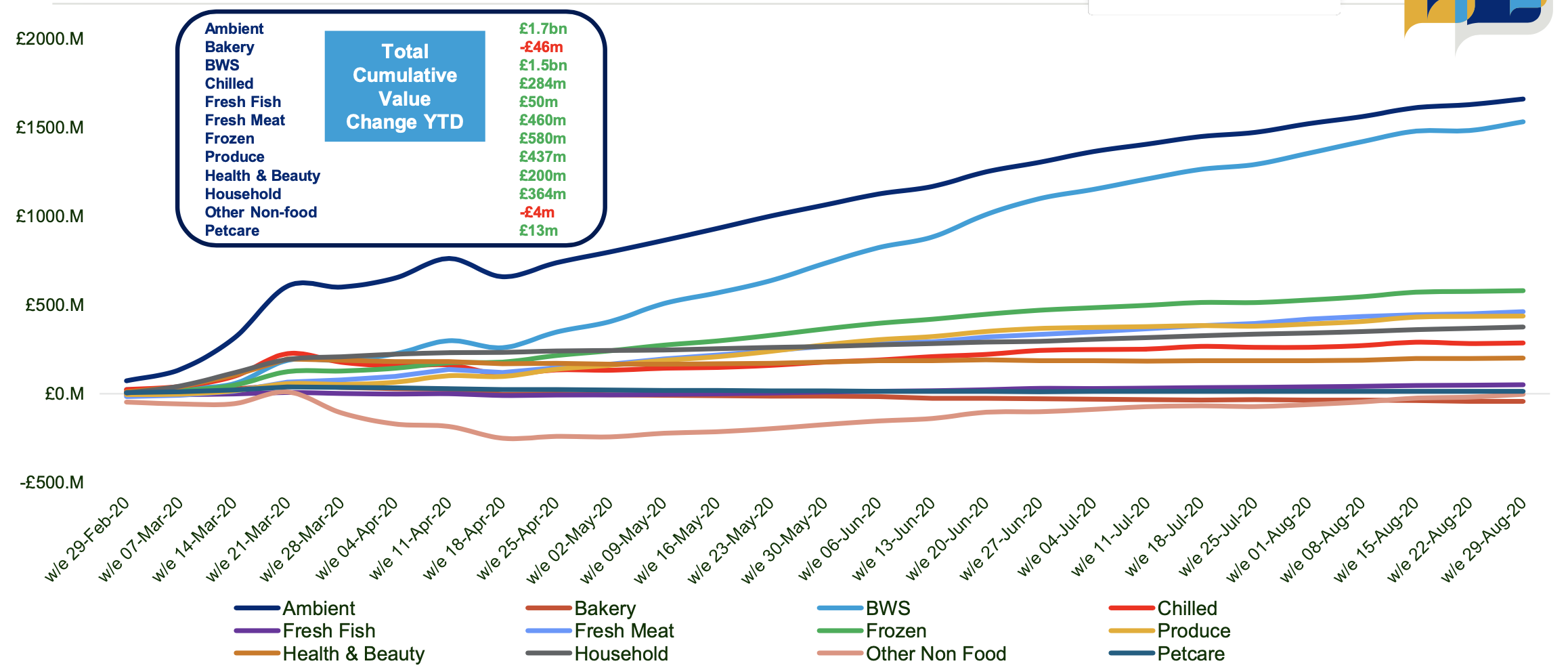

Since the beginning of 2020 and predominantly since the start of COVID- 19, UK Retailer sales are £5.539b higher than last year, driven by Ambient (+£1.7b) and BWS (+£1.5b)

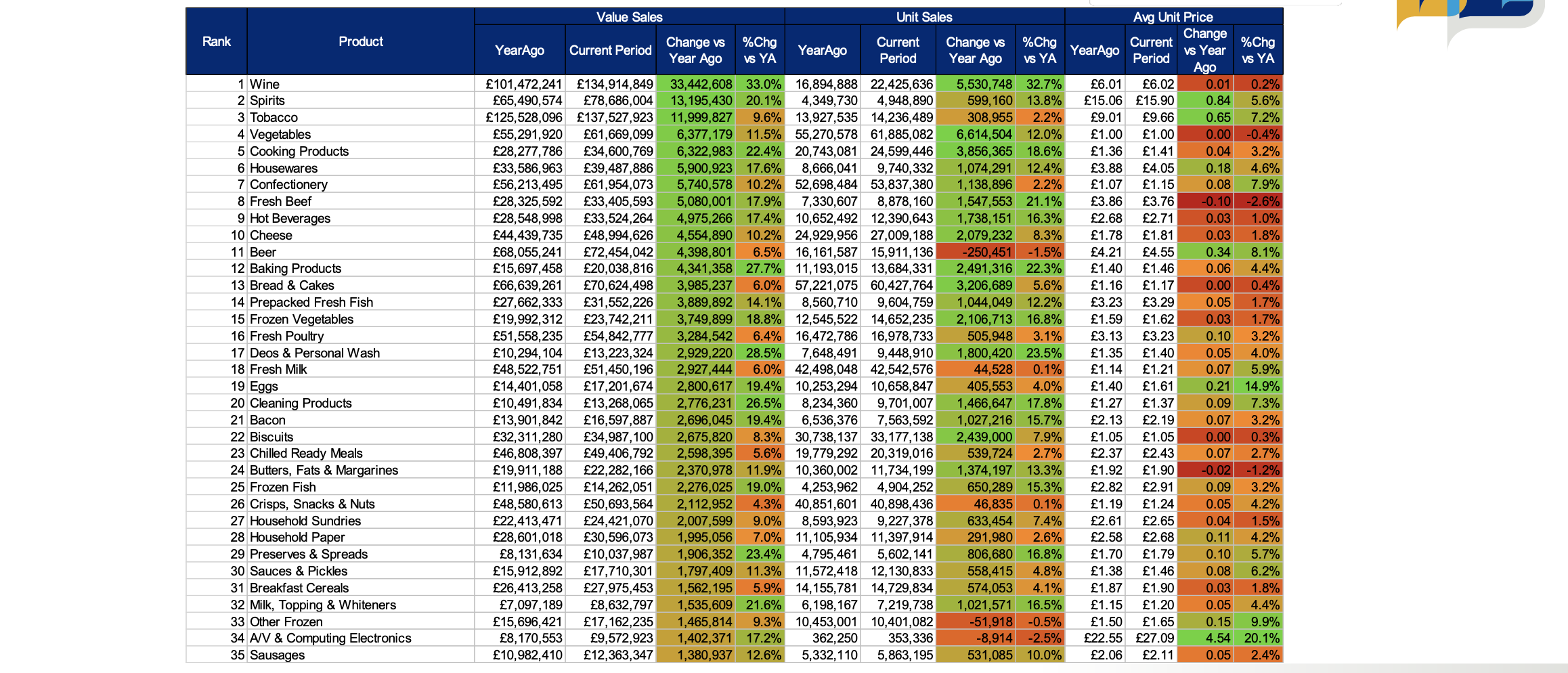

Top 35 Categories based on Value Change for the Latest Week

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}