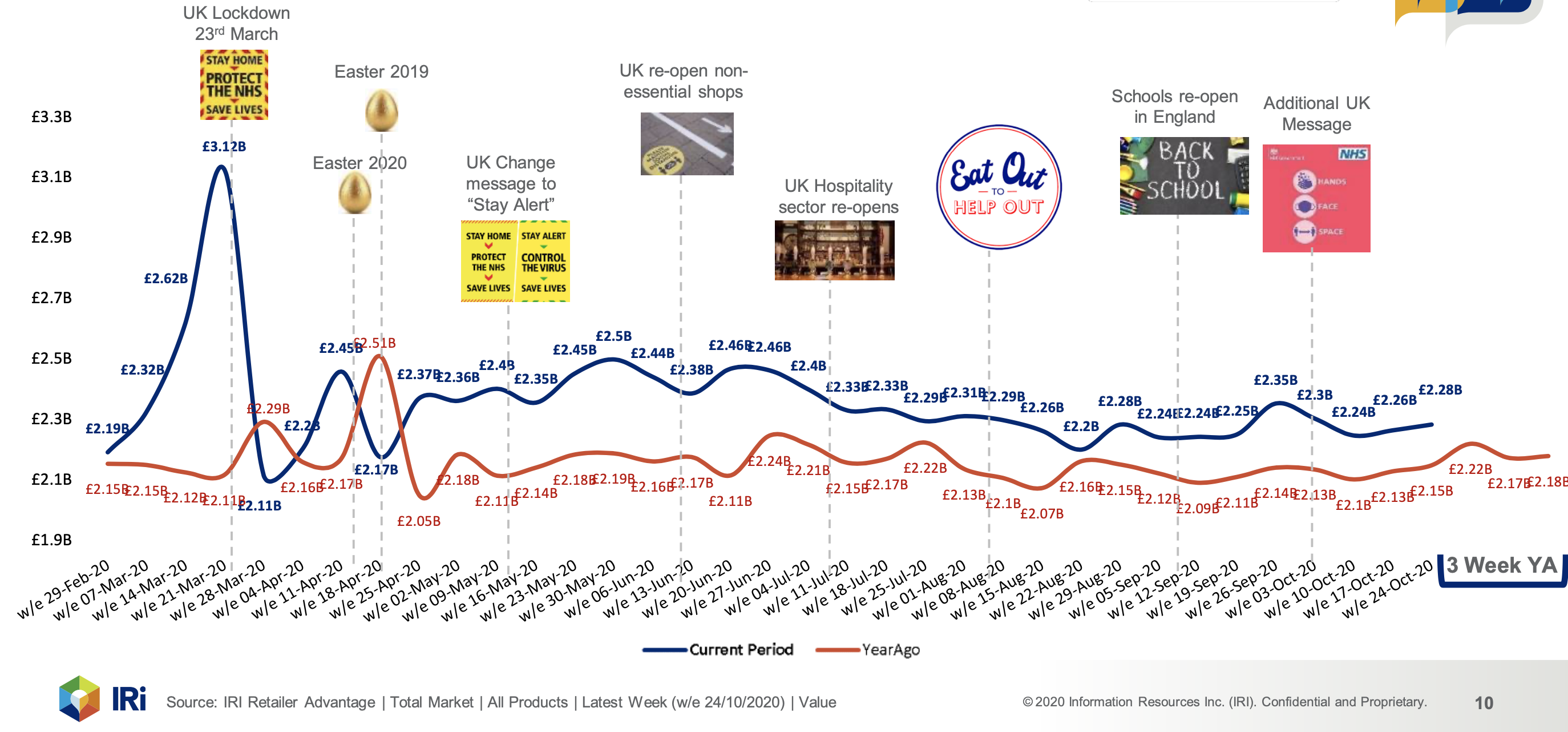

With more COVID-19 cases and an increase of local areas moving into Tiers 2 and 3, sales grew +0.8% compared to last week. This week's sales of £2.28b are £134m ahead of last years with the trend in line with what we have seen over the last few weeks. However with the 2nd lockdown in England starting 5th November, we can expect to see a sales increase in the data to 7th Nov.

