This flash report contains:

• UK Market Context

• Summary of UK Performance

• Category Performance

• Top Manufacturers

• Bottom Manufacturers

Summary of UK Performance

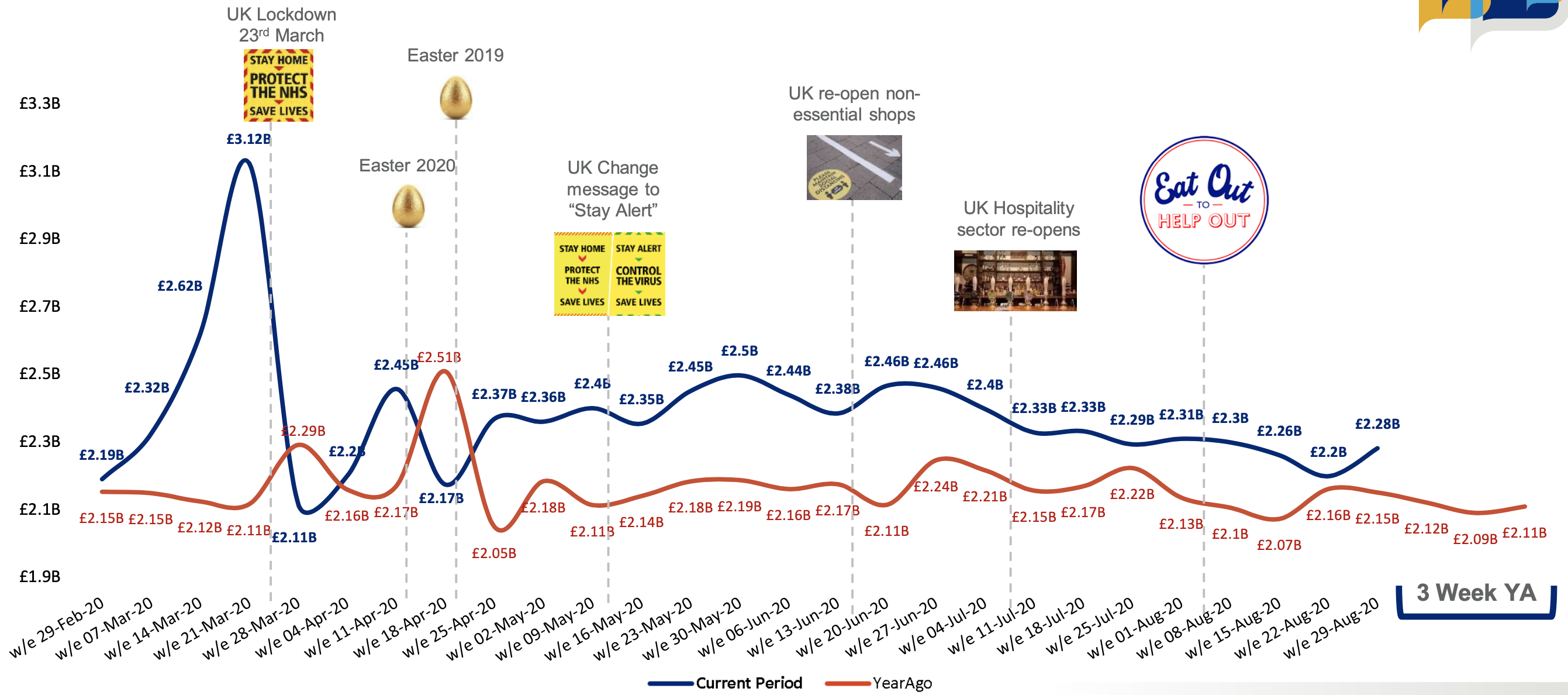

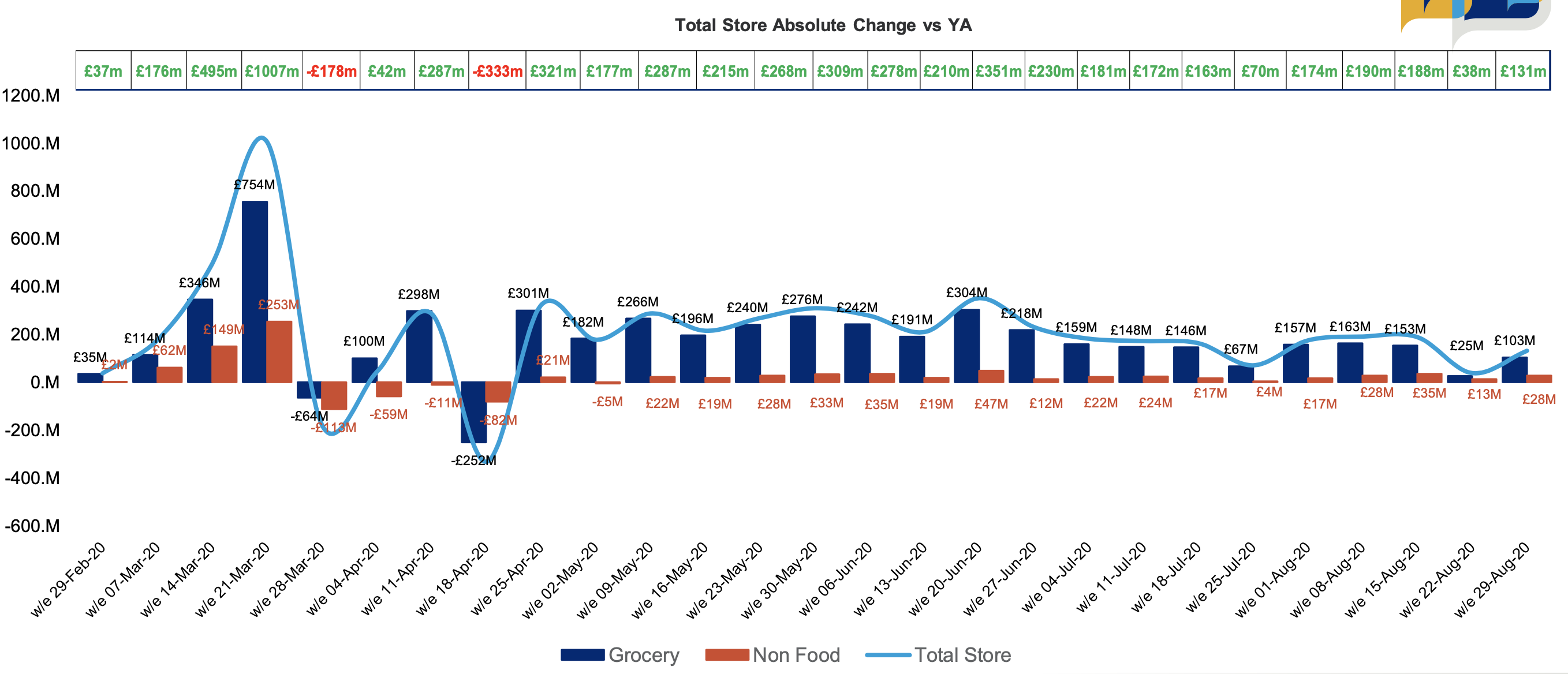

- In the latest week, sales reached £2.28b; £131m higher than the same time last year an increase of +3.8% on last weeks’ sales

- This week's sales have benefited from the phasing of the Bank Holiday which was a week later compared to last year, although last year we had warmer weather. The “Eat Out to Help Out” scheme ends in August and we know this has been successful with 64m meals claimed in the first 3 weeks. With the scheme ending on Monday and schools returning this week, it will be interesting to see what impact this has on sales.

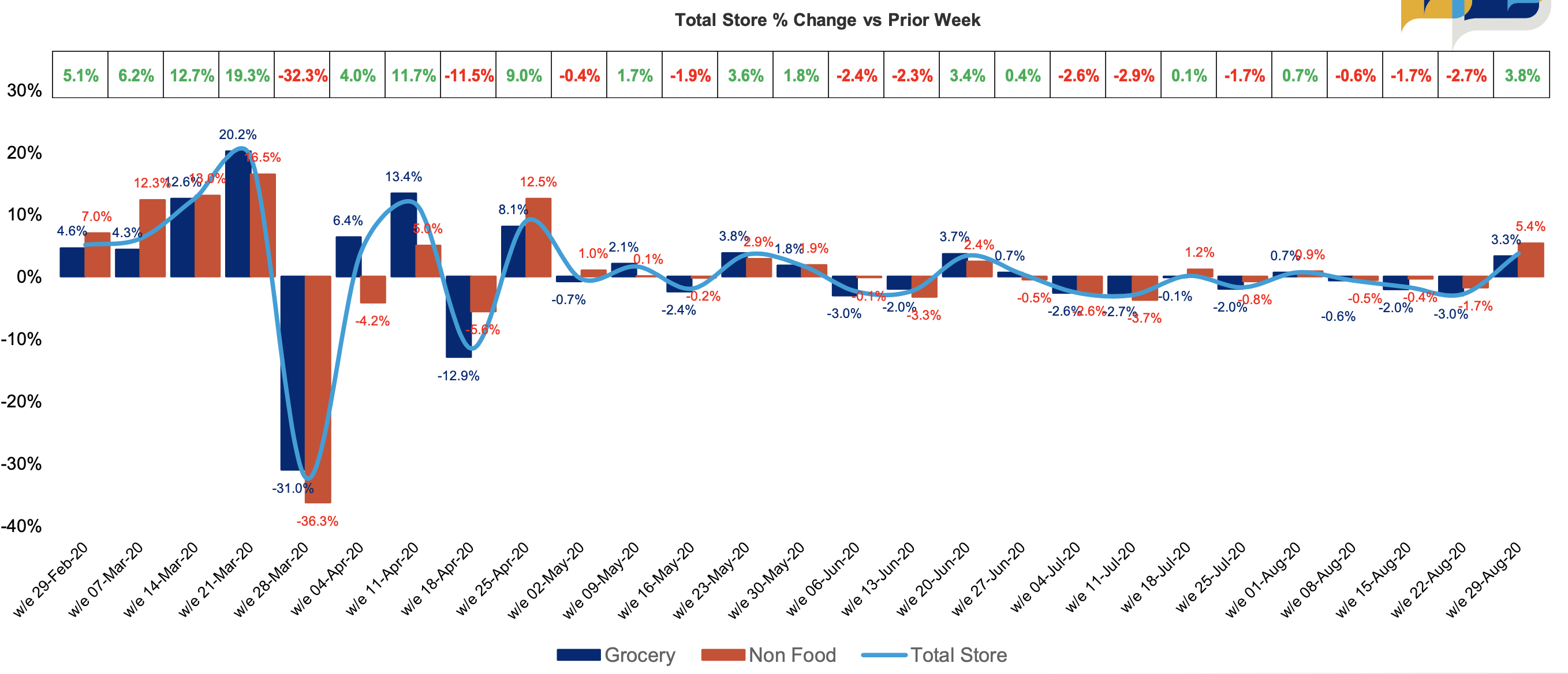

- Of the additional £131m spend in the latest week, this was driven by Grocery +£103m and +£28m in Non Food

- BWS is back in the top performing Sub-Categories with Tobacco, Fresh Meats, Prepacked Cooked Meats, Prepacked Fresh Fish and Personal Wash feature in the top growing Sub-Categories

- Worst performing Sub Categories remain those impacted by the continued lack of movement, so Food to Go categories; Sandwiches, Lunch Salads, In-Store Bakery Goods and Prepared Fruit Salads as well as those impacted by the difference on the weather vs last year

Total Market Sales Value

In the latest week, sales reached £2.28b which is £131m higher than last year. This week's sales have benefited from the phasing of the Bank Holiday which was a week later compared to last year, although last year we had warmer weather. The “Eat Out to Help Out” scheme ends in August and we know this has been successful with 64m meals claimed in the first 3 weeks. With the scheme ending on Monday and schools returning this week, it will be interesting to see what impact this has on sales.