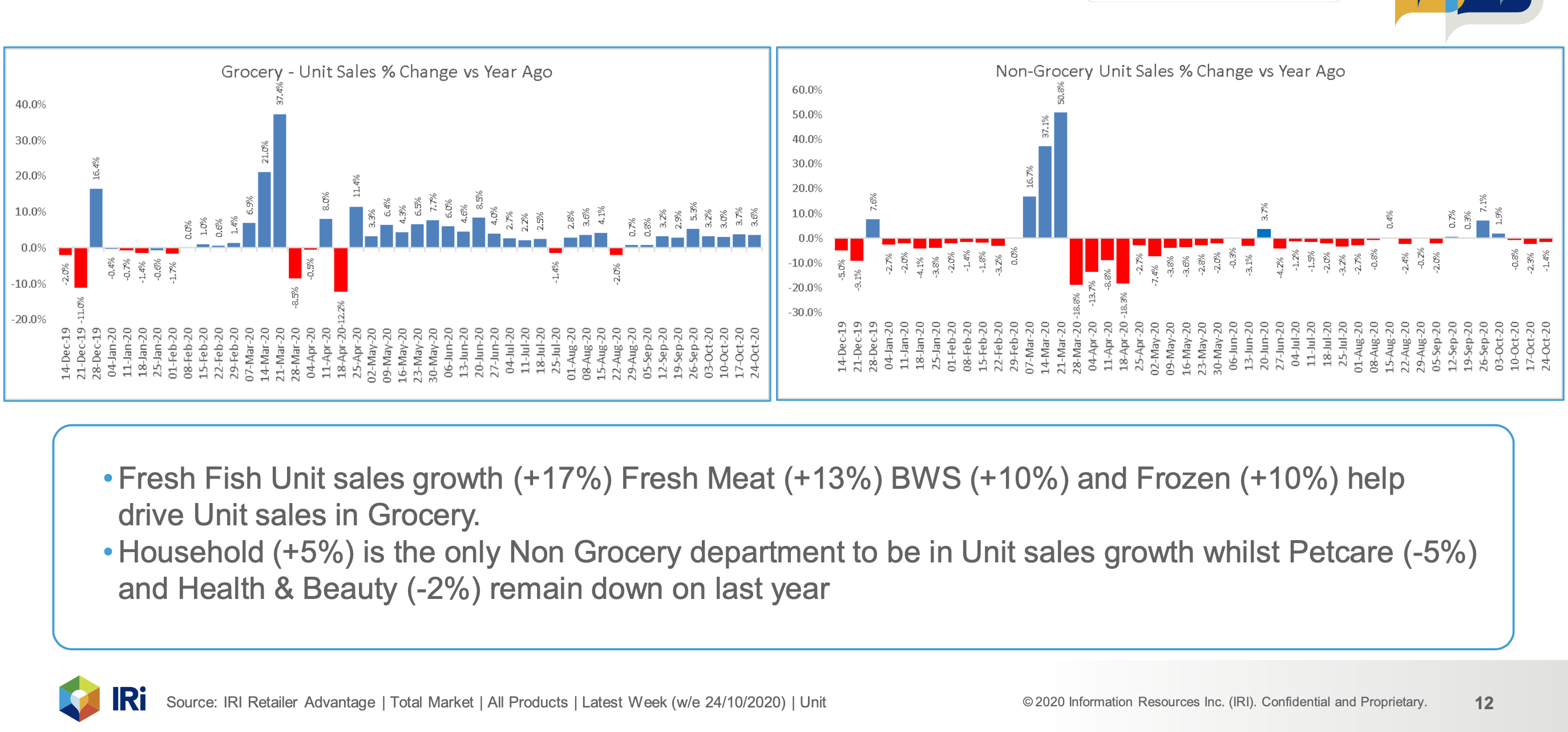

Unit sales grew in Grocery (+3.6%) as Fresh Fish/Meat increased linked to greater restrictions. Non Grocery (-1.4%) sales dropped in the latest week driven by a drop in Household.

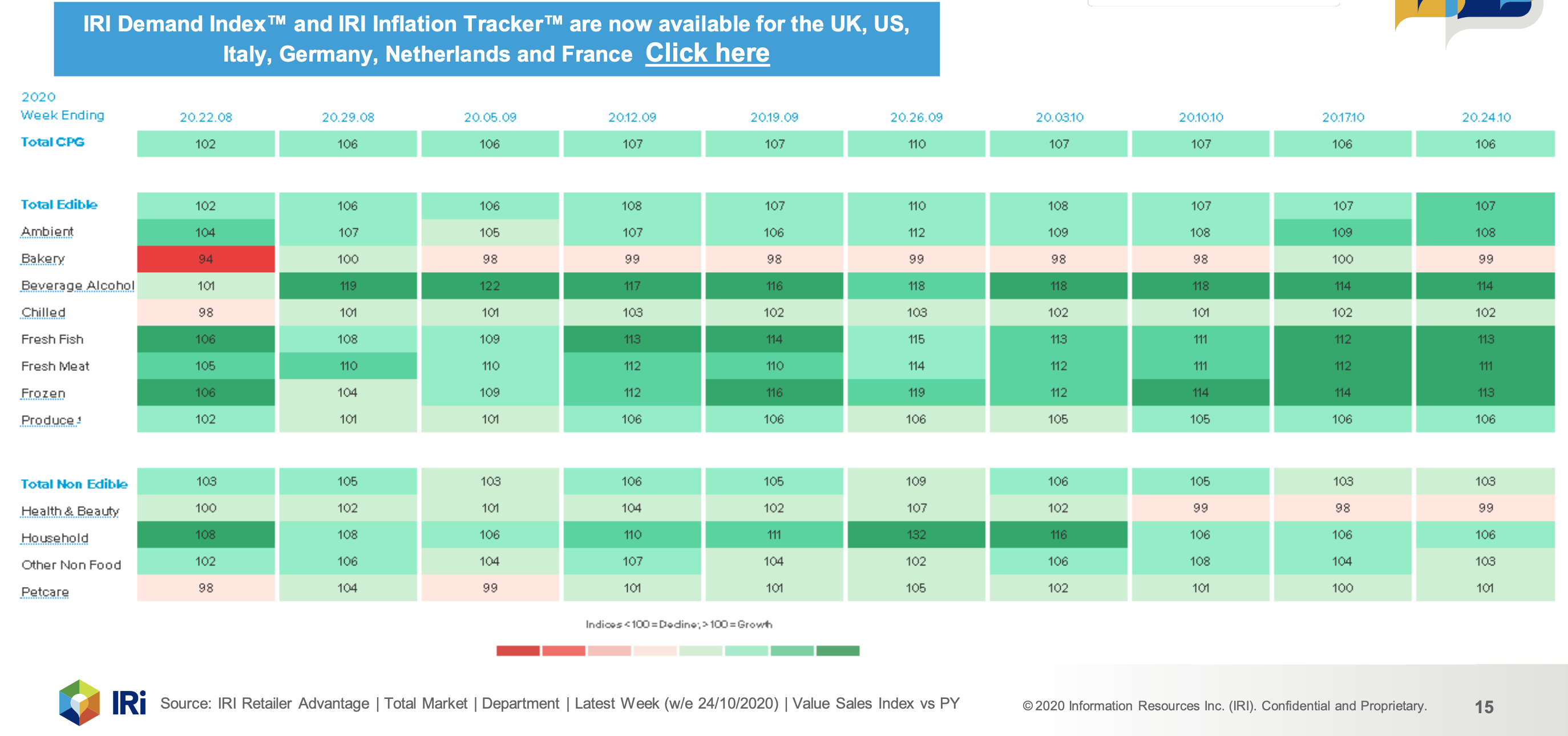

The recent increases in UK COVID-19 cases and subsequent increased government restrictions being put in place have meant demand for CPG products remain high.