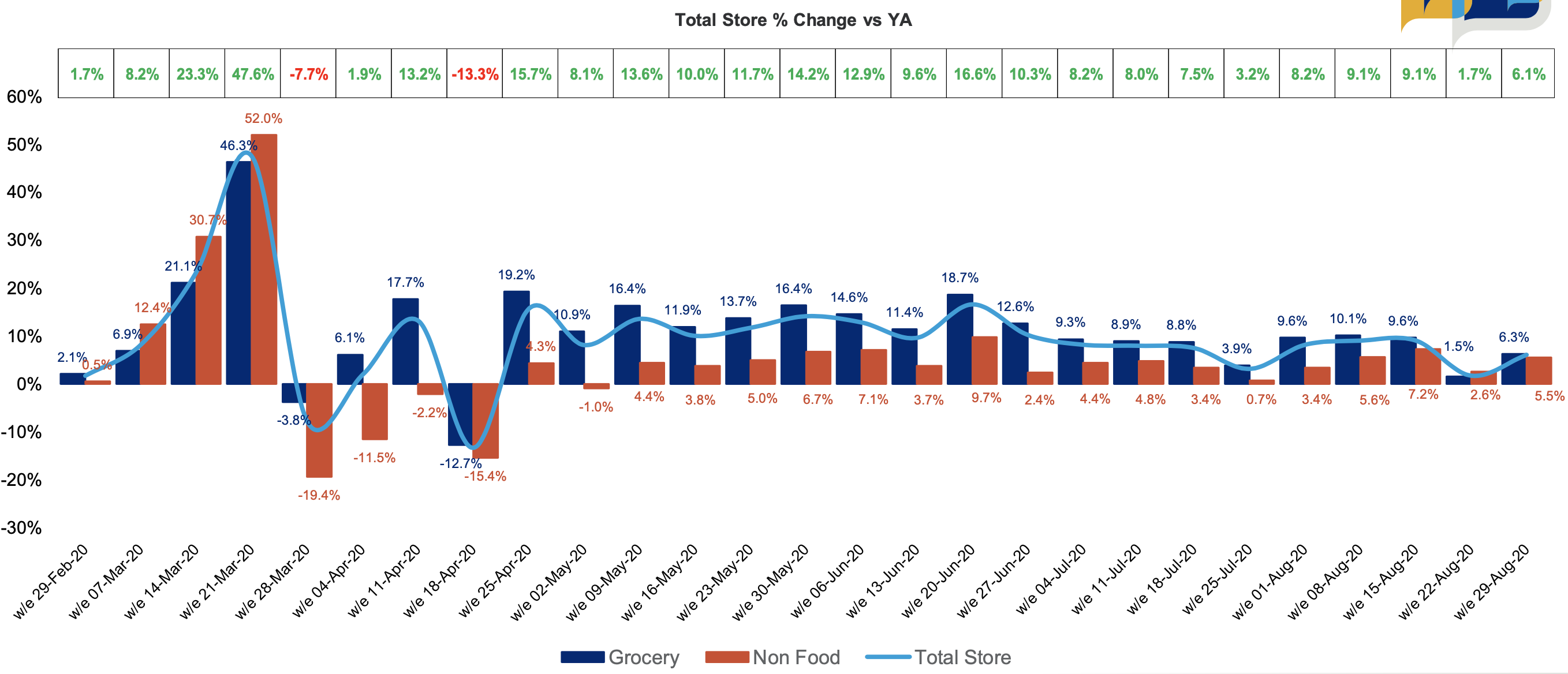

Total Store sales +6.1% vs year ago with Grocery growth +6.3% and Non Food growth +5.5%

An Additional £131m has been spent in the latest week driven by an increased Grocery spend of £103m and £28m in Non Food

Overall sales grew +3.8% this week compared to last week with Grocery sales up +3.3% and Non Food sales up +5.4%

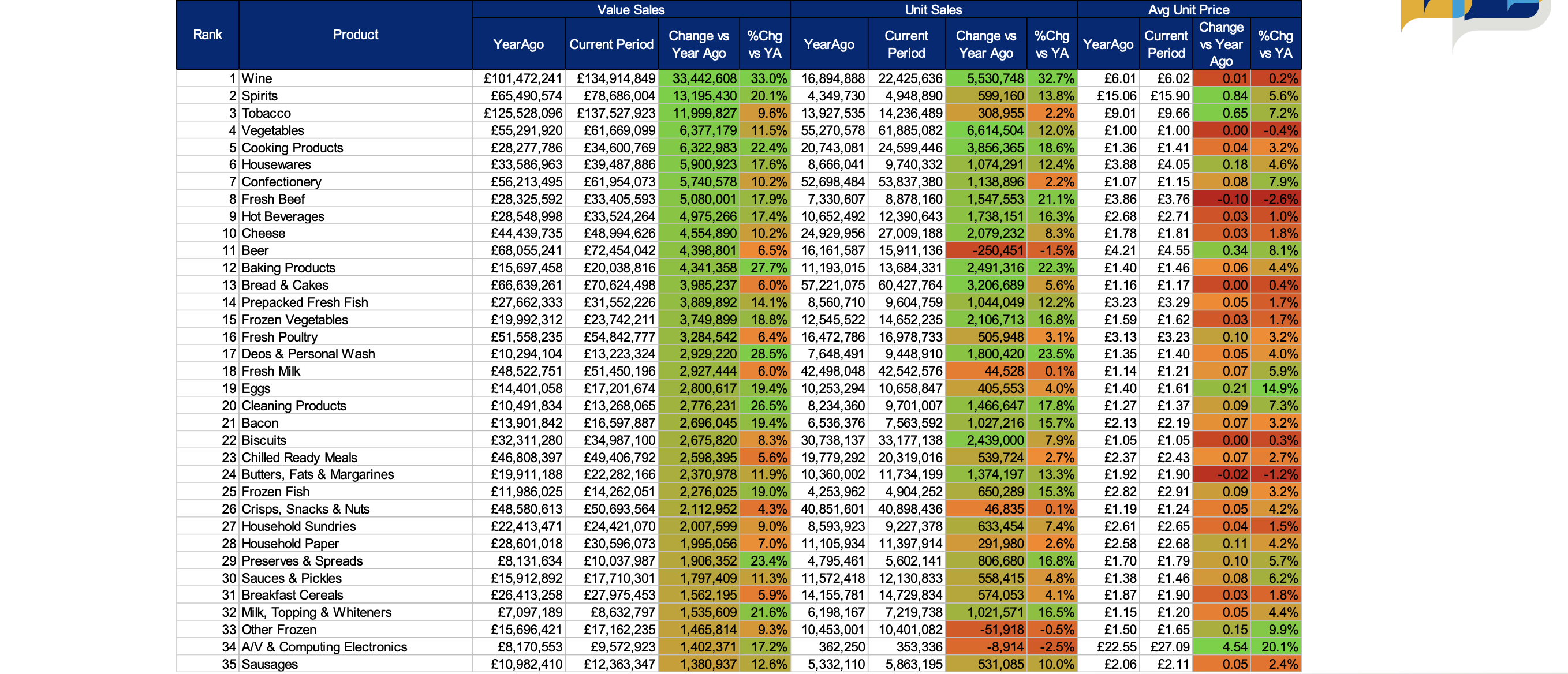

Top 35 Categories based on Value Change for the Latest Week