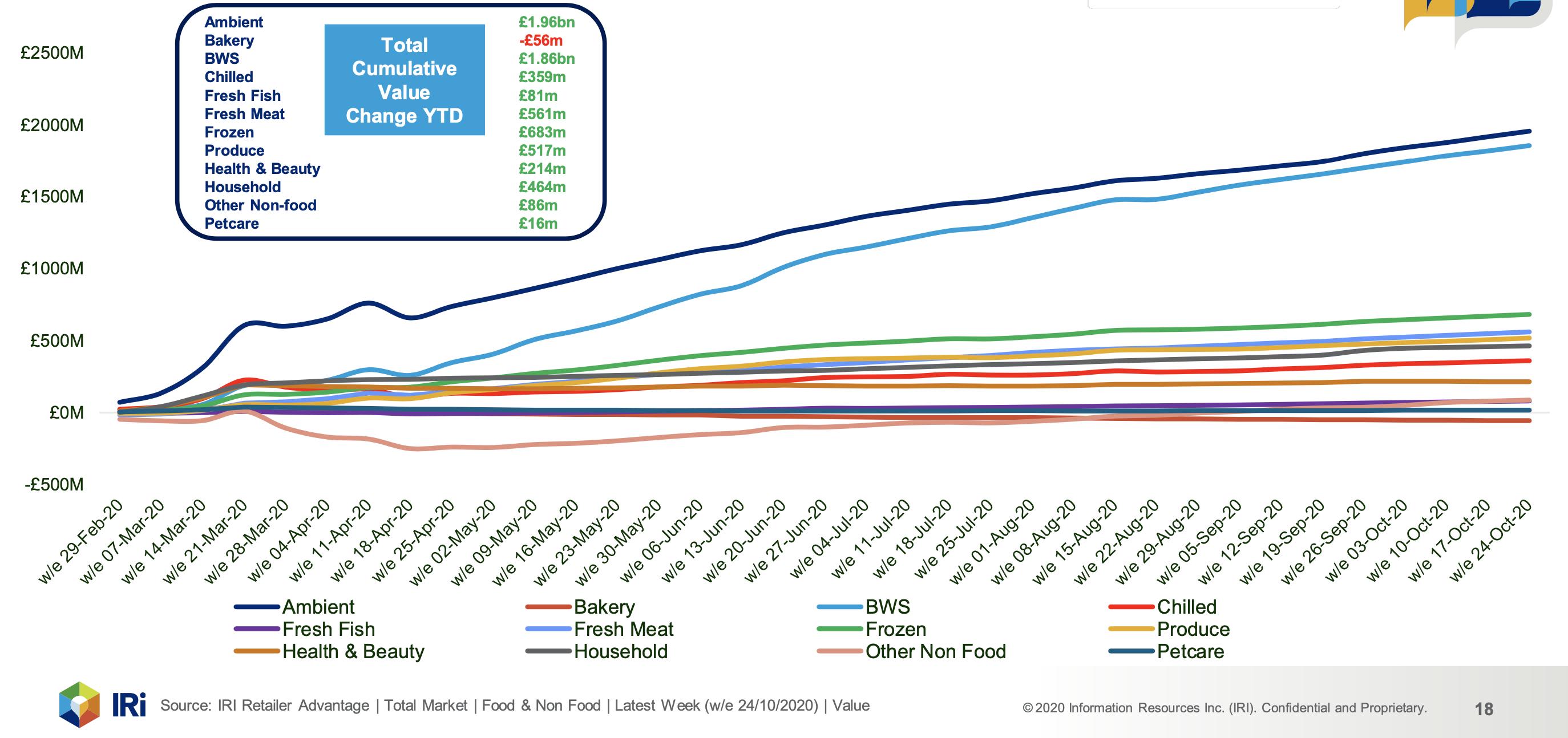

Since the beginning of 2020 and predominantly since the start of COVID-19, UK Retailer sales are £6.740b higher than last year, driven by Ambient (+£1.96b) and BWS (+£1.86b).

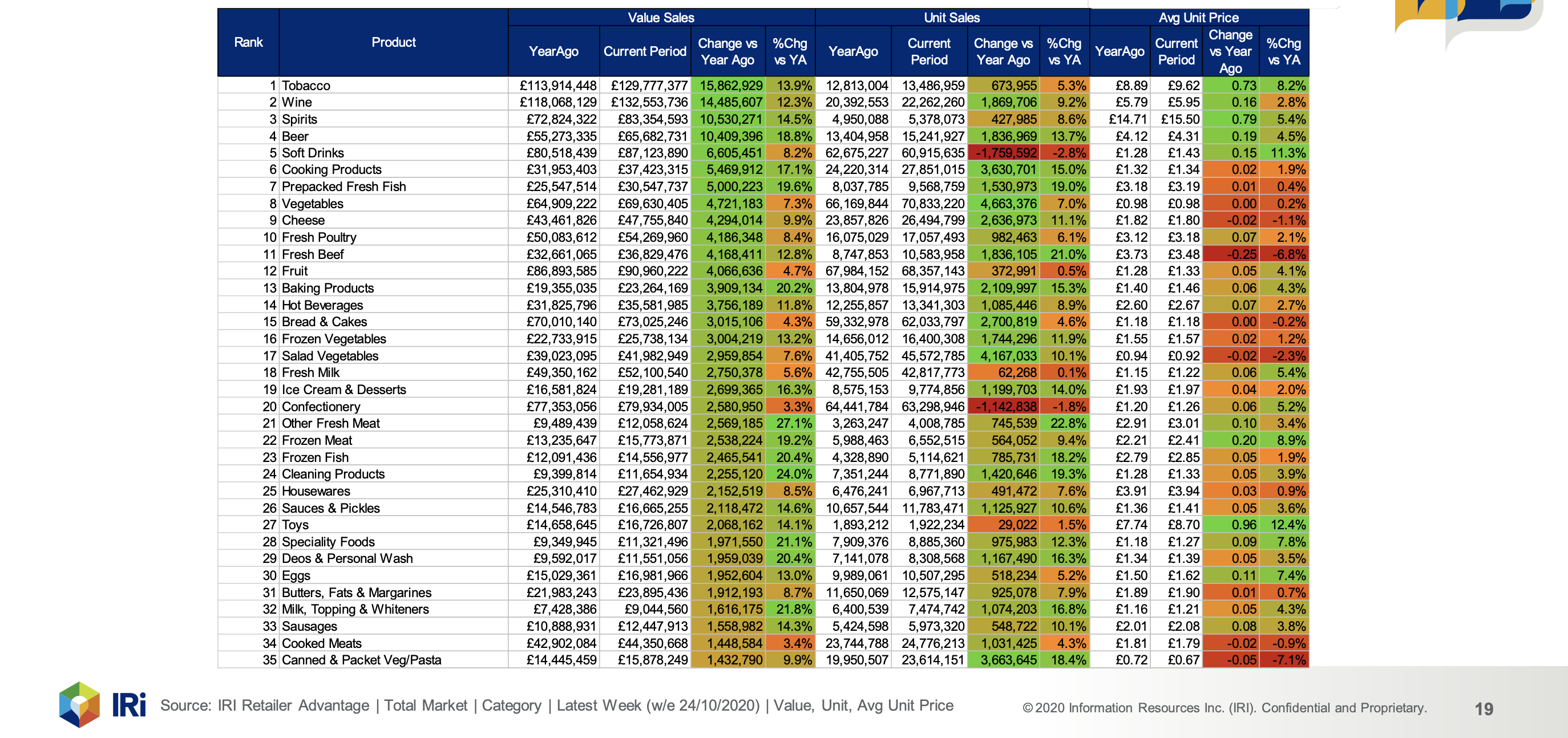

Top 35 Categories based on Value Change for the Latest Week.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